Fed Day - Welcome to the Terrordome

Fed Day - Welcome to the Terrordome

I am sending this out just hours before the US Federal Reserve Bank is scheduled to make its policy declaration and release the ‘dot plot,’ which is the epitome of kayfabe, by the way. The idea that a group of political economists who have never as a group forecasted a recession accurately, nor the recent upturn in inflation, would release growth and inflation projections over the next few years that we should all care about? Wooooooo!

I covered the state of the US economy here, on December 8th, and the path laid out remains intact. Growth was slowing on the margin, and subsequently, the wider world is becoming aware of that fact - funny how falling stock prices can cause that. In addition, we now have another month of ECRI’s future inflation gauge having been reported, and for December it was down a chunky 0.9. Inflation in the US is very likely to peak in the first half of this year and then roll over. That is not to suggest ‘deflation,’ but at least for now, lower levels of inflation.

So with that direction of travel remaining intact, today I want to lay out what I see as growing risks of a huge policy mistake made by the Fed. First, some graphs on the pandemic era inflation upturn:

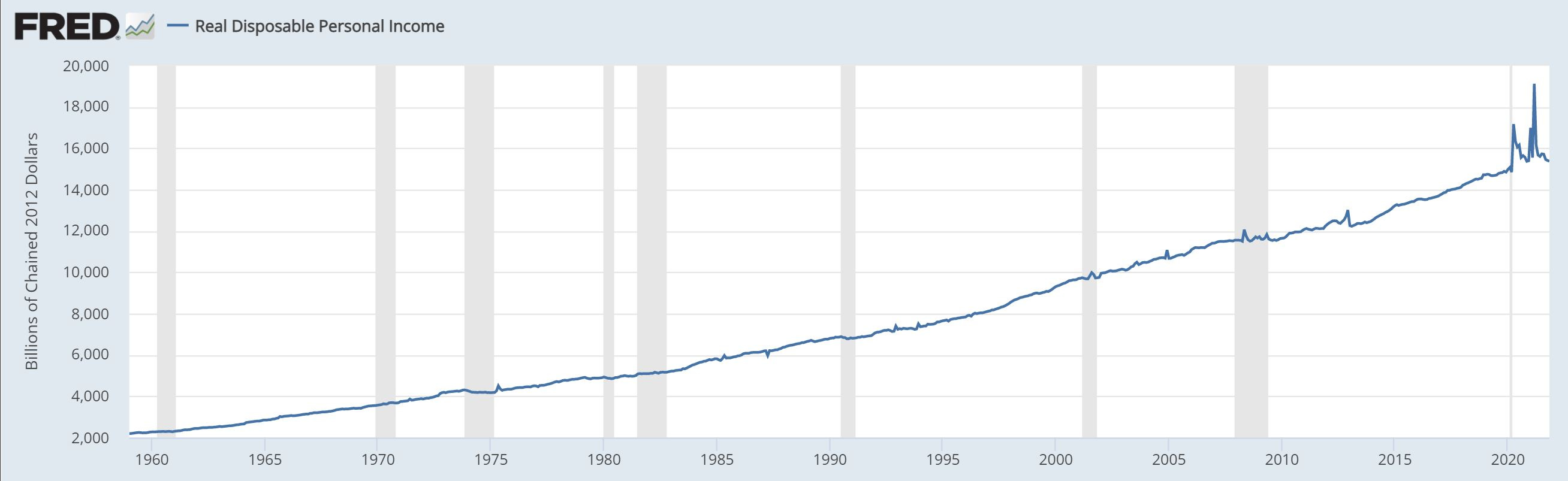

That is real disposable personal income- see anything unusual?

