Four Legged Table

The current business cycle is unprecedented and quite messy to analyze. I suspect dynamic stochastic general equilibrium economic models may be even worse than usual in trying to forecast such an ‘out of sample’ backdrop. The pandemic period was insane in many ways, but believe the economic implications remain underestimated and widely misunderstood. Here is a series of 5 year charts:

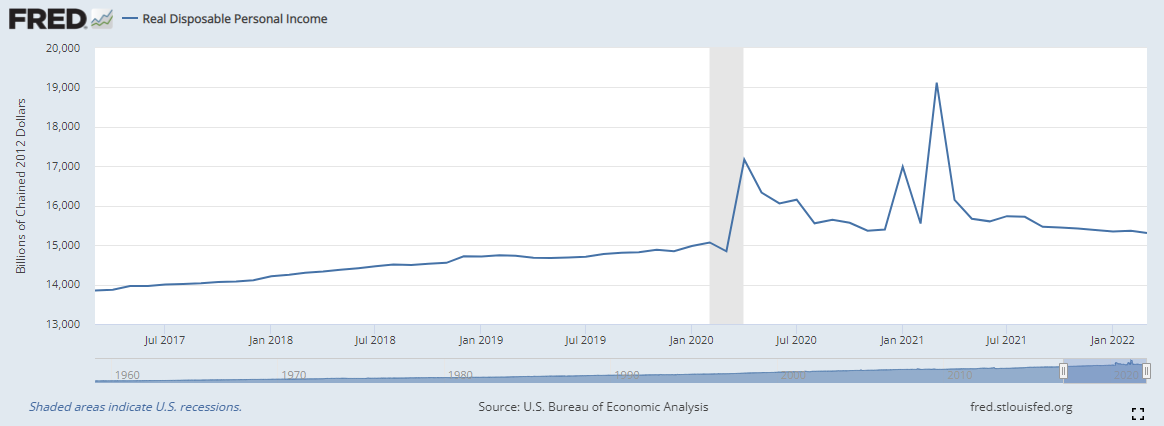

As a reminder from prior pieces, government stimulus did not simply offer emergency support for US households, but rather a financial windfall for over a year.

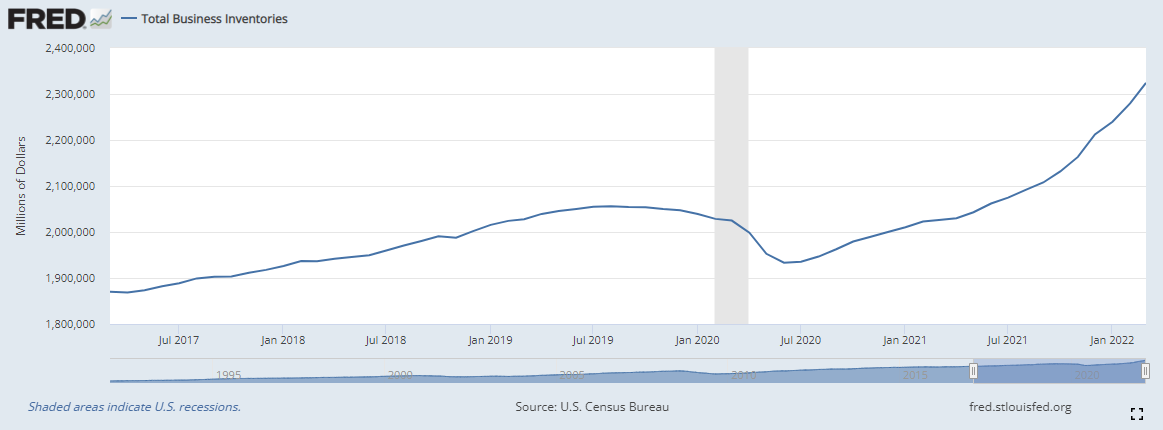

Business inventories dropped significantly, but have been recovering and now moving up at a pretty rapid pace.

