Geek Squad Reboot

Have a confession to make- my family was touring universities last week with our daughter and when the time came to write, I chose the path of procrastination and ultimately rationalization. Apologies: your subscription will be refunded by a prorated amount.

One of the activities in which I have participated as part of launching this letter and the related Twitter account last year has been Twitter Spaces. In particular, George Noble has been holding regular Spaces, and next Thursday’s scheduled guest is Lakshman Achuthan of the Economic Cycle Research Institute (ECRI).

I mention this because ECRI is part of my Circle of Trust, as laid out in the introductory post of this letter. Today’s letter is dedicated to my current thinking on the business cycle, as I look forward to hearing Lakshman on Thursday, and hopefully getting an opportunity to ask him a few questions. For those interested, I strongly encourage you to listen to Lakshman’s recent appearance on this podcast, as it offers a good introduction to ECRI and its analytical process.

There are roughly 130 independent currencies globally and over 190 nation-states. With varying levels of interest rates, currency values, natural resources, human resources, financial resources, etc., the business cycles of nations and regions typically vary.

At times there are global expansions when the broader economic pie is expanding with broad participation in growth, but there are also periods when nations/regions are at different cycle stages. Some can be growing while others contracting, while still others just slowing or accelerating. The dispersion and variability in direction and rates of change all create a sort of robust system-wide stability.

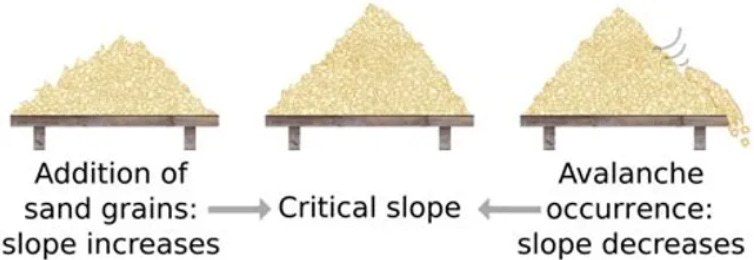

Many modern economists have gleefully supported globalization, and there are certainly many benefits. However, as we have seen over the past 2+ years, those benefits also come with some issues. From a complex system perspective, it has likely increased the fragility of the broader economic system. To put it another way, it has allowed the size of the Sand Pile to grow significantly.

This was made clear as global supply chains seized up during the pandemic, with the Fed and many mainstream economists underestimating the forces being unleashed due to this fragility/complexity. I believe they are making a similar analytical mistake as relates to the broader business cycle. The US business cycle is part of the broader global Sand Pile:

During most localized or regional business cycle contractions, or Sand Pile avalanches, the ramifications do not result in the larger pile collapsing. For example, even in 2008-2009, significant areas of the world such as China and India only slowed as the US-centric portion of the Pile avalanched. However, their relative resilience helped the broader system be less fragile despite a large chunk of the Sand Pile cascading.

Fast forward to 2020, and the business cycle Geek Squad arrived:

The interconnected nature of the globe brought about the world’s first major pandemic in the era of hyper-globalization. Regardless of one’s views on the relative wisdom of various policy responses, the reality was that lockdowns served as a sort of global reboot of business cycles around the world. It was as if everyone’s RAM got full in a relatively short period of time, and nations/regions unplugged and then plugged back in their business cycles.

This synchronicity created all sorts of issues as economies rebooted, including the global supply chain and inflation crises. The subsequent response has been a synchronized move to tighten all the liquidity which had been added in response. This setups up a scenario which reminds me of this Billy Joel chorus:

As referenced in this letter from June 24th, ECRI had indicated publicly that their leading indicators had turned down in a way not seen since the last synchronized global recession, which was over 40 years ago. Combined with a Sand Pile view of the world, I am probably way out on a limb in terms of the risks associated with current system dynamics.

The fiscal policy responses to the GFC and pandemic resulted in an explosion in debt levels around the world. The monetary policy of financial repression compounded this economic leverage with financial leverage, as the combination of low rates, low volatility, and low levels of consumer inflation incentivized leverage.

What we know from complexity is that when these forces are unleashed, they tend to follow power law dynamics/non-linearity. Phase transitions to chaos occur as sections of the Sand Pile crumbling begin to weaken more of their ‘neighbors,’ with this process going from what looks like relative stability to instability fast.

I remember the 2008 cycle vividly, as I had rotated what short/hedging exposure I had from financials-centric to small caps and emerging market stocks following the Soc Gen and Bear Stearns bailouts. The next few months were shear misery, as the Sand Pile took its good old time getting to its phase transition to chaos for those market segments:

Given the hypercriticality of the Sand Pile heading into this avalanche, both economically and financially, those expecting to ‘hide’ in the areas holding up so far, may just be delaying the inevitable.

Tune in to George’s Space on Thursday if you are interested and able. I hope to get an update on where ECRI’s forward-looking indicators and analytical process are relative to my Sand Pile framework.

Next week, I may take a look at one specific hiding spot, assuming another bout of procrastination does not occur- not sure I can afford all these refunds, so…..

Great post king kayfabe!

Globalization, as currently defined, ended first with the kinetic WWI (as an aside, believe Germany wanted war and was not an "accident" of treaty obligations). The second ended recently as the American sponsored model of "free trade" became incongruously apparent that it had been gamed by EM (read China) and others to their one-sided advantage. Not the end of the world but a reordering on deck.