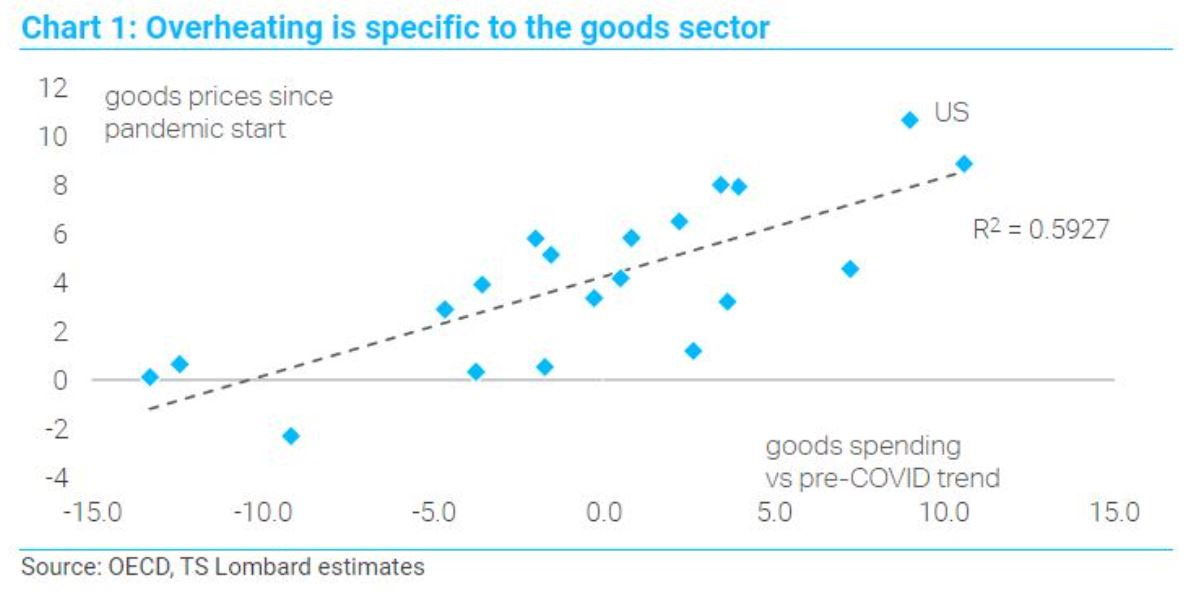

Next, we see how that explosion in personal income was spent- disproportionately on the goods sector. Here was the US versus the rest of the OECD excluding the US:

That shows how much the various government transfer payment programs via huge fiscal deficits in the US drove relative good spending during the pandemic. Surely you have heard about all the supply chain problems, and this dynamic has likely been central.

Not sure how so many seem to be oblivious to Econ 101-level supply and demand curve theory, but shift the supply and demand curves, and guess what is supposed to happen? Prices go up!

This comes back to a fundamental problem with common language surrounding Fed policy, with Quantitative Easing (QE) and Money Printing being used as synonyms by many. The mechanism of QE has been clear across countries for nearly 30 years now- it increases bank reserves and inflates asset prices, but remains ‘trapped’ in the financial system. Yes, central banks exploded monetary aggregates during the pandemic via QE, and we saw the explosion in asset prices globally which resulted. However, many are conflating QE as also having directly caused the increase in consumer inflation.

