Is the Tide Going Out?

Is the Tide Going Out?

Can you get the power of Buffett in the Palm of your hand?

“Only when the tide goes out do you discover who's been swimming naked.”

-Warren Buffett

Have dedicated the first couple of months to introducing my analytical process, and then looking at macro-level events and associated risks. I am going to revisit some of the cyclical risks today, but then add a bit more on ideas as to what to do about navigating this climate.

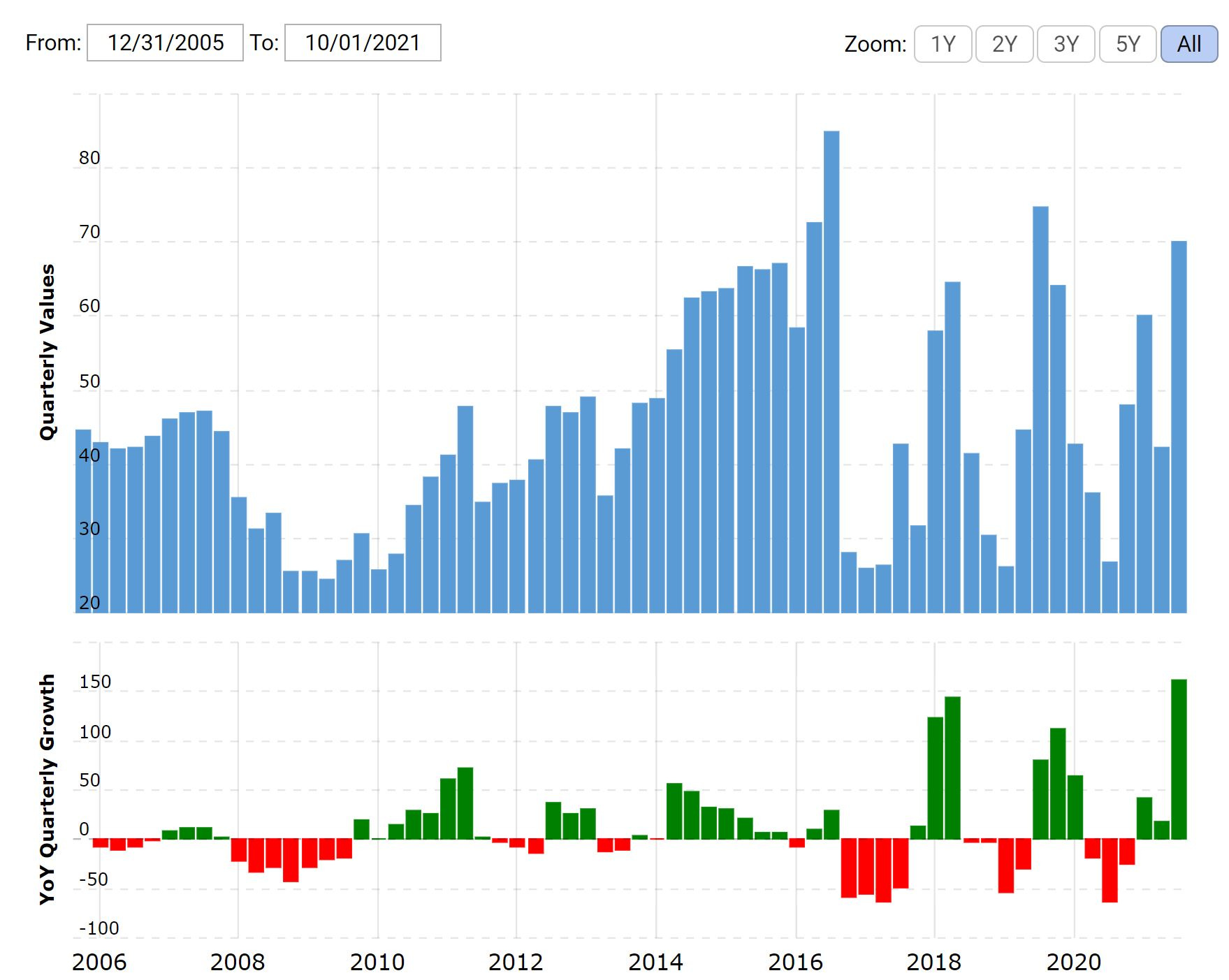

While many remain fixated on the US Federal Reserve, potential quantitative tightening, and 30-year highs in US government inflation data, I continue to monitor what is unfolding outside the US. Here is an updated view of Chinese construction:

The recent downturn has now reached contraction in real terms, which has not occurred in the past 30 years outside of the lockdown period. The downturn also coincided with the beginning of the slowdown in the global industrial cycle last spring, which I have been referencing since the start of this substack in November.