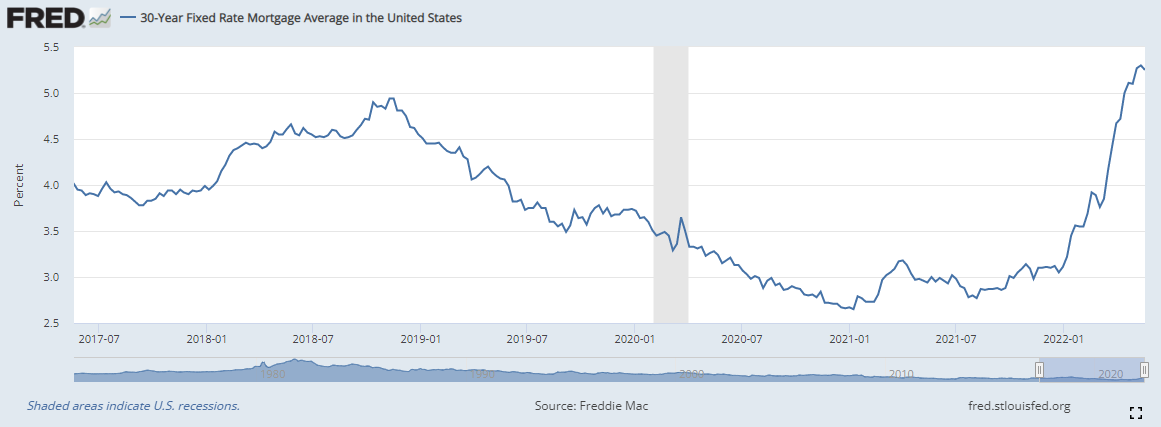

Thirty-year fixed mortgage rates continued the downtrend from when the Fed’s last attempt at tightening ended in capitulation back in December 2018, while renewed QE buying of mortgage-backed securities accompanied a drop to record lows.

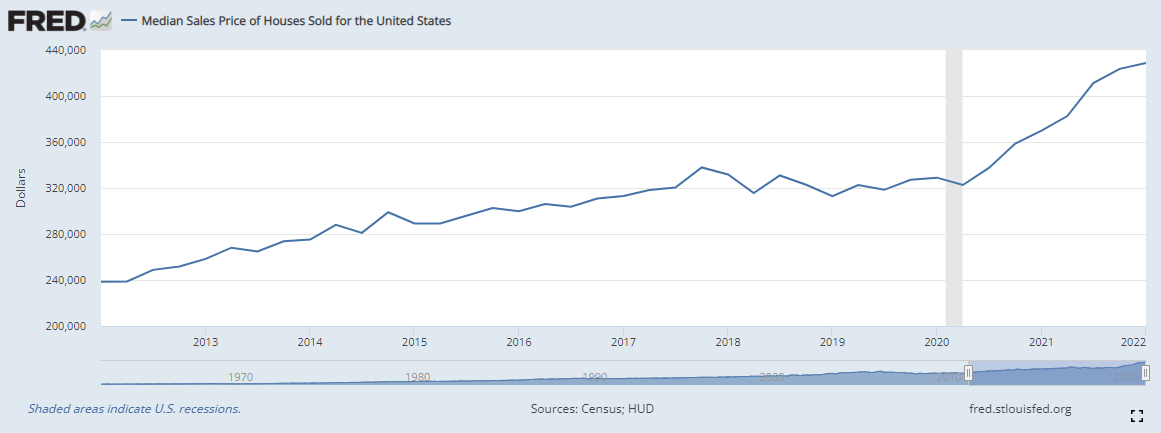

After a steady recovery in home prices coming out of the Global Financial Crisis of 2007-2009, median home prices went into hyperdrive.

But what does this all potentially suggest about the future? Glad you asked!