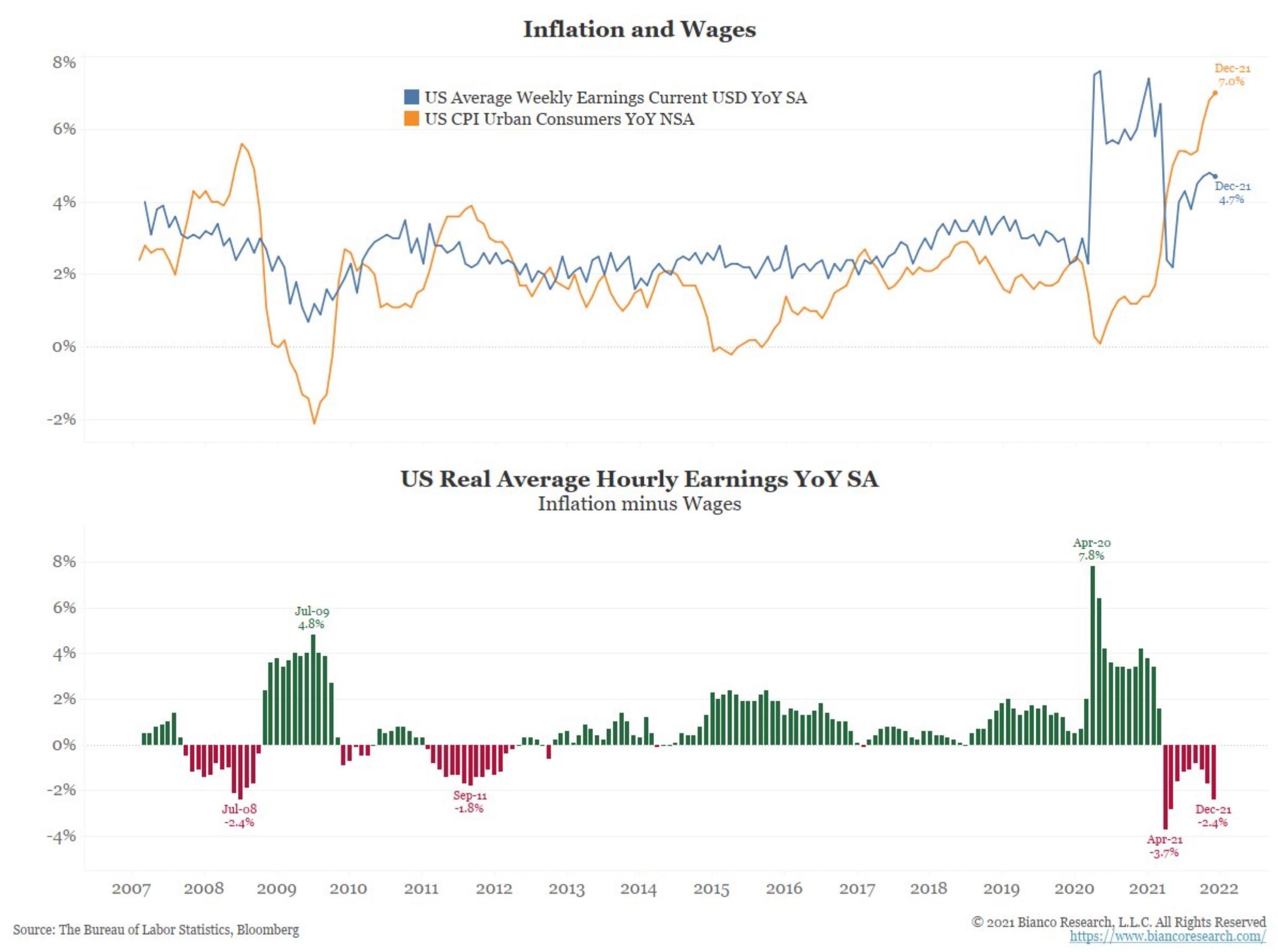

This creates a potentially BIG problem, as the political muscle memory of our octogenarian ruling class seems to have atrophied along with their grey matter. Inflation is a HUGE political problem, and in an election year with the party in power having major polling issues, pressures are further compounded. Here is a graphic reflecting why:

People are really feeling the inflation, as real wages have plummeted, and that is even using the BLS’s phoney baloney inflation data.

