Crushing Consumers

Much has been said and written about the resilience of the American consumer. ‘Betting against’ them long term has generally been a terrible idea. Conceptually, that would be like having a bet against Visa and Mastercard - doh!

However, if a significant long-term shift were to occur, what might it look like? The potential scenario has begun the creep into what is the dark and crazy recesses of my mind, as the Bizarro Recession scenario takes shape.

The 1980-1982 period launched the era of lower inflation, lower interest rates, and the explosion in the financialization of the West, with the United States at the epicenter.

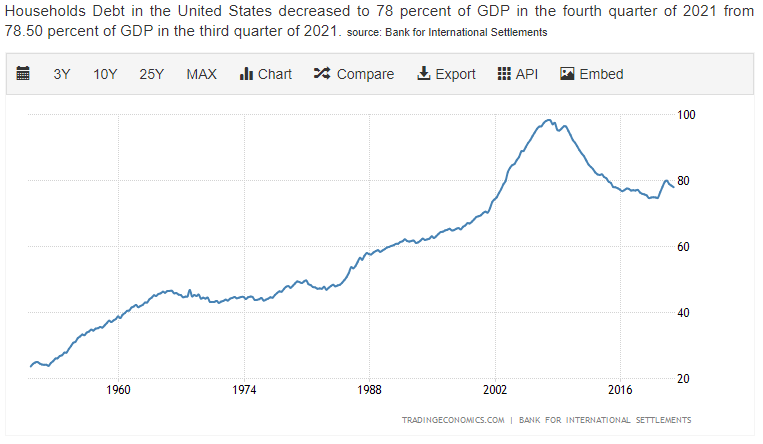

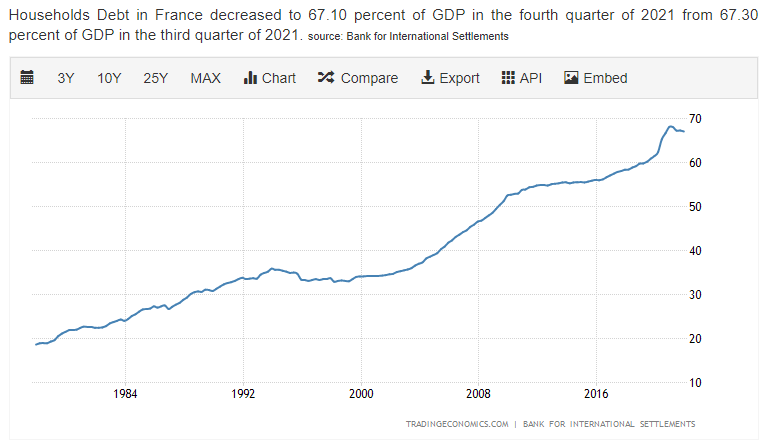

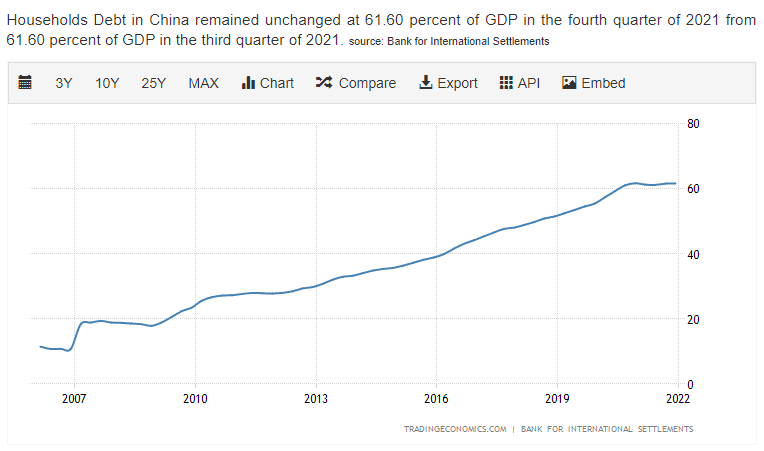

Another not-so-funny example of how price fixing interest rates below even phoney baloney inflation rates has resulted in excess demand. The Global Financial Crisis served as a sort of convulsion which crescendoed the growth, and the era of financial repression policies served to incentivize borrowing even more. This has not been a trend specific to the US:

Yes - debt levels for consumers using broad aggregates in the US are down quite a bit from the levels reached pre-GFC, but citing that fact overlooks some important variables:

Averages can cloak what is occurring underneath the surface

Sanguine views on debt often reference relative metrics

Historical relationships may not be stable

Median debt to income ratios in the US has increased from about 1.1 to 1.8 since the year 2000, and even metrics using medians can mask what is occurring on the left side of the income distribution. Prior to the onset of the pandemic, average US savings account balances were over $40,000, but the median was just $5,000. Looking at income percentiles, the bottom twenty percent has a median saving balance of $800, and the next twenty percent about $2,100.

The massive stimulus dispersed during the pandemic shifted these a lot, but what we have seen in the past year has been a rapid return to ‘normal.’

Revolving credit has recovered to approach new highs following the large decline during the pandemic.

As reflected above, real disposable incomes spiked dramatically during the pandemic, but have now rolled over back to what had been the post-GFC trend.

For a huge segment of US households, and the issue is far more severe in many countries around the world, balance sheets were/are simply not in a position to handle this:

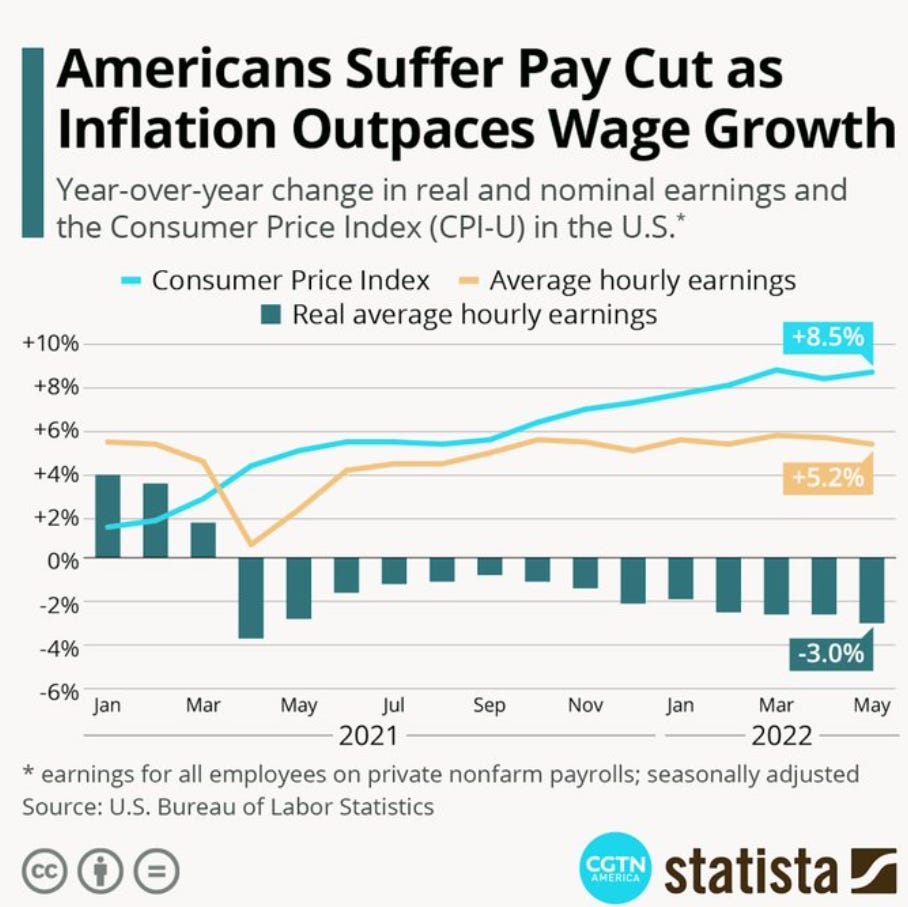

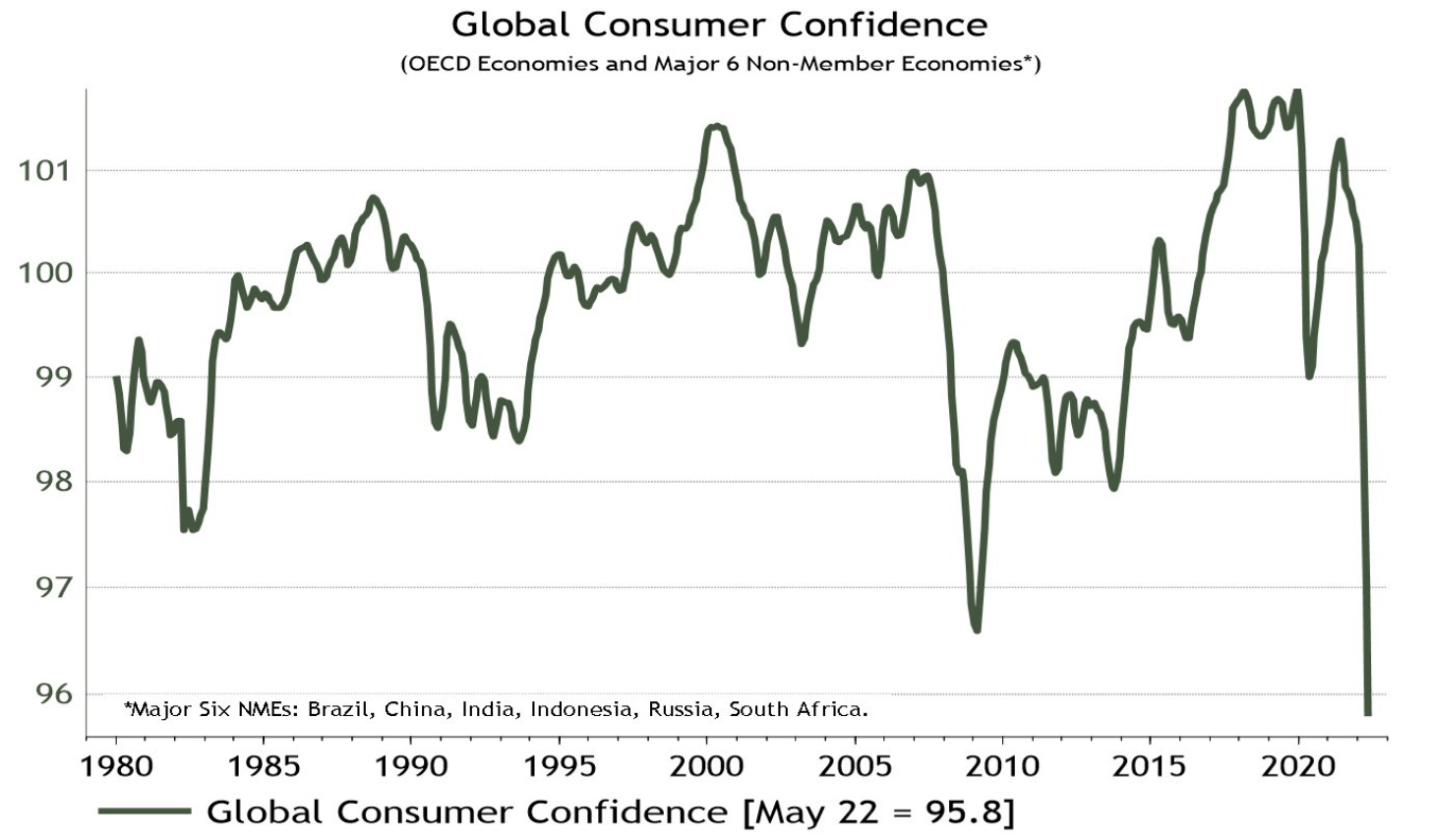

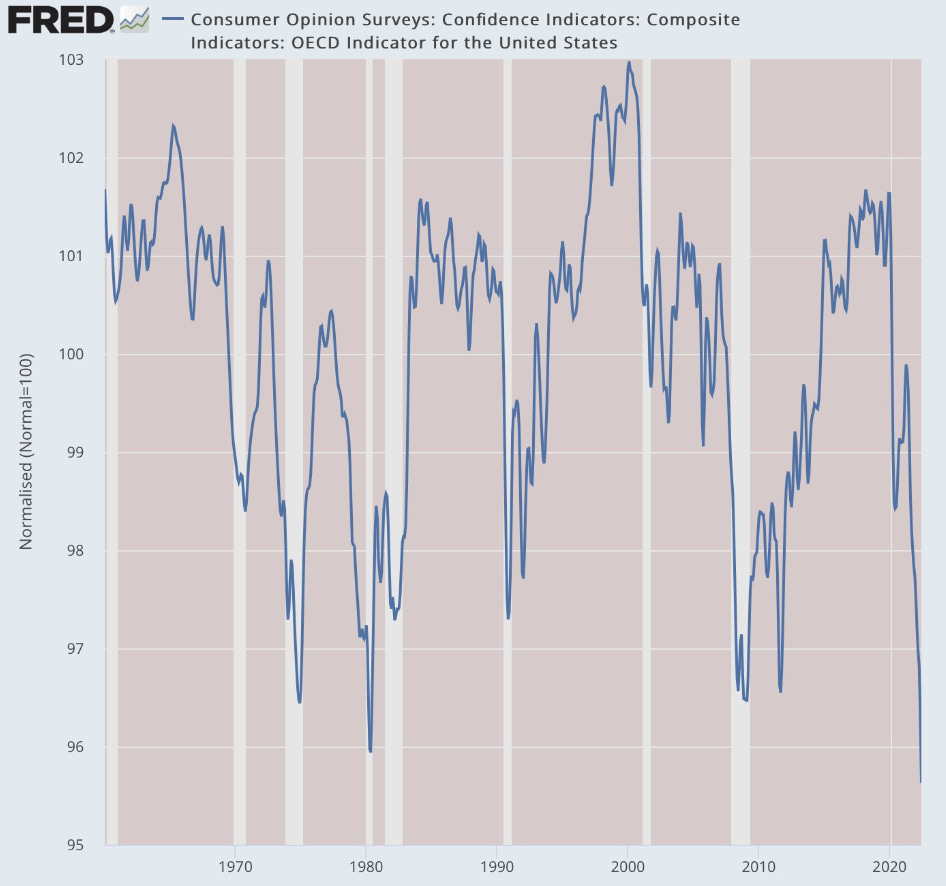

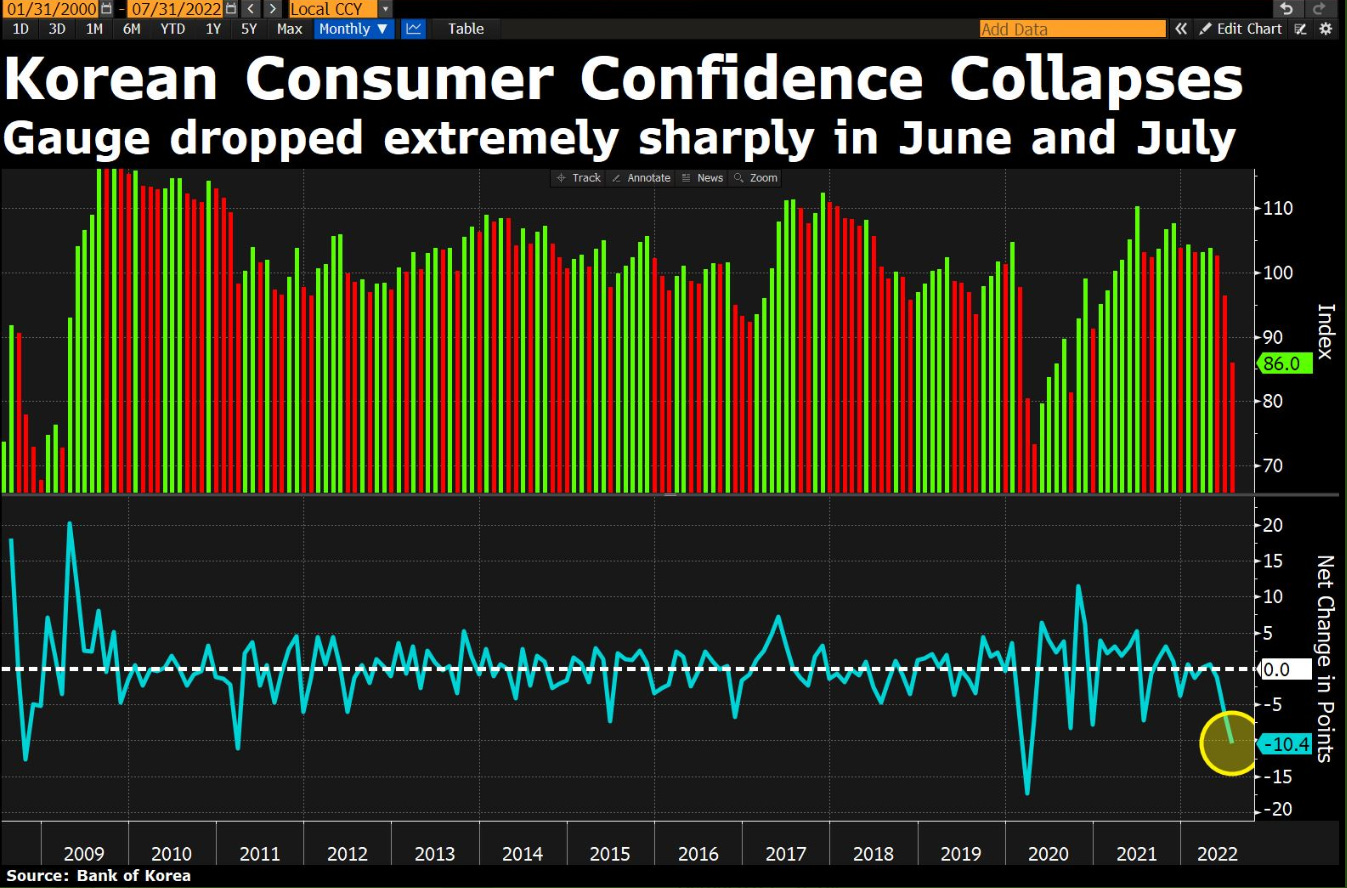

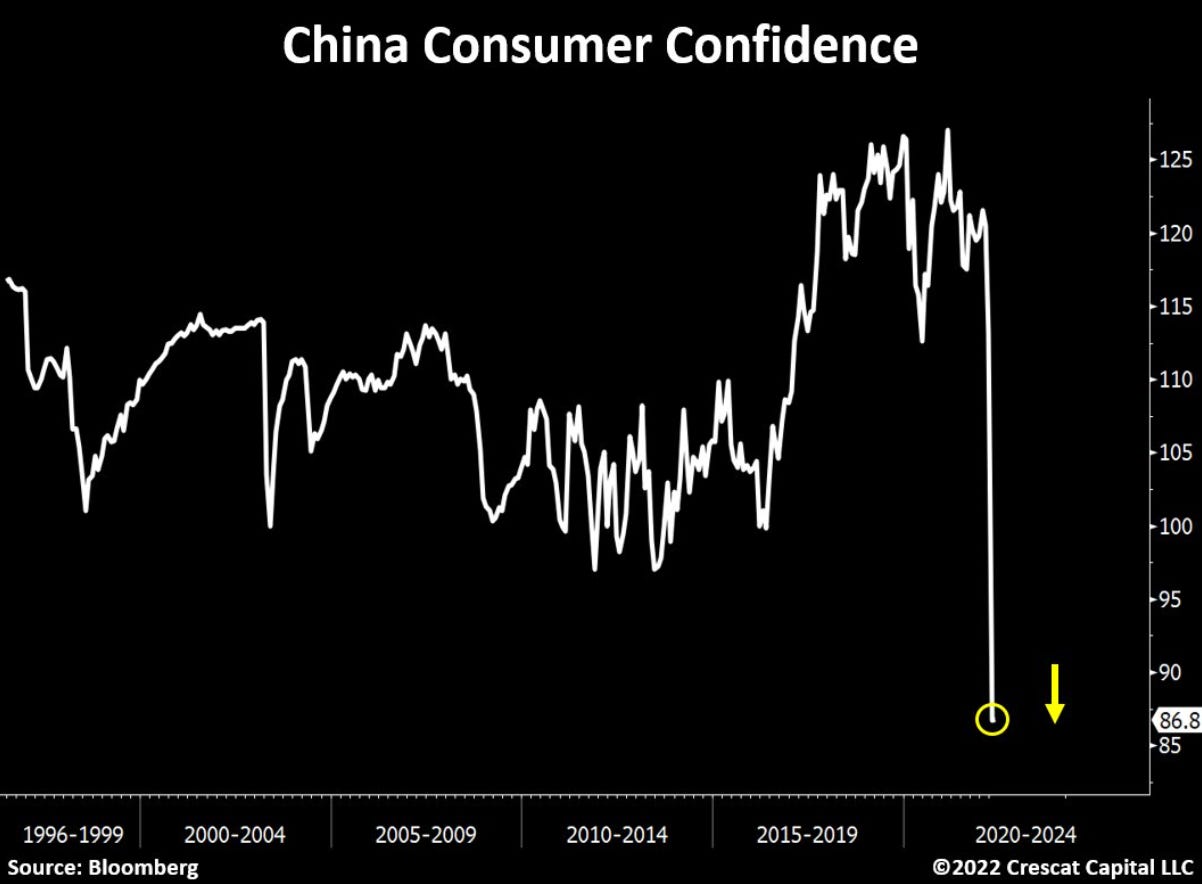

Nominal wages have been rising but not at the level of consumer prices - even as ‘measured’ by the phoney baloney BLS CPI. Perhaps unsurprisingly, consumer sentiment has been plummeting, but not just in the US:

These developments have all transpired prior to a significant upturn in job losses and related unemployment, which typically increase dramatically in business cycle contractions. With inflation a typically sticky phenomenon, real wages may remain under pressure even as job losses increase, all while a huge segment of households are already at a tipping point financially. This leads us back to Regime Change.

Governments are already collapsing around the world, with civil unrest on the rise. The US Congress continues to spend like drunken sailors, and that is before the brunt of the wave hits US households. I expect massive fiscal responses to try and placate increasingly unsettled citizenries while accelerating the opening of Pandora’s Box via the inflationary forces unleashed via pandemic-era policies.

The Bizarro Recession may usher in Regime Change and an end to the seemingly endless resilience of the US/Western consumer. As we have seen with climate change, central planning has a way of ‘firing up the old coal plants.’ Policies nominally intended to help the working and middle classes are likely to end up doing the opposite.

Curious, why am I being offered credit cards this past week with zero APR for 15 months? I wonder what went into the decision. Do banks intend to get repaid by consumers? Is a new account on the books now more useful in their earnings call than what any damage that could occur later on? I realize my questions are for someone who understands how banks issue consumer credit.