This slowdown is interesting, as it has commenced within the context of the unusual supply and demand dynamics relative to the explosion in goods-based consumption in the West, as well as structural underinvestment in ‘dirty’ industries since the prior cycle peak in 2011-2012. Many industrial commodities, such as oil, base metals, etc., have seen inventory levels depleted and activity focused upon growing production and reserves deprioritized.

Many of the large industry players have instead been focused on ‘shareholder value,’ or financial engineering, as I like to call it. Share buybacks have become preferred over drilling rigs. This is likely to be a multi-year story, as many of the imbalances are now likely structural and will take sustained higher prices to attract further capital investment. In addition, the ESG movement has further constrained the availability and cost of capital, and that movement appears likely to remain for the foreseeable future.

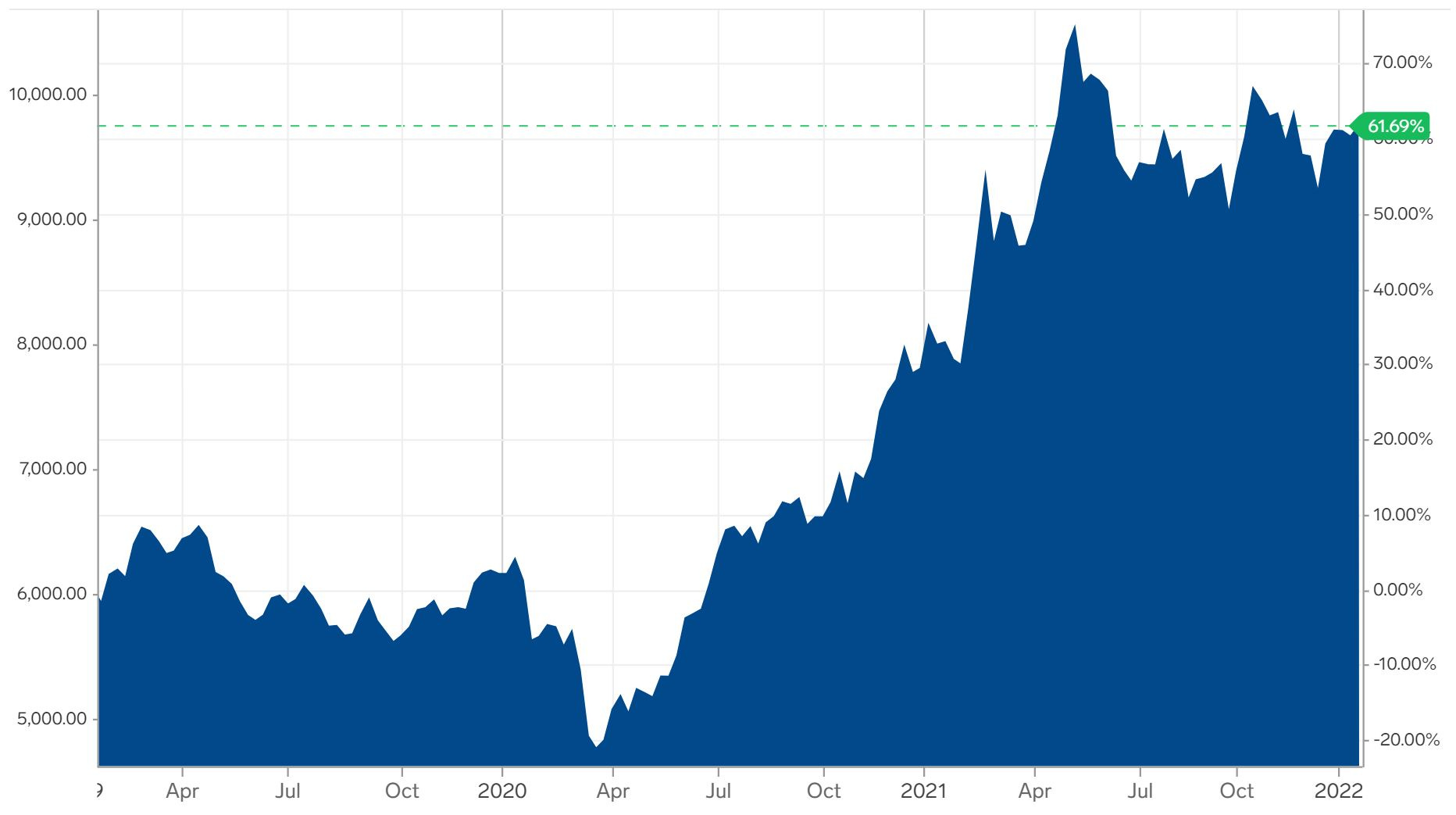

Despite these structural issues, we’ve begun to see various commodities peak and then possibly set up failed rallies. Here is ‘Dr. Copper’ (all charts are 3-year trailing):

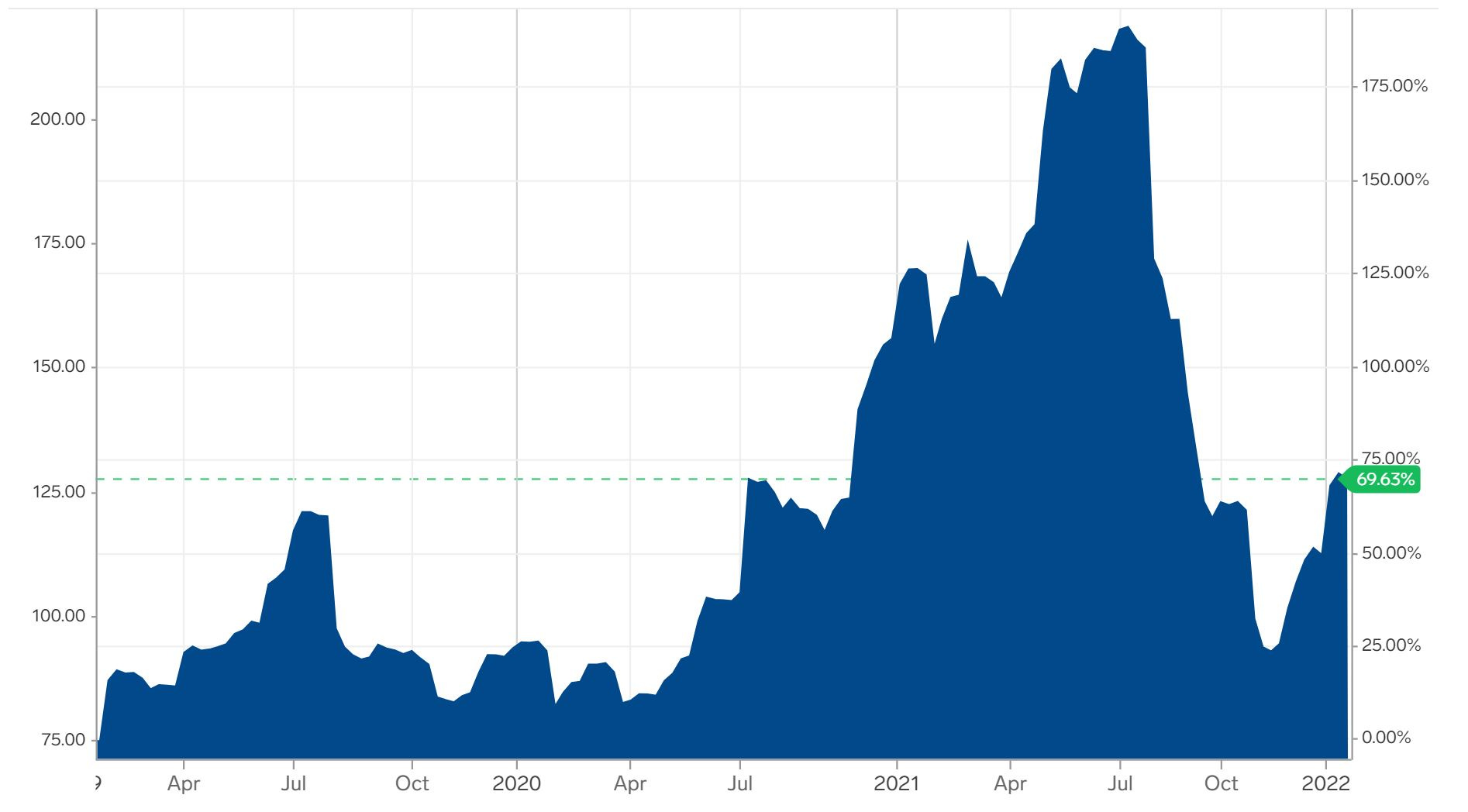

Next, we have iron ore and lumber - remember that Chinese construction chart?