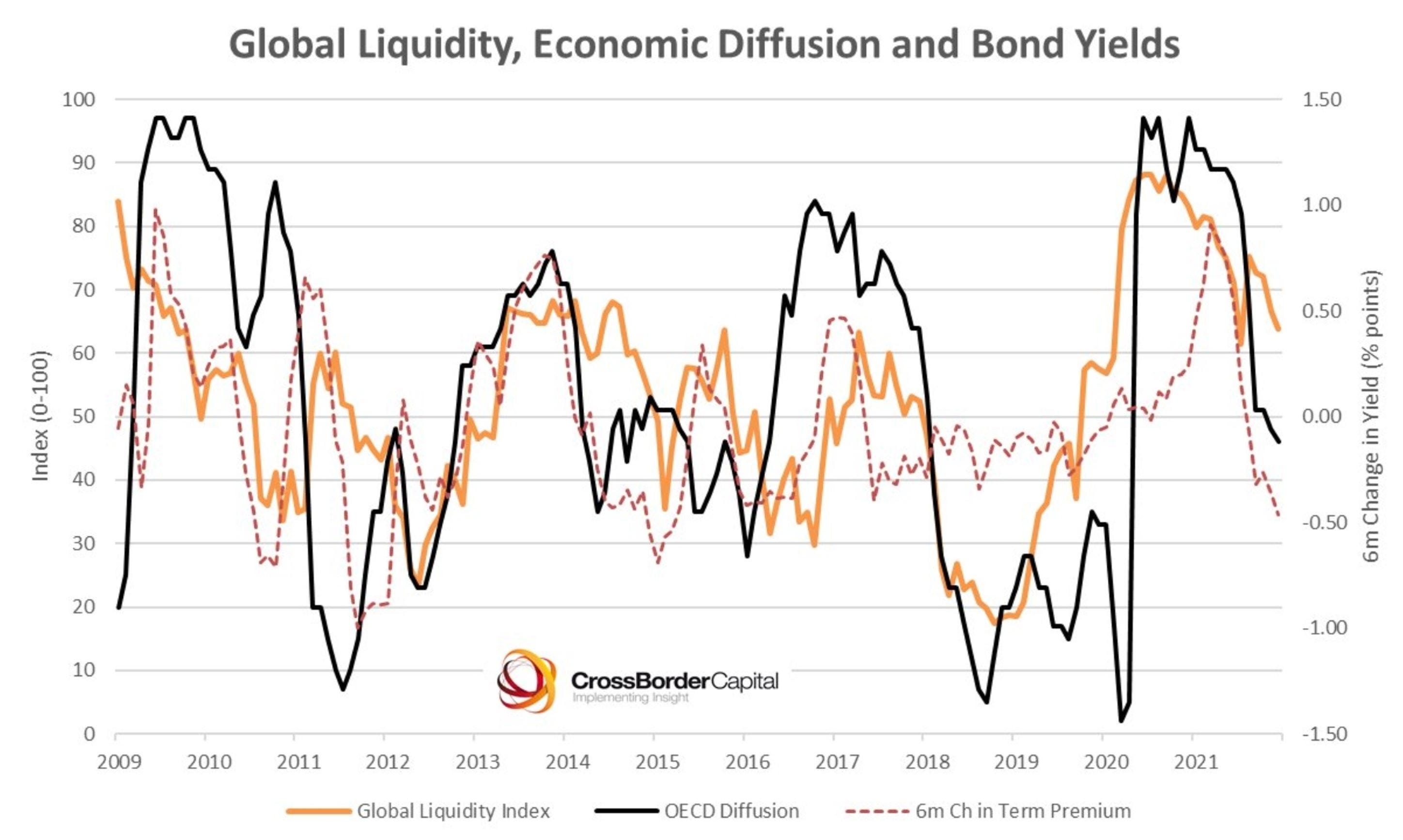

Consequently, we have a major inflation problem in an election year, with massive political pressure growing on the central bank to do something. Unfortunately, they have very blunt instruments with which to act. Here are global financial system liquidity conditions from Cross Border Capital:

Central banks in emerging markets have been tightening for a year, as the shockwaves of US-fueled inflation have cascaded globally and hit those countries the hardest, as it has coincided with a stronger US dollar. Global commodity markets are priced in USD, and staples comprise a far greater percentage of consumption baskets in emerging markets, so the decline in their currencies has started causing real issues. In addition, many finance fiscal deficits via USD-denominated debt. This is the Chilean Peso to USD, with Chile having been one of the more fiscally prudent emerging countries historically:

It is good to see the recent election in Chile has the president-elect focusing on vital matters.

As I have been saying to people with whom I converse, the US is the ‘ass end’ of this business cycle. The ass may be waking up:

That is an index to measure financial conditions- higher means conditions were worse and lower the opposite. The US has just bottomed, but there is a LOT of ‘air’ above.

