Inadvertently McFlying

Inadvertently McFlying

1.21 Gigawatts Back to 1920

One of the phrases I am fond of using is to describe the modern practitioners of economics as flat-earthing astrological alchemists. I wrote about some of this back in the Do You Have LSS? post from June 2022. In my view, modern economics has morphed largely into various ideologies debating how to best centrally plan the economy and fight market forces. Basically, we have a bunch of so-called free market advocates who do not actually want market forces to be left to work their ‘magic.’

This migration to Politburo-style central planning of the economy exploded during the 1930s, as the Great Depression offered the kind of terrible human suffering, similar to COVID, where federal governments around the world were able to push boundaries on what had been norms prior to the crises in order to acquire power.

This cycle has been, and remains, such a fascinating confluence of various historical extremes that it is easy to extract lessons from all sorts of prior periods. While many remain fixated upon the 1970s and the associated inflation crisis and related bond market wreckage, the real Negative Nellies often reference the early 1930s while they await a deflationary bust.

Today, I borrow Doc Brown’s Delorean and ride with Marty McFly to a decade prior to the onset of the Great Depression - the often-forgotten Depression of 1920-1921.

I will forgive those readers who have no knowledge of that Depression or never even knew that it occurred. For reasons that will likely become self-evident, it is not one to which modern economics are apt to reference.

The Great War had just recently ended, and the Spanish Flu pandemic was winding down in its fourth wave, as the Depression kicked off in early 1920. Following the Panic of 1907, JP Morgan had had enough of bailing out the financial system, and the latest attempt at a central bank was finally realized, with the Federal Reserve Act in 1913. The new central bank was stress-tested quickly, as US entry into the Great War was accompanied by amendments to the Federal Reserve Act that enabled the Fed to nearly triple the amount of currency in the system to assist with funding the war effort.

Federal debt as a percentage of GDP went from less than 3% prior to entry into the war to around 30%, which was comparable to the levels reached during the Civil War. The nation remained deeply skeptical of centralized federal power, but the incrementalist approach made huge strides in the decade preceding the 1920-1921 Depression, with the Sixteenth Amendment enabling a federal income tax ratified in early 1913. Those greedy politicians set the top tax rate at 7%.

The economy experienced various shocks, obviously, and with the combination of returning soldiers looking to reintegrate into the labor force, over 600,000 people perishing in the pandemic in the US, and labor unions asserting power, cross-currents following the war and pandemic were severe.

With what at the time was considered high levels of federal debt, the first major economic contraction the Federal Reserve faced was greeted in a way that would be viewed as heretical today. Throw in the response by Congress, and it is quite possible that modern economists’ collective head could spontaneously combust from examining the cycle.

The Federal Reserve raised interest rates starting in 1919 and persisted into mid-1920. Here is a graphic from a 1965 paper showing corporate borrowing rates from the period:

With the economy in severe contraction and consumer prices deflating by double digits, real interest rates exploded for businesses. Consumer financing was a banking innovation that would not gain significant traction until later in the decade, so higher rates mostly impacted businesses.

Oh, but dear modern economists, the bad news did not stop there! Guess what the early 20th-century troglodytes in Congress did? The maniacs cut federal spending by over 65%!!! Surely, based on the work of economists ranging from Milton Friedman to John Maynard Keynes, these policy responses must have resulted in the worst economic period in history - what MORONS!

