Hershey Highway Investing

Hershey Highway Investing

Company vs Stock

My first full-time job as a teenager was working a summer job at Hersheypark (owned by Hershey Entertainment), with The Hershey Company’s (NYSE:HSY) nearby chocolate factory cranking out a sweet daily plume of scents from various iconic brands being manufactured.

Milton Hershey endowed the Hershey Trust, which provides resources for the Milton Hershey School, with approximately $60 million in 1918 and has grown to over $17 billion according to Form 990 from 2020. My guess is it is materially higher now, as the Trust retains a large minority position in HSY, though has been diversifying its super-voting rights shares with systematic sales. HSY’s price has nearly doubled since the fiscal 2020 year-end in the report for July 2020:

Regrettably, I was not wise enough as a teen to invest any of my $3.35 per hour in wages that summer. The stock has appreciated a lot since having gone up 23 times vs where it was during my summer employment in the early 1990s. The buy-and-hold return works out to about 11% per year over the period, plus a consistently increasing dividend.

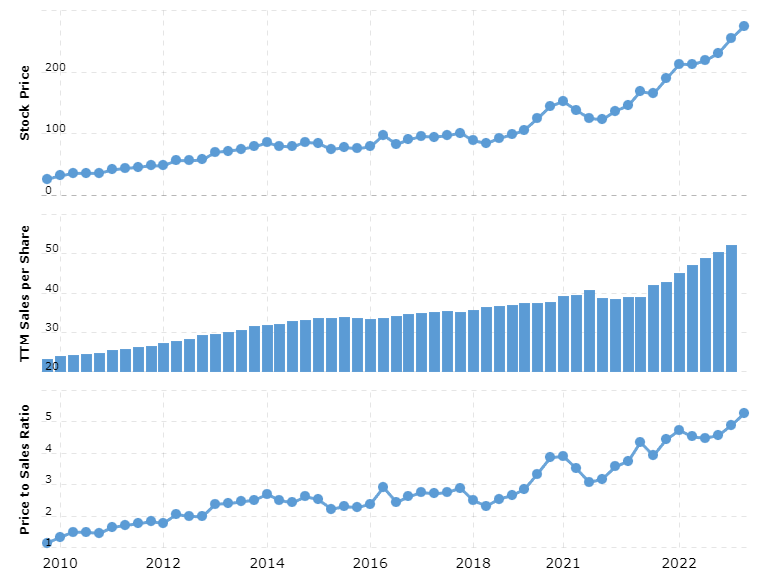

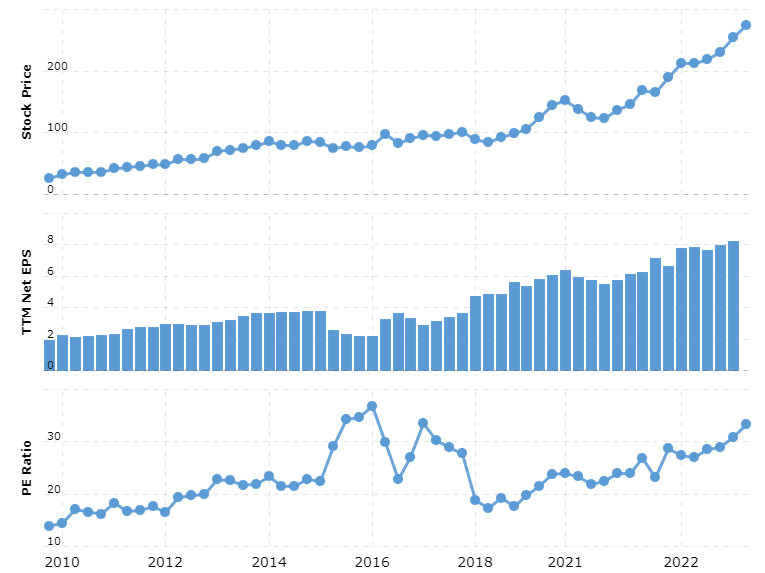

But as they say, past performance does not guarantee anything as to the present or future, and the stock is emblematic of the rush into the stocks of high-quality companies over the past couple of years. A great company does not necessarily make for a great investment if the acquisition price is very high. Here are graphs showing Price-to-Sales and Price-to-Earnings for the stock since the end of 2009:

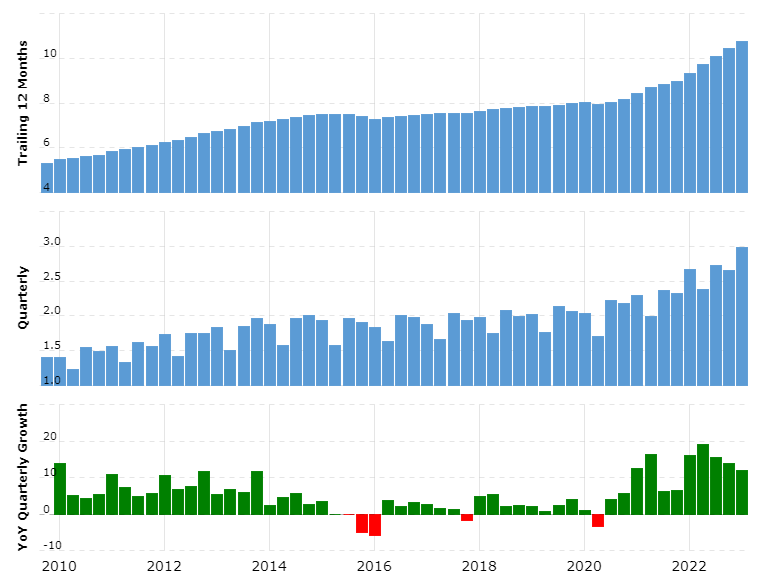

Here are operating and net profit margins over the same period:

Here are revenues and shares of stock outstanding over the period:

We can see from the graphs that revenues grew at about a 4% average annual rate for the ten-year period that preceded the onset of the pandemic and has subsequently grown at over 9% in the three-year period since. Operating and net margins have expanded during this inflationary period, and the company’s profits have benefited. In addition, the company has been engaged in a systematic buyback program for most of the past decade, with reduced share count further goosing the growth in earnings per share (EPS).

Obviously, as Yogi Berra once said, “It’s tough to make predictions, especially about the future.” Rather than predict, here is some simple scenario analysis to try and gauge what sort of margin for error is currently priced into the stock, which just reached a new all-time high on May 1, 2023.

As we can see from the revenue growth figures above, HSY has been around a nominal-GDP grower, meaning that over time its revenues typically grow roughly in line with inflation. Again, just as an exercise, let us assume that the ten-year period starting from December 31, 2022, sees HSY revenues growth at 4% per year, as they did from the ten-year period that preceded the pandemic.

In addition, if we apply a 12% net margin, which is around the midpoint of the range since 2009, that would place trailing 4Q 2032 earnings at about $1.85 billion. If we assume that the company continues to buy back 2% of the shares outstanding each year, that would take the share count down from about 206 million to 168 million. Dividing the two numbers would give us a trailing 12-month EPS figure of $10.99 for 4Q 2032. Again - this is not a forecast.

With Q4 2022 EPS already in the books at $7.96, these assumptions would result in a compounded EPS growth rate of just under 3.3% per year. Of course, this introduces the question as to what multiple to sales or earnings investors may apply in the future.

During the pre-pandemic period of ZIRP (zero interest rates), HSY’s price-to-sales had drifted up towards three. Applying that multiple to 2032 sales of about $15.4 billion (2022 was $10.4) is a market capitalization of about $46.2 billion. Divide by the reduced share count of 168 million, and we get $275 per share. For perspective, the last trade in HSY as I write this piece is $274.86.

If we assume a price-to-earnings ratio of 20 on the $10.99 EPS figure for 2032, which again was relatively typical during the pre-pandemic period, we get about $220 per share. This sort of exercise suggests that even using what I believe are reasonably sanguine assumptions, there is not much margin for error priced into the current stock price. In fact, it appears to me to be a potential recipe for returnless risk from the current starting point.

History offers various examples to examine. For example, Warren Buffett’s famous investment in Coca-Cola (NYSE:KO) in the aftermath of the 1987 crash, along with an additional stake taken during the mini-equity bear market in 1994, had appreciated massively by 1998:

I have drawn in horizontal blue lines as to the areas of price in which Buffett had taken his huge stake, and then where the stock peaked in 1998. The stock went up over 20 times in price from the post-1987 crash level by mid-1998 and was trading at valuation levels that HSY and many of its ‘high quality’ brethren echo currently.

The subsequent period saw KO grow its revenues and dividend consistently, continuing to be a high-quality business and reasonably well managed by all accounts. Yet, the stock price turned into what amounted to returnless risk for two decades. In fact, the pandemic-induced market panic in March 2020 saw the price of KO fall below where it was in 1998!

Buffett wrote this in the 2003 annual report for Berkshire Hathaway:

We are neither enthusiastic nor negative about the portfolio we hold. We own pieces of excellent businesses...but their current prices reflect their excellence. The unpleasant corollary to this conclusion is that I made a big mistake in not selling several of our larger holdings during The Great Bubble. If these stocks are fully priced now, you may wonder what I was thinking four years ago when their intrinsic value was lower and their prices far higher.

The price of KO had declined to about half of its 1998 peak by the time Buffett penned that letter.

In this era of mindless passive index flows, quantitative strategies chasing price momentum, and an equity options market mania unfolding, thinking about these sorts of old school fundamentals may not assist with speculation and selling shares to a greater fool.

In addition, today’s missive, despite the walk down memory lane for me, is not actually about Hershey’s stock. Rather, the stock is an example of a class of ‘high quality’ stocks in which investors have been increasingly ‘hiding.’

The Nifty Fifty and many other lessons of the past are regularly ignored only to be relearned by investors. I have no idea where any of these anointed stocks may trade in the coming days, weeks, or even months, but unless the lessons of history are finally ‘different this time,’ long-term investors may be setting themselves up for an unlubricated journey on the financial Hershey Highway in the coming years.

Graham works well to ballpark equities like this. Using your numbers and a 5.5AAA (WAG because the thing doesn't really exist anymore) Graham spits out 96.