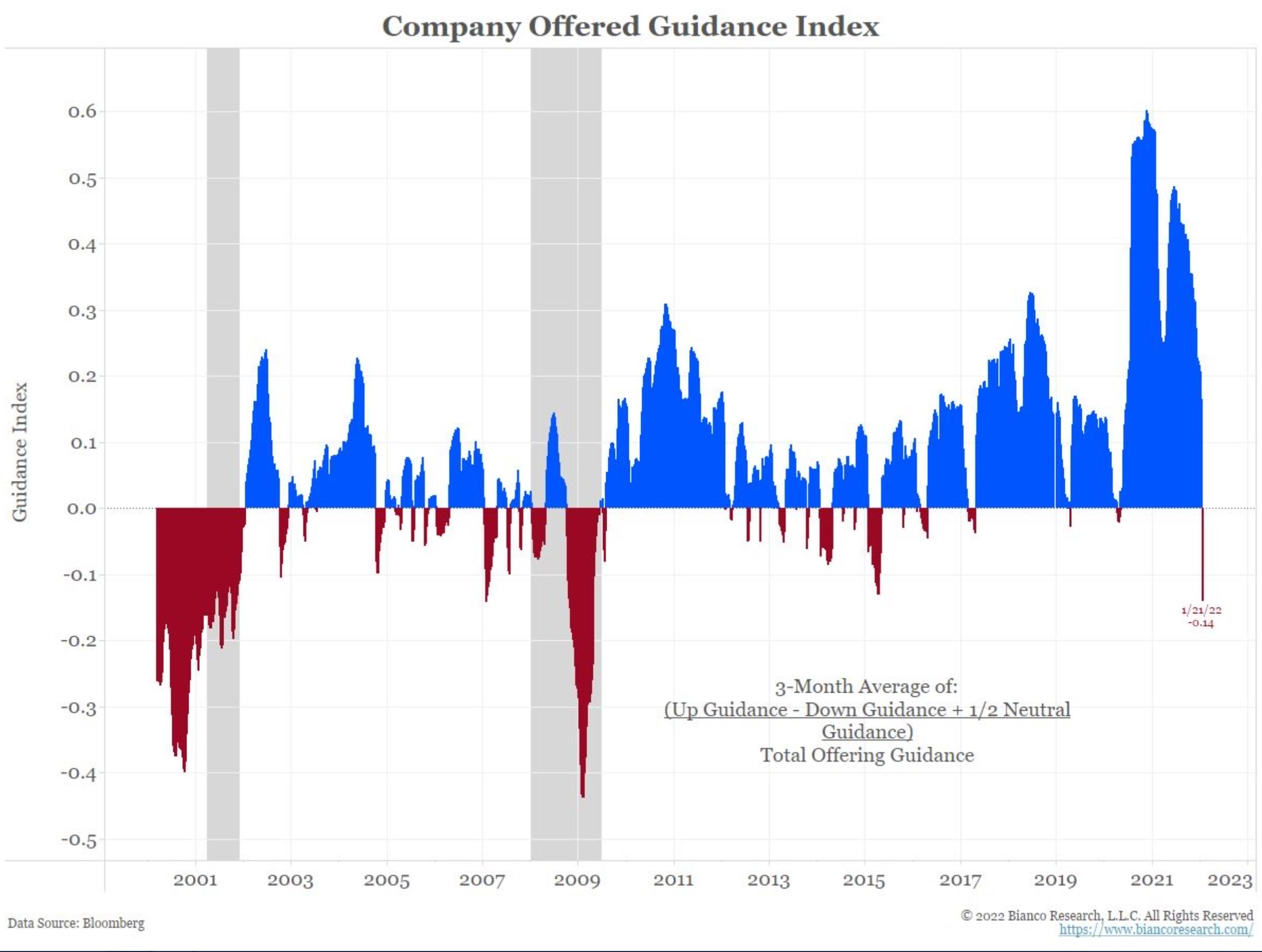

Corporate earnings guidance has just recently flipped negative.