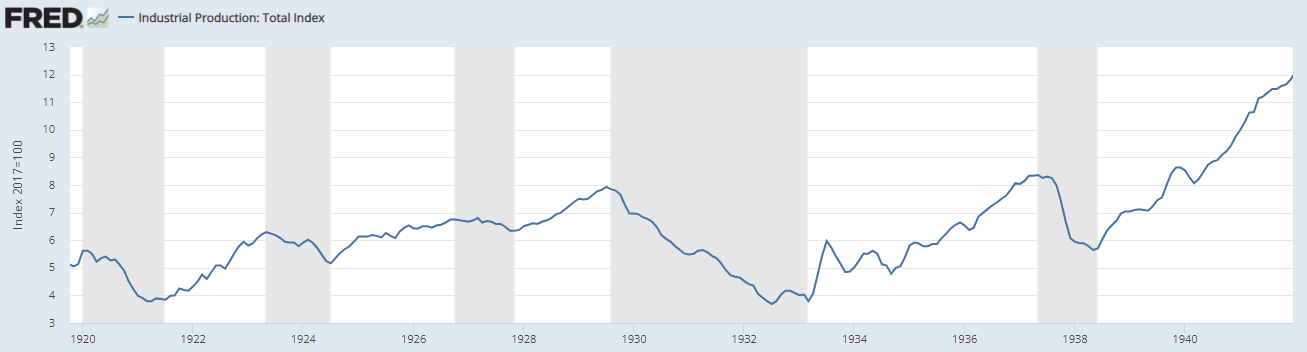

The breadth of economic data from the era is relatively limited compared to what our modern rocket scient…I mean economists get to work with, but here was industrial production from post-Great War up until the start of WWII. Yes, the Depression of 1920-1921 was vicious and terrible, to which the term “depression” may have offered a clue.

However, the subsequent recovery was significant and diffused across the economy. The horrible cross-currents of the post-war period were resolved via the sharp and painful reallocation of resources within the economy. Rather than a centrally planned economic Politburo, markets, and the private sector were generally left alone, especially compared to modern conventions.

We can see that the level of industrial production exceeded the pre-Depression level in 1923, and the unemployment rate dropped from around 10% back to below 3% quickly - again, the data collection and reliability were spotty so keep that in mind.

By comparison, the MASSIVE response by the federal government to the Great Depression coincided with industrial production failing to durably eclipse the 1929 peak until the onset of WWII.

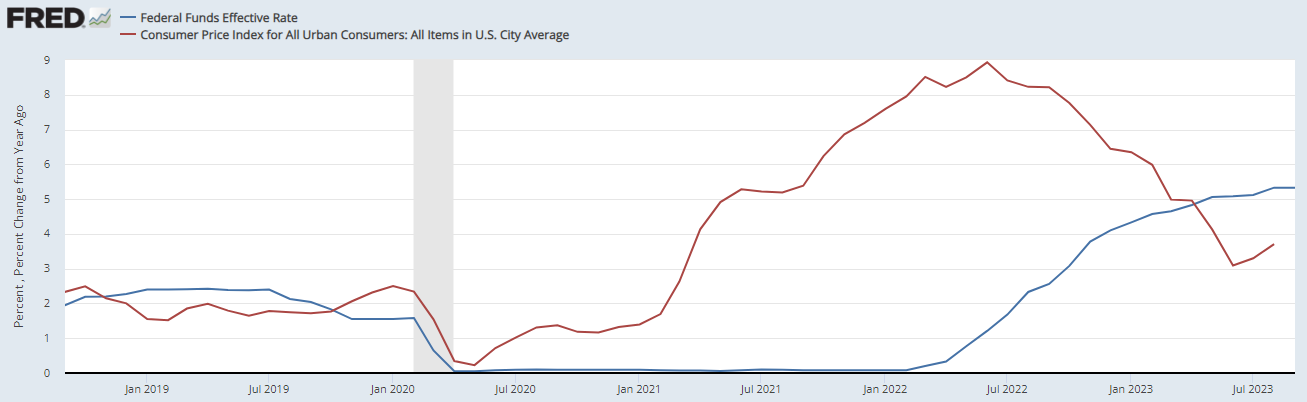

So what does any of this have to do with the current cycle? The Fed’s concerns over the risks of a 1970s-style inflation problem, following their getting blindsided by the huge upturn in inflation post-2020, has them acting more like the Fed of 1920….likely by accident. Real interest rates have moved sharply higher and quantitative easing remains on autopilot.

Obviously, Congress is not anywhere near the actions of its long-ago predecessor, though the recent upheaval pertaining to the Speaker of the House has at least partly been due to controversy over federal spending. The monetary system is also very different, but the entire point of this trip with Marty has been to revisit what a central bank tightening into a recession looked like.