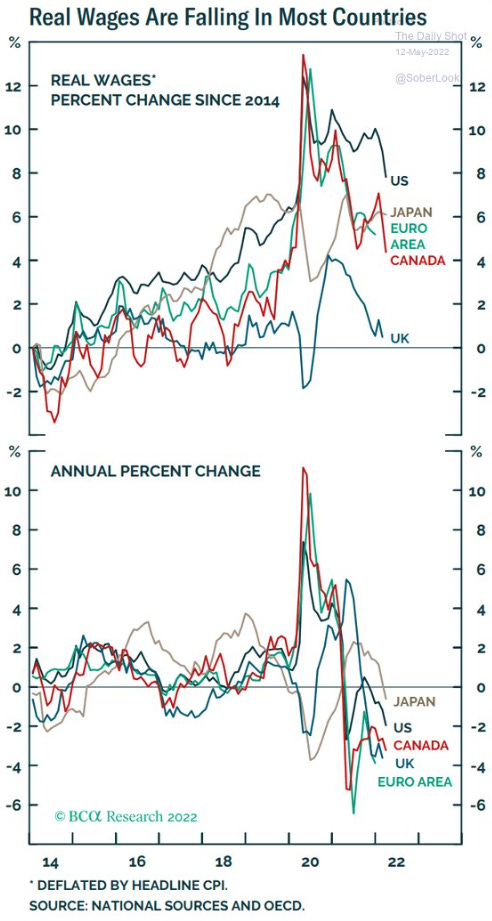

This morning’s German PPI report of 33.5% (holy f*ck!) is just one data point in a broader global mosaic in which consumers have been getting crushed. Remember, many of these CPI metrics are phoney baloney and masking the true extent of the carnage.

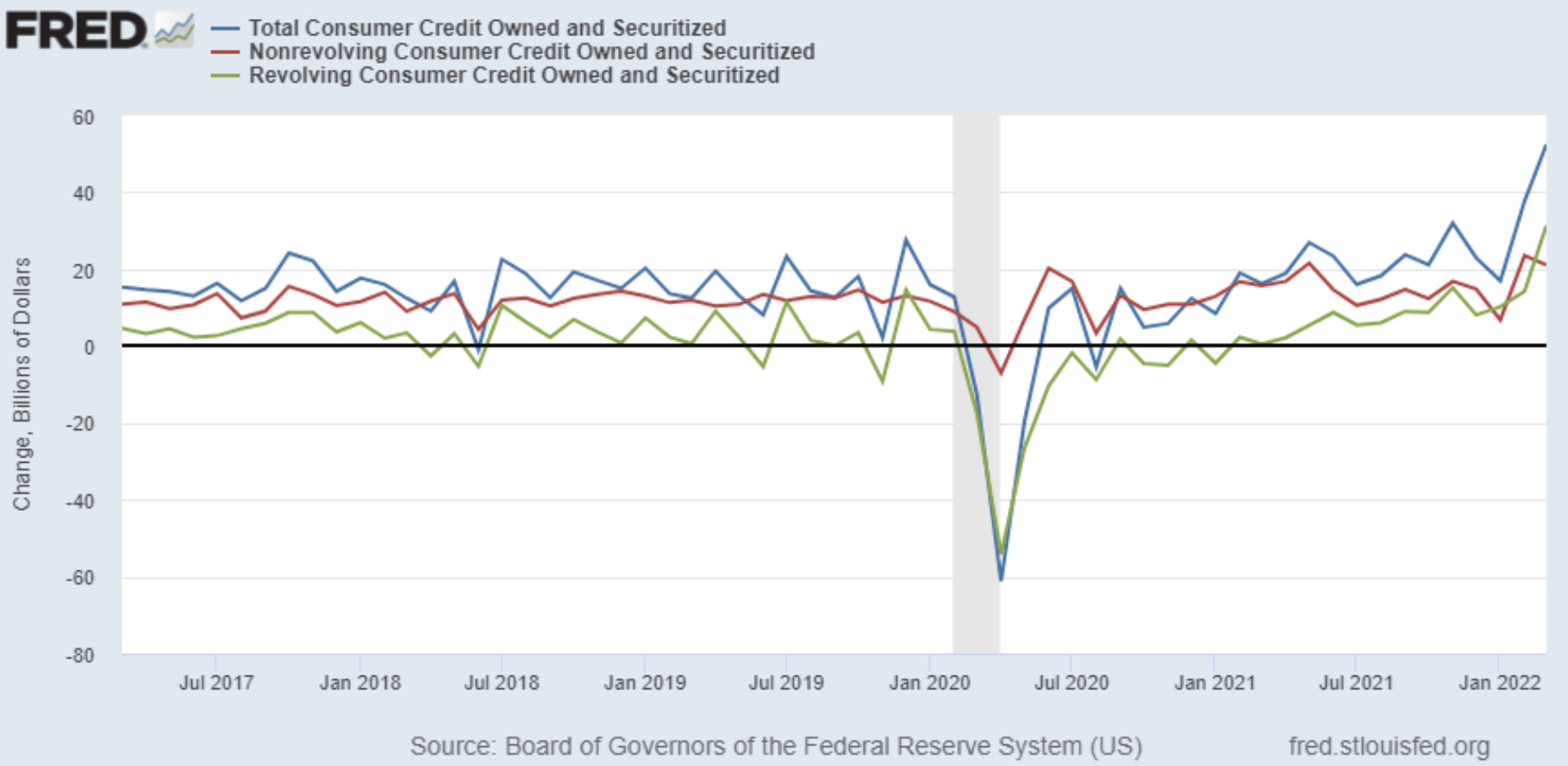

Consumers’ use of credit in the US has turned sharply higher after having plummeted during the lockdown period.