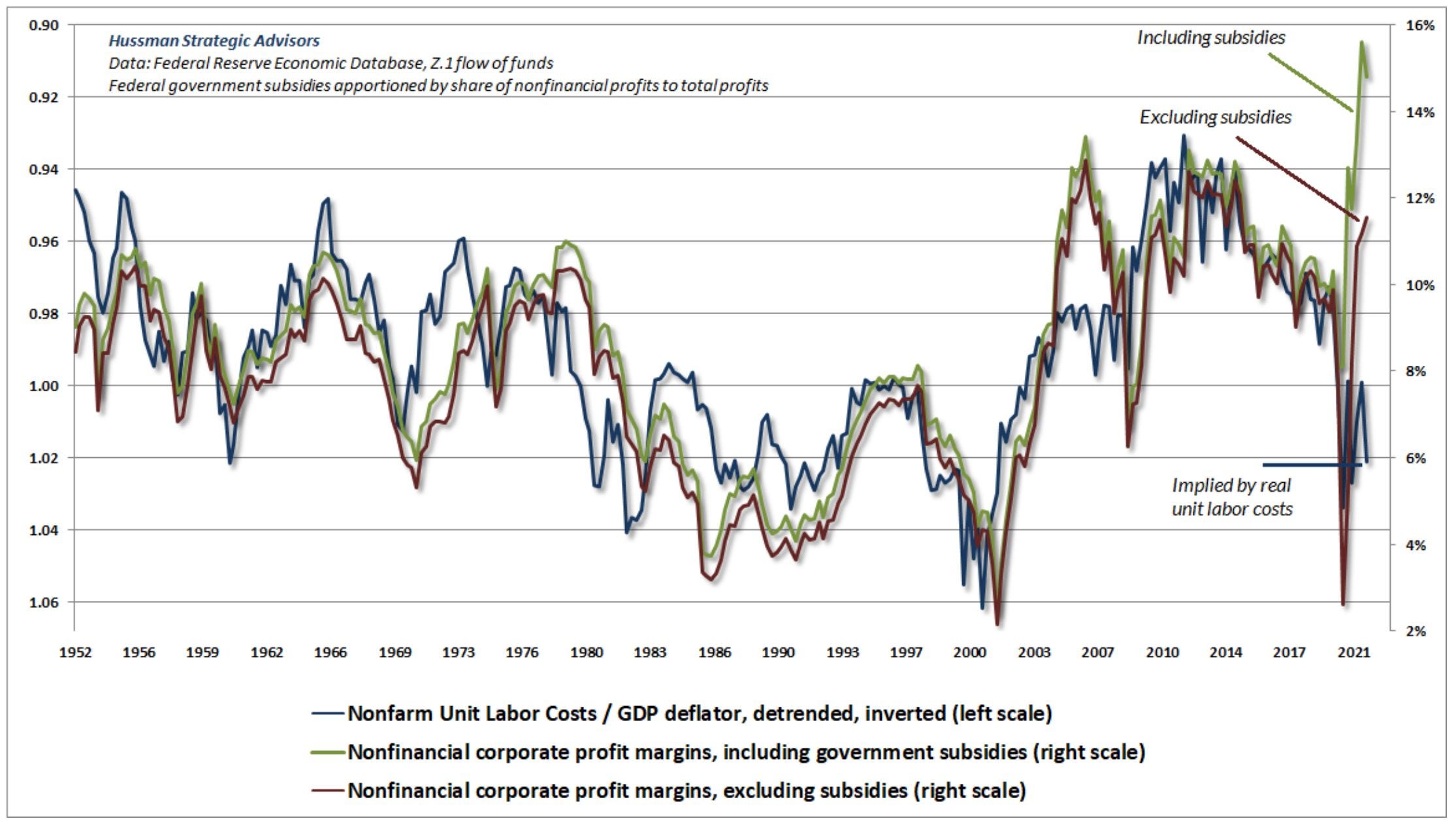

As John Hussman laid out in this recent commentary, all that excess fiscal stimulus during the pandemic made its way into corporate profit margins, and to levels that are very likely to be unsustainable. The prior chart suggests a tipping point may have already been reached, with a lot of room to drop, potentially.

