Could Kazakhstan be the 'Dubai' or Lehman of 2022?

Could Kazakhstan be the 'Dubai' or Lehman of 2022?

Ferdinand or Khrushchev?

I wrote last week in the Complex Systems section about what appear to be hypercritical societal conditions that have started to be unleashed. News breaking out of Kazakhstan over the past couple of days highlights the inherent challenge of complexity. It is probably impossible to predict with a degree of confidence what and when the ultimate catalyst for a phase transition to emerge.

I have placed ‘Dubai’ in quotes in the title, because my memory is not what it used to be, and am unable to find confirming reports via web searches. However, my memory is that there was a relatively brief market event, or mini-panic, around US Thanksgiving in 2006, in which there were initial signs of potential market distress. Of course, it is such a non-event in the resulting timeline that I am not even sure it happened!

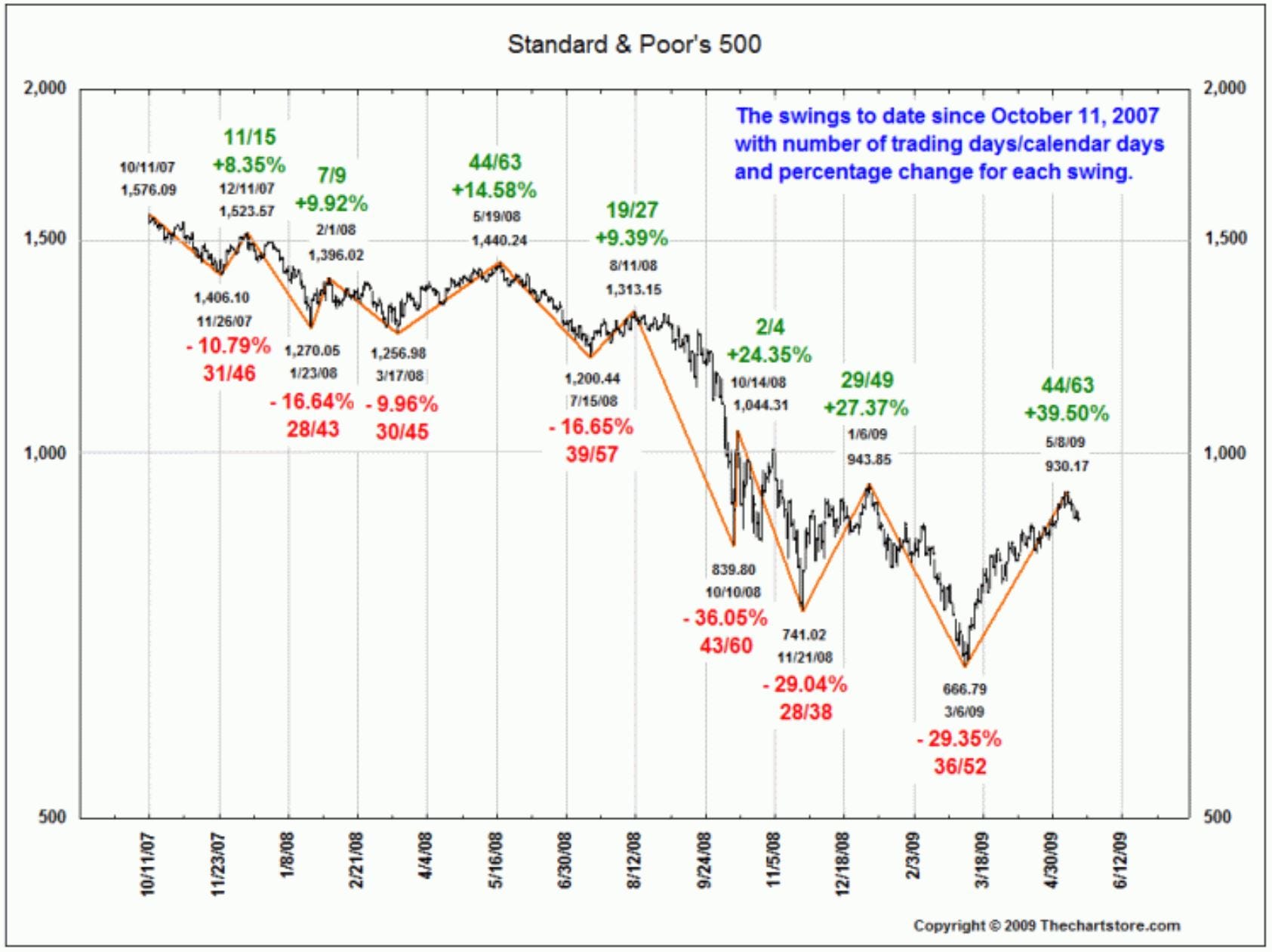

Subsequent to that, we had subprime-related credit instruments peak in late 2006 and begin to drop, then the mini-crash in Chinese stocks in February 2007, which coincided with what remains the all-time high in the US large bank index (BKX) at 121.16. The Bear Stearns hedge funds active in mortgages blew up in June 2007, then we had the quant blow up where Cramer went on his infamous ‘they know nothing’ rant in August 2007. Of course, the Federal Reserve, which had just issued an inflation and tightening bias statement a few weeks prior, panicked and cut interest rates, launching the major US market averages to new highs into October 2007. Here is a chart from thechartstore.com showing the bear market from that peak:

Societe Generale was the next big ‘news’ on the US Martin Luther King Day holiday in January 2008, which was sort of when the European central bank joined the panic. Bear Stearns then collapsed in March 2008 and was part of an arranged shotgun merger, which was followed by a rip-roaring market rally which took the S&P 500 back up to within 10% of the then all-time high reached in the prior October.

Fannie Mae and Freddie Mac proceeded to implode in July into August, and then the real ‘fun’ began in August into September. Of course, nearly everyone active in markets at the time remembers Lehman, and probably when the infamous TARP initially failed.

So why this chronological stroll down a horror show memory lane? Do you remember Auction Rate Securities? I had never heard of them before the crisis - they were a pseudo ‘cash’ product sold by the big wirehouse brokers and became illiquid. Do you remember when the Reserve Fund, a well-respected long-standing, money market fund that ‘broke the buck?’ What about New Century or Countrywide Financial?

When systems reach inherently unstable, or hypercritical conditions, the condition is what is paramount and creates the embedded risks. I reviewed this timeline as context, as there was a veritable orgy of potential catalysts which could have been the butterfly flapping its wings, with many of them likely forgotten, or never even known, by many.

I do not know about you, but I have not had Kazakhstan on my radar- heck…have checked 6 times am spelling it correctly, and am still not confident. Seemingly like everyone else, Ukraine and Taiwan have been the obvious potential hotspots to which I have paid some attention. But when phase transitions occur, chaos can ensue, with seemingly no rhyme or reason to the sequencing of what ‘matters,’ and what does not. Why didn’t the market meltdown when Fannie and Freddie imploded in 2008? Post-hoc there is always a reasonable narrative that emerges - letting Lehman go bankrupt is a common narrative now as to what ‘caused’ the meltdown. But did it?

Will Kazakhstan end up being Dubai, Bear I, Quants, SocGen, Bear II, Fannie/Freddie, or Lehman of this cycle? No idea, and frankly from an analytical perspective relative to the underlying system dynamics, it is not that relevant. Like the assassination of Arch Duke Ferdinand, or the Cuban Missle crisis, who knows whether this hypercritical system will cascade or not? Regardless, it appears to me that global financial markets are not sufficiently pricing in the elevated risks it, or something else from out of the blue, does.