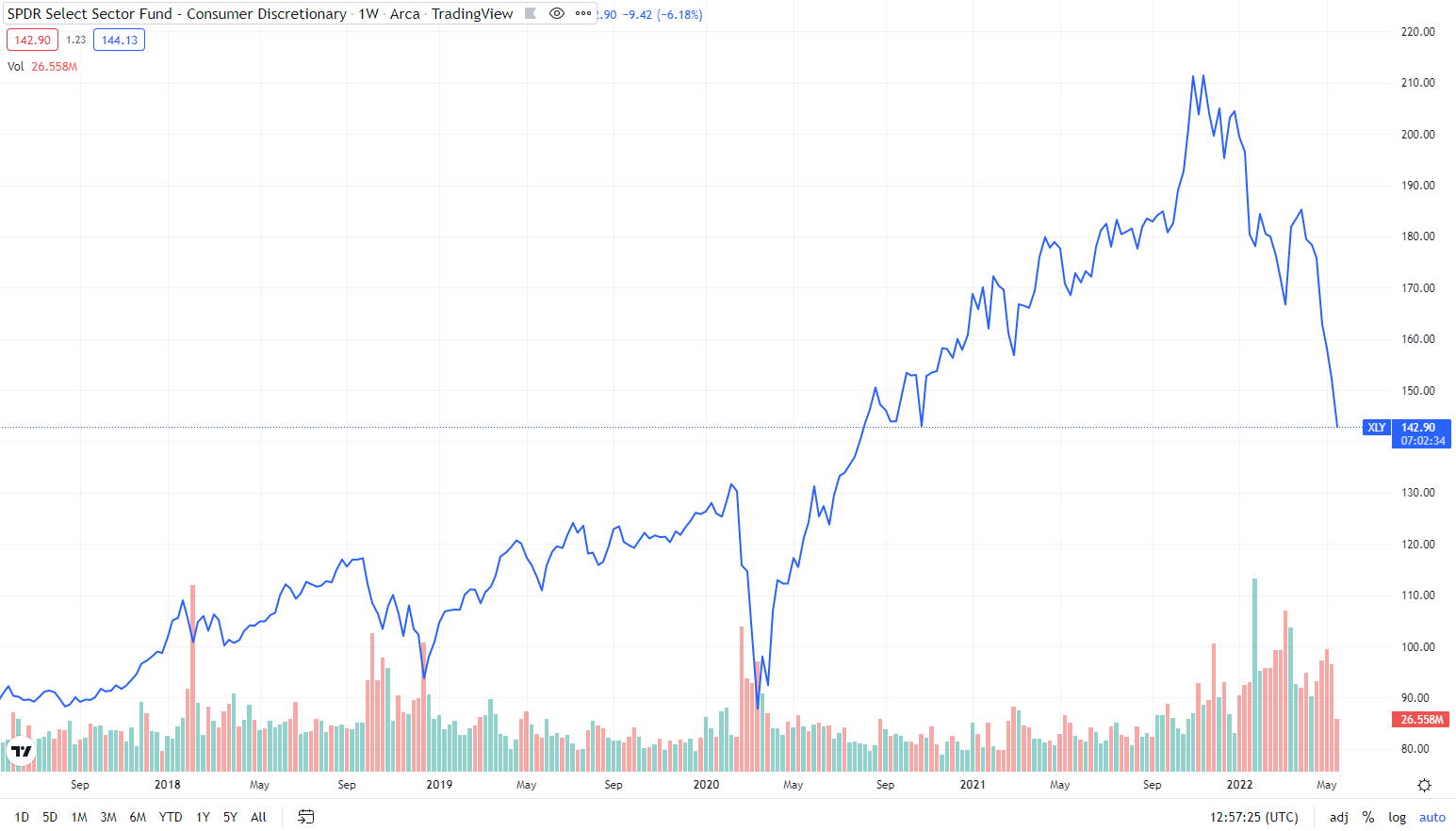

The equal-weighted retail stock ETF, symbol XRT, as well as the S&P 500 consumer discretionary sector ETF, symbol XLY, both rolled over late last year and have accelerated to the downside.

Those are two comparable ETF’s for the homebuilding industry. Here is a sort of intersection between the two, with Home Depot and Lowe’s on the same 5-year weekly chart:

With the four legs of defining the business cycle being sales, income, production, and employment, the first two are already showing significant signs of stress in real terms.

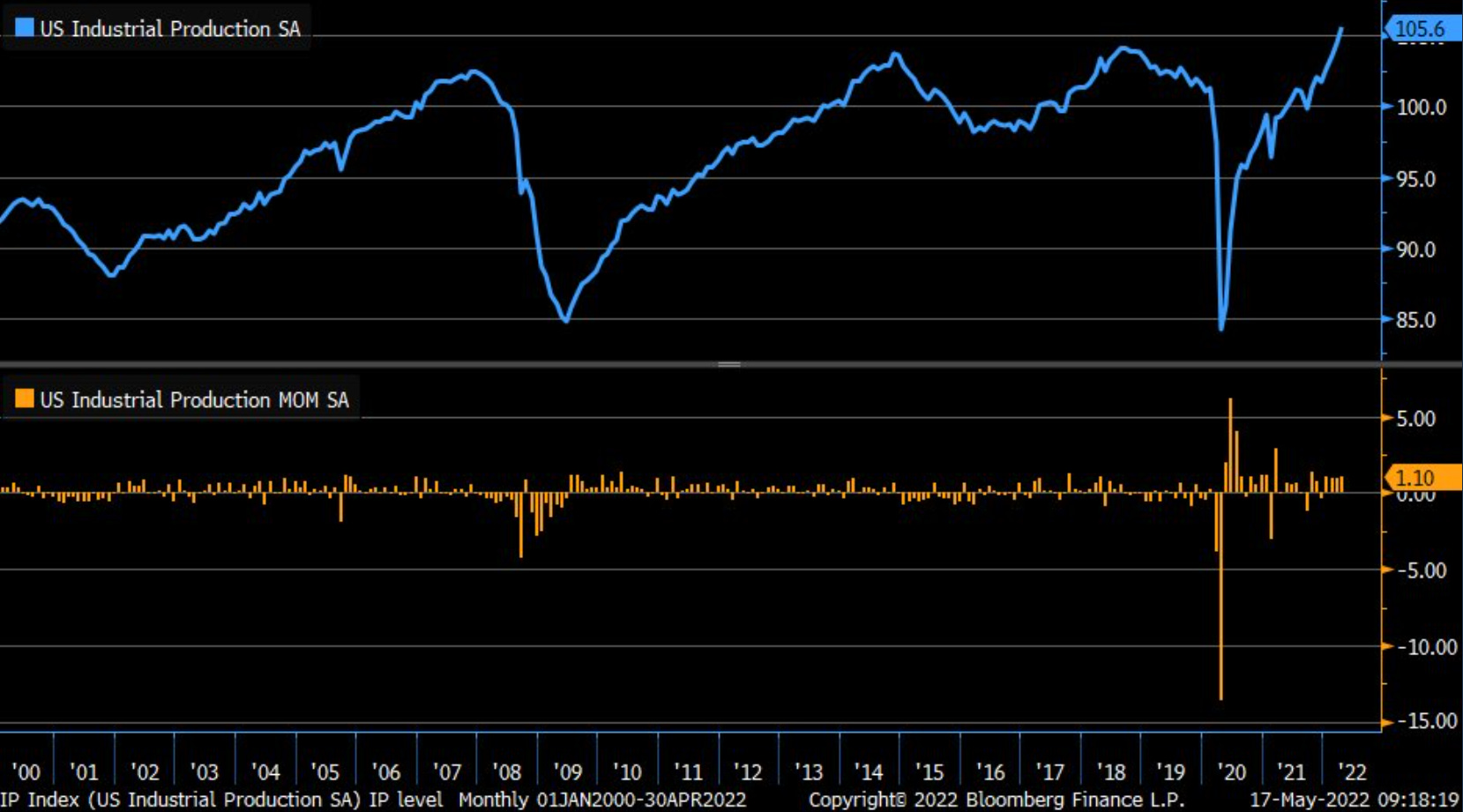

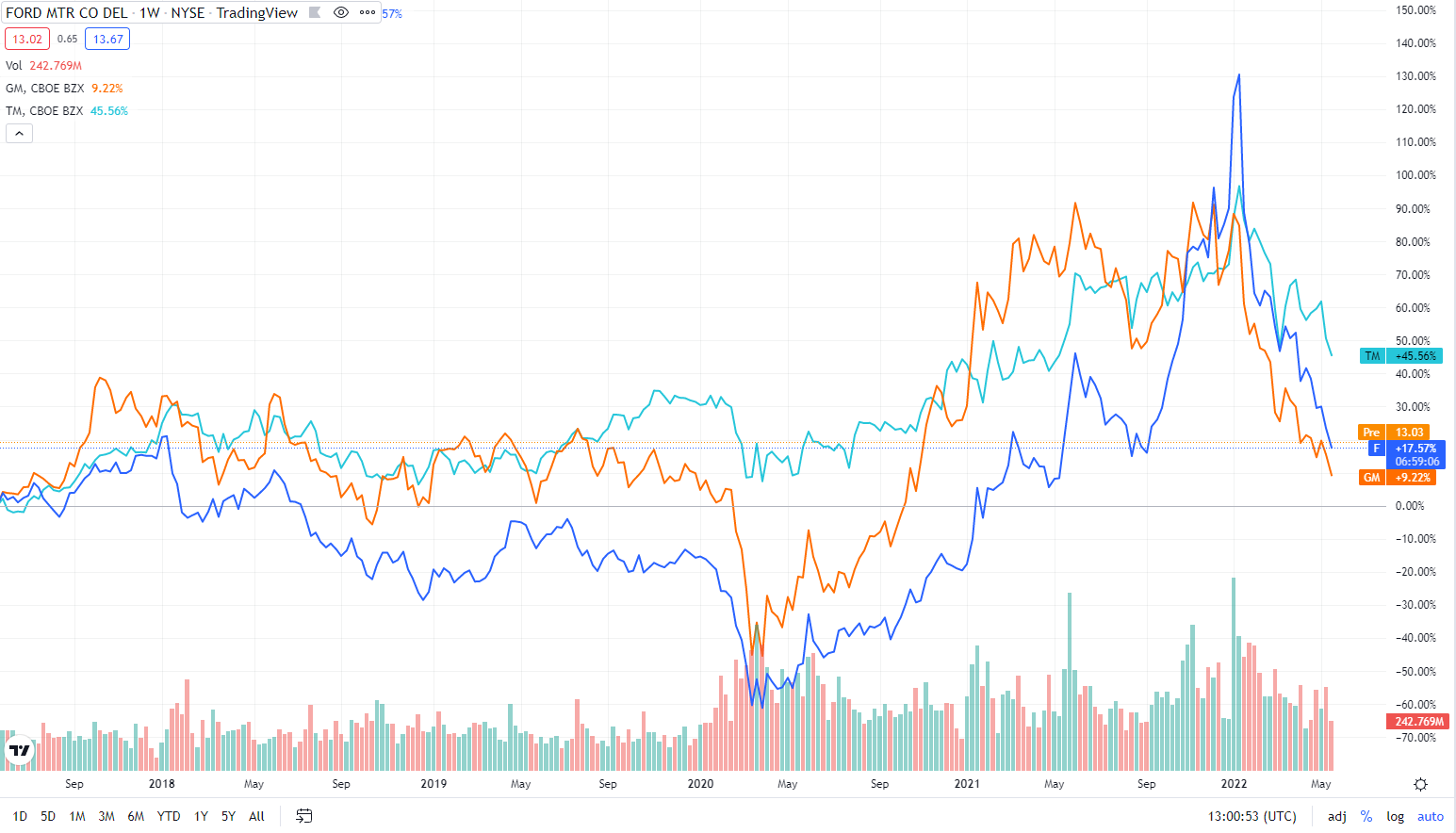

Industrial production has remained in recovery, but remember the inventory situation above. Also, the odd situation in the auto industry due to the microchip shortages should be considered:

Activity has been recovering, yet lookie at Ford, GM, and Toyota share prices:

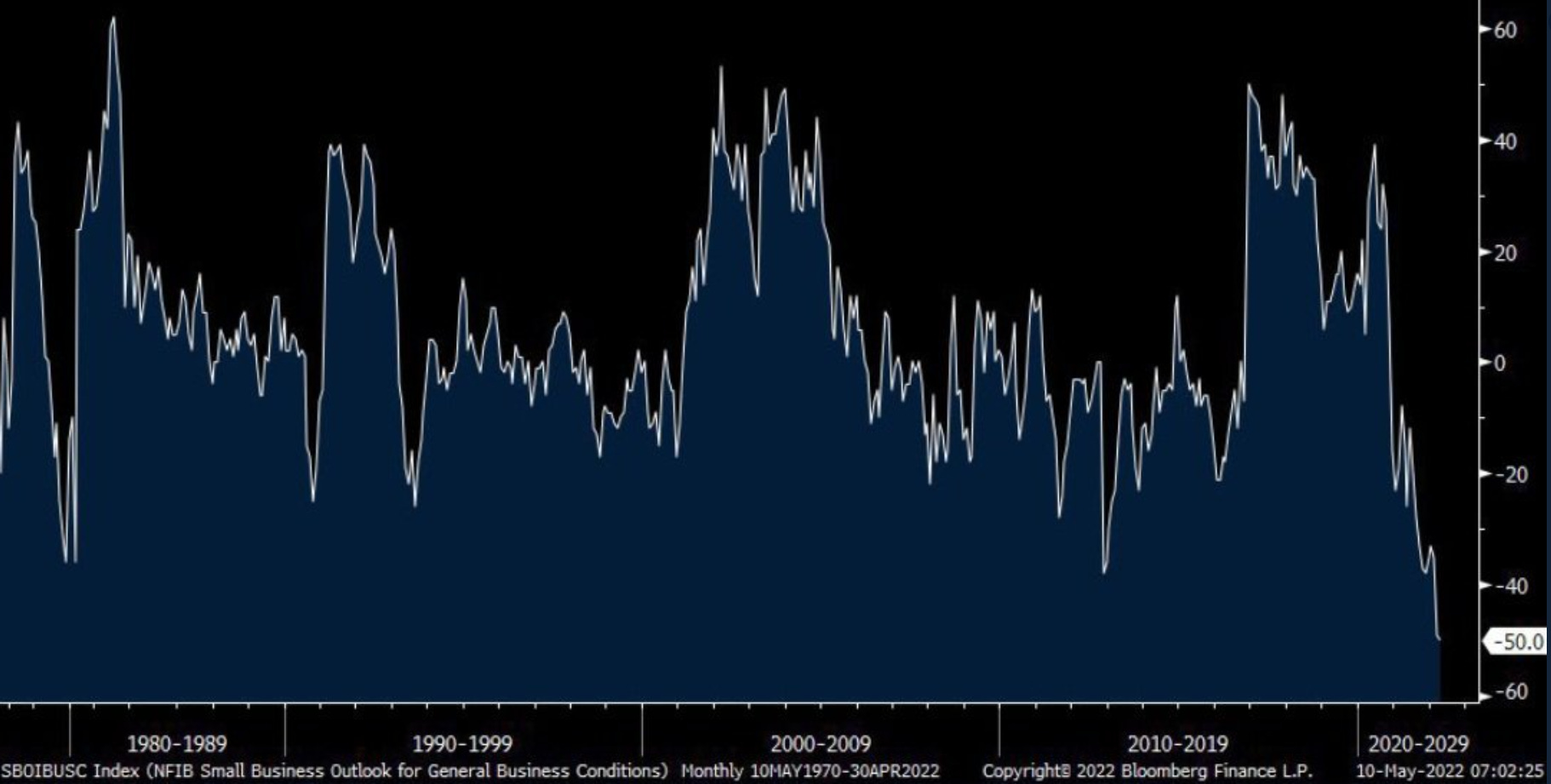

Here is small business outlook sentiment- think we have some inflation and labor market issues?

Does this seem like a recipe for business investment to grow production? Demand is being destroyed by higher prices, and higher financing costs, while profit margins fall amidst a disjointed labor market filled with select shortages.

The acute focus remains inflation, but various areas of the stock market suggest that we may be facing a significant consumer-centric demand problem, with the potential for lagged unemployment to compound the issue. The US consumer has legendarily persisted for many years, to the point where ‘betting against’ them was unwise. However, we may finally be approaching a time when what has been the most resilient of the four legs….snaps.

You are building a case for the collapse in “E”. In the coming weeks/months, which of course makes any sort of discussion about market’s relative valuation today. Majority of today’s “traders” “investors” have no idea about what Mr Market has in store for them