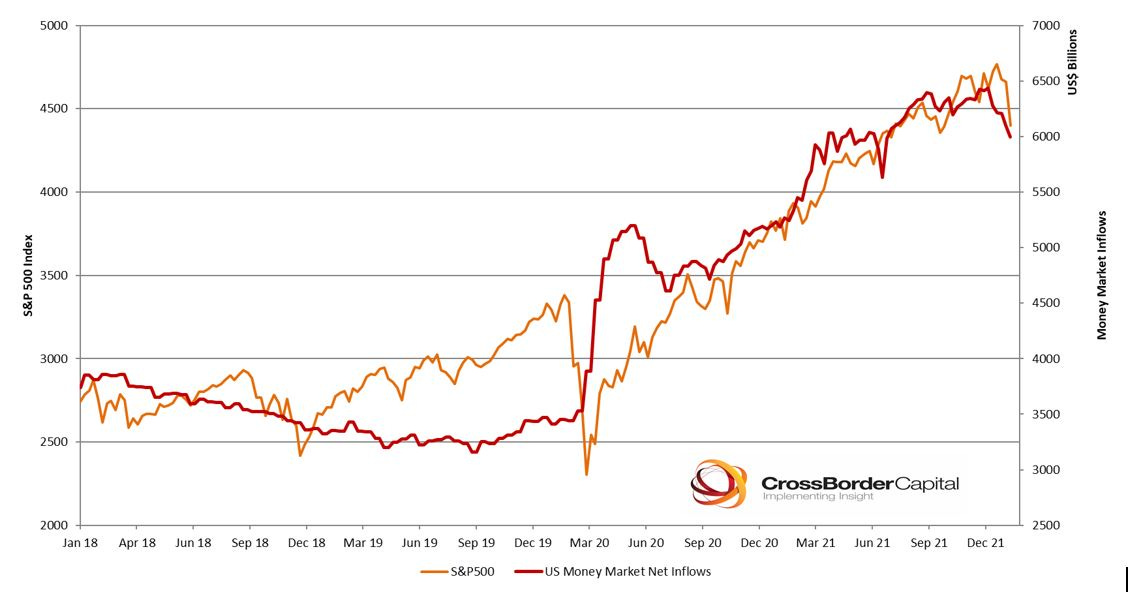

Last year saw record fund flows into equities, and now we see that also possibly just rolling over.

Much will surely be made over the specifics of Fed action or inaction today, what Powell says, and where the little dots are on the plot. However, nothing which happens today is likely to change the following:

The global economy started to slow last spring, the US recently joined, and leading indicators for both continue to point down.

Central banks are usually late and wrong, and most remain in tightening cycles, driving global liquidity down.

The US is the ass end of this cycle, and the Fed has not even really started to tighten yet, but now has huge political pressure to do so.

Despite the recent drop in the major stock market indexes, credit markets and broader financial conditions remain little impacted….so far.

The bulk of the inflation upswing has been due to factors that central bank tightening will not directly impact outside of catalyzing demand-crushing recession.

Asset valuations and corporate profits are coming off record nose-bleed high levels.

I wrote in December about how an ‘avalanche’ of sorts had already started higher up the mountain and that the US remained oblivious to the cascading wall of snow descending upon us. The past three weeks have likely just been the beginning.

This was a slide from a recent presentation made by Lacy Hunt:

This may offer some context as to why the Fed may try to thread the needle by raising rates at the same time as they reduce QE. Unfortunately, this is not a knitting class.

Lastly, bear markets are infamously volatile, with massive counter-trend rallies. Indeed, the largest reversals, up days, and short-term rallies have occurred within bear markets. Sound familiar?

Will there be a ‘Fed put’ to save everyone if this all gets out of control? I have no doubt, but think people have the wrong strike price- it is likely MUCH lower.