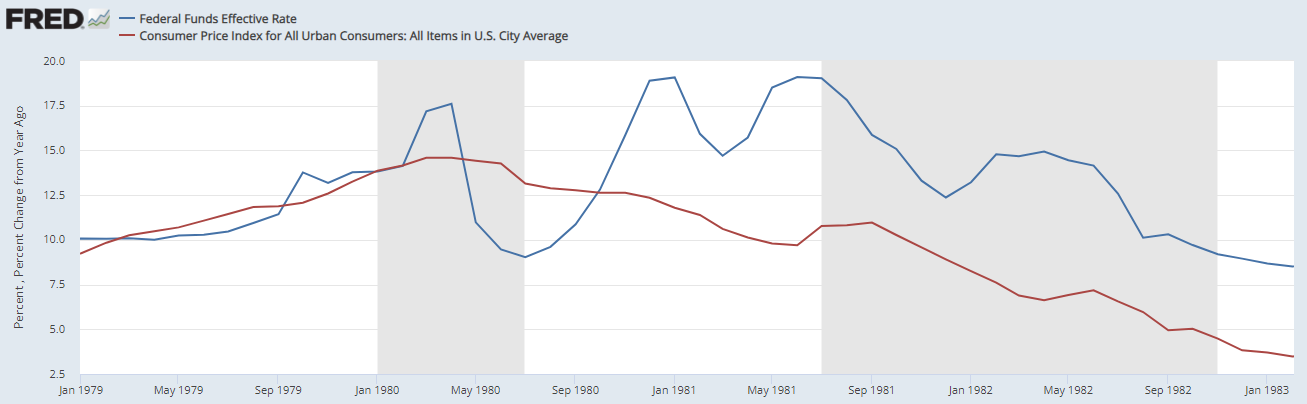

Even Paul Volcker’s Fed reversed its policy direction quickly in the spring of 1980 and took the Effective Fed Funds Rate down from 17% to 9% in just a few months. The Fed Funds Rate peaked at about 4% above the All Urban CPI and the rapid slashing took it to about 4% below by July 1980:

I laid out in summer 2022 the potential for that 1980s double-dip to unfold Bizarro Recession-style this cycle, with the Fed’s fear of repeating Volcker’s sequencing resulting in a REAL throwback style of central banking. The recent moves by the Fed and real interest rates moving sharply positive across the yield curve fit with an economy suffering from massive post-pandemic cross currents entering recession amidst a restrictive central bank.

The underpinning of the Bizarro thesis is that this tightening is the result of incompetent central planning rather than some newfound return to how the Fed addressed things a century ago and that neither the Fed nor Congress are likely to persist with what would now be considered heretically restrictive monetary and fiscal policies.

But in order for Regime Change to unfold amidst the Bizarro Recession, the severity of what they will likely view to end up as policy mistakes, similar to the bungling of the inflation upturn, will require severe economic and financial market conditions to transpire.

Lest we forget that the Fed remained at zero percent Fed Funds and STILL conducting QE in March 2022, AFTER the invasion of Ukraine and CPI at 8.5%!

As the credit cycle gets nasty and unemployment rises considerably, the Fed is likely to be slow to start cutting, and then struggle to keep up to prevent real rates from going higher despite their eventual policy shift.

Similarly, the idea of the current Congress cutting nominal spending at all is likely farcical, but relative fiscal restraint (i.e. going from insane to marginally less insane) heading into what may be a toxically partisan election year, would be directionally in line with their predecessors of a century ago.

While a policy response that would have Ayn Rand’s ghost doing cartwheels while Ludwig Von Mises’ break dances joyously is not gonna happen, the current backdrop is downright Austrian from a direction of travel perspective, despite those responsible doing so unwittingly.

Fear not those of you suffering from LSS - they are unlikely to persist long enough for the system to actually repair all of the misallocated resources from the post-GFC era. Rejoice that your favorite flat-earthing astrological alchemist central planners will once again return to pressing the accelerator….you just may have to remain patient for their incompetence to manifest more fully.

Really appreciate both your writing and your thoughts! Thank you kindly.

Great post! The Forgotten Depression was such a great book. Recommend it to everyone.