Divorcing Demand

Divorcing Demand

Have supply siders been unfaithful?

With so much ink spilled and oxygen consumed regarding the supply chain shock of the past two years, I could see how the demand side could have grown jealous. Perhaps a divorce could even be in the cards for the two? Could supply divorce from demand in the coming months?

The Fed Chairman’s comments Wednesday about a higher terminal rate for this cycle than they had previously expected occurred within the context of the global business cycle continuing to erode. Here is what the March 2023 euro dollars futures contract began to price in after the comments:

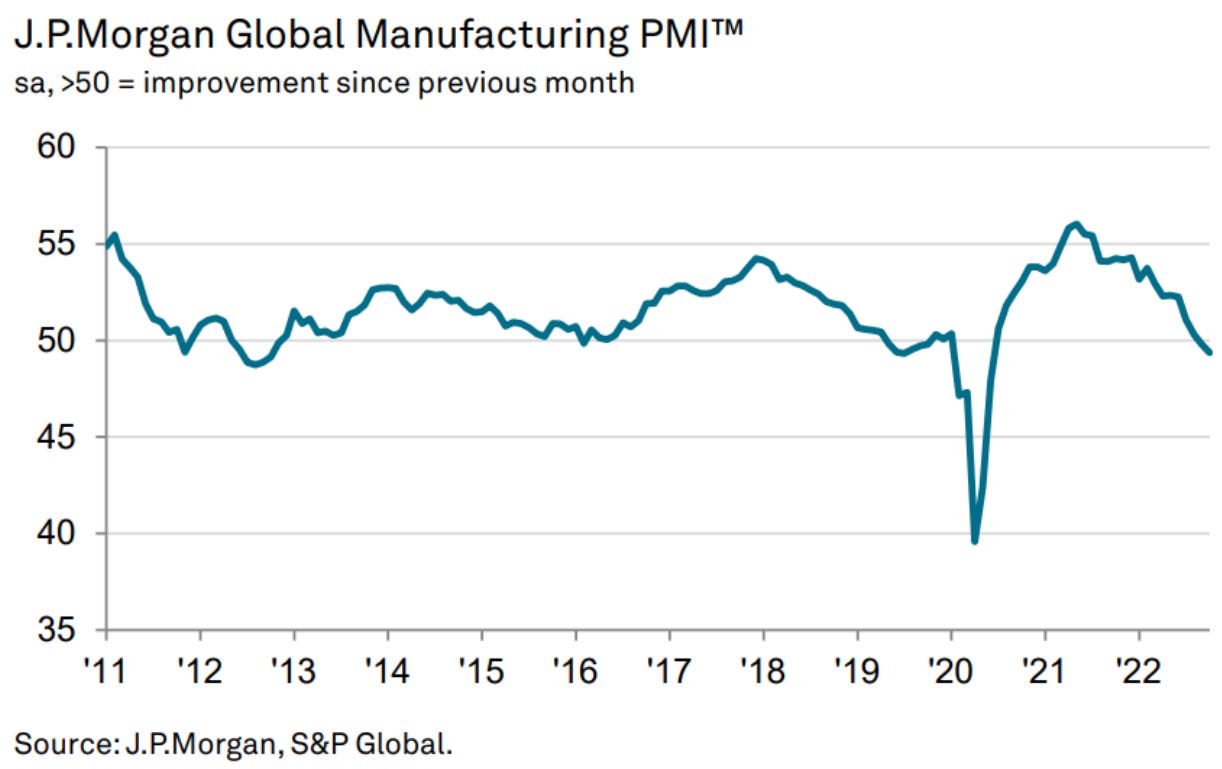

The Global Composite Purchasing Managers Index (PMI) has dropped below 50, which is the level which demarcates expansion versus contraction.

Perhaps unsurprisingly, the Eurozone appears on the front edge:

Those are coincident economic data. Leading indicators are still pointing sharply lower for the global economy. I recommend readers watch this approximately 38 minute presentation from October 25th, in which Lakshman Achuthan of ECRI provided a cyclical update through the lens of their leading indicators. Just after the 35 minute mark, a slide appears showing ECRI’s 21-Country Long Leading Index Growth Rate, which was already at a level comparable to the depths of the 2020 lockdown-driven recession, and also where the index was just prior to Lehman Brothers going bankrupt in 2008- i.e. already nine months into the US recession.

The slide also showed a diffusion index of central banks and their relative tightening versus loosening policy directions, and it was at a record high. So to summarize:

Coincident global economic data is right on the cusp of recessionary contraction

Long leading indicators, which forecast about six months into the future, are already deeply into recessionary levels, and have not yet turned durably higher

Central banks are tightening at a record level into the teeth of those conditions

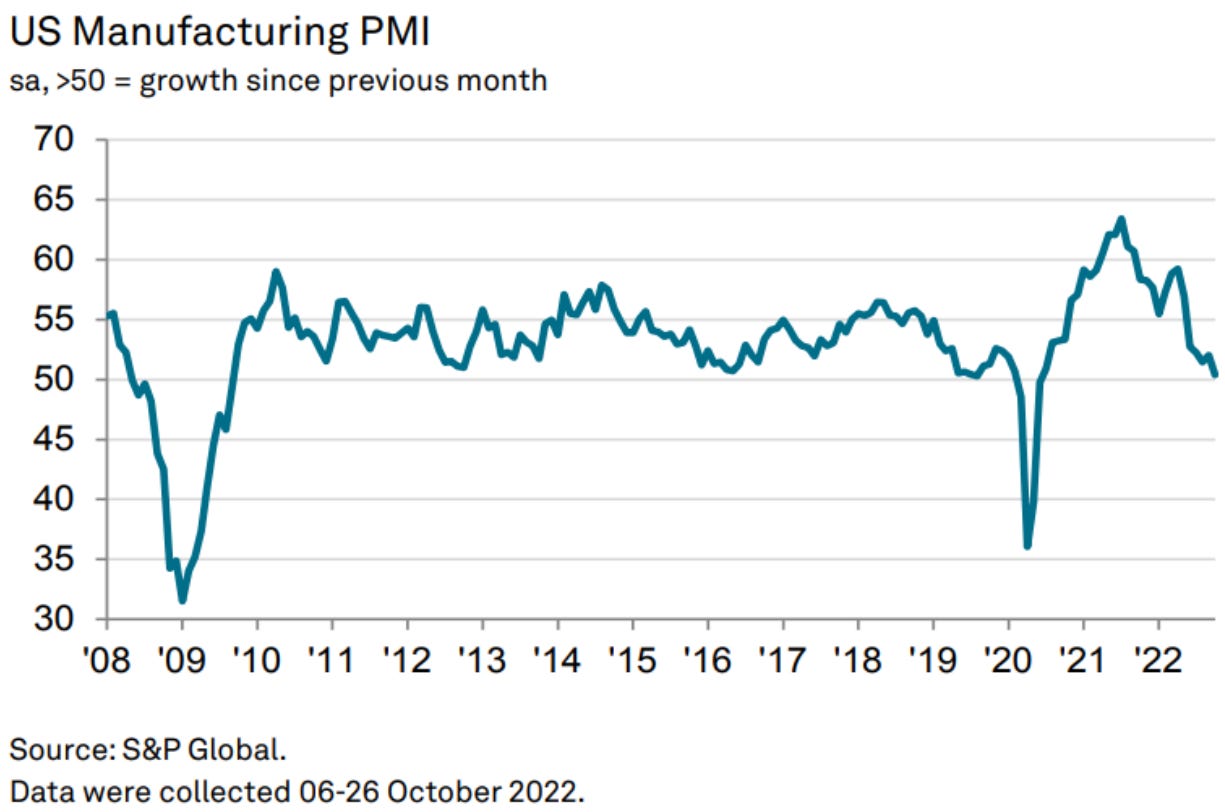

The two quarters of negative advanced GDP reports in the first half of 2022 complicated the normal Fog of Cycles, as we can see from the most recent US PMI report, manufacturing just recently approached the level between growth and contraction:

The US has been on the backend of this cycle, which flips the recency bias-fueled script from 2008, when the US was on the forefront of that global business cycle. The various impacts of recessionary contraction for the US still lay dead ahead:

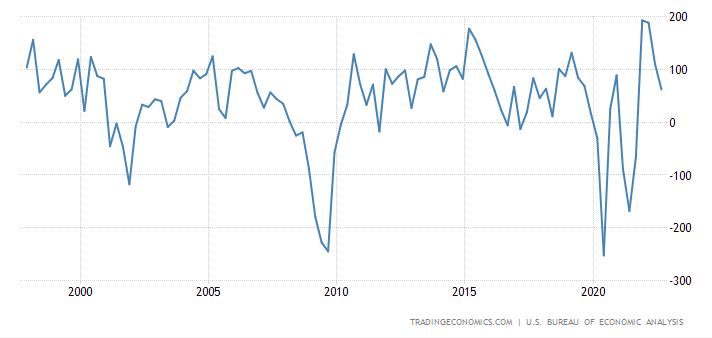

That is ISM New Orders, which has just tipped into contraction territory in recent months.

Business inventories exploded in a yang to the ying of the 2020 lockdowns and subsequent supply chain mess, but have only begun to normalize and remain well above contractionary levels.

This longer term view of the rate of change in inventories suggest what is likely to be coming in the months ahead, with global long leading indicators foreshadowing a severe global recession.

For those who believe that the two negative quarters of GDP in the US signified recession, this can all be quite confusing, I am sure. Demand, employment, and the consumer all held up well during the ‘recession’! With nominal GDP running in the mid to high single digits each quarter so far in 2022, demand has remained high.

The demand destruction the Fed and other central banks are intentionally looking to engineer in order to ‘fight’ inflation is dead ahead, with the US still at the ass end of the cycle. The Fed appears to be making policy decisions using coincident data, like Friday’s October employment report, on lagging indicators on an economy at the ass end of the the global cycle. Contrary to Mr. Brady and Ms. Bundchen, there will be no divorce between supply and demand. Perhaps things could have worked out between the love birds had they Kissed It Patiently. As for the Fed, they appear headed more towards a different pair of kindred spirits.

This is such an excellent summary. Clairvoyant! Thanks for sharing Kayfabe. I always look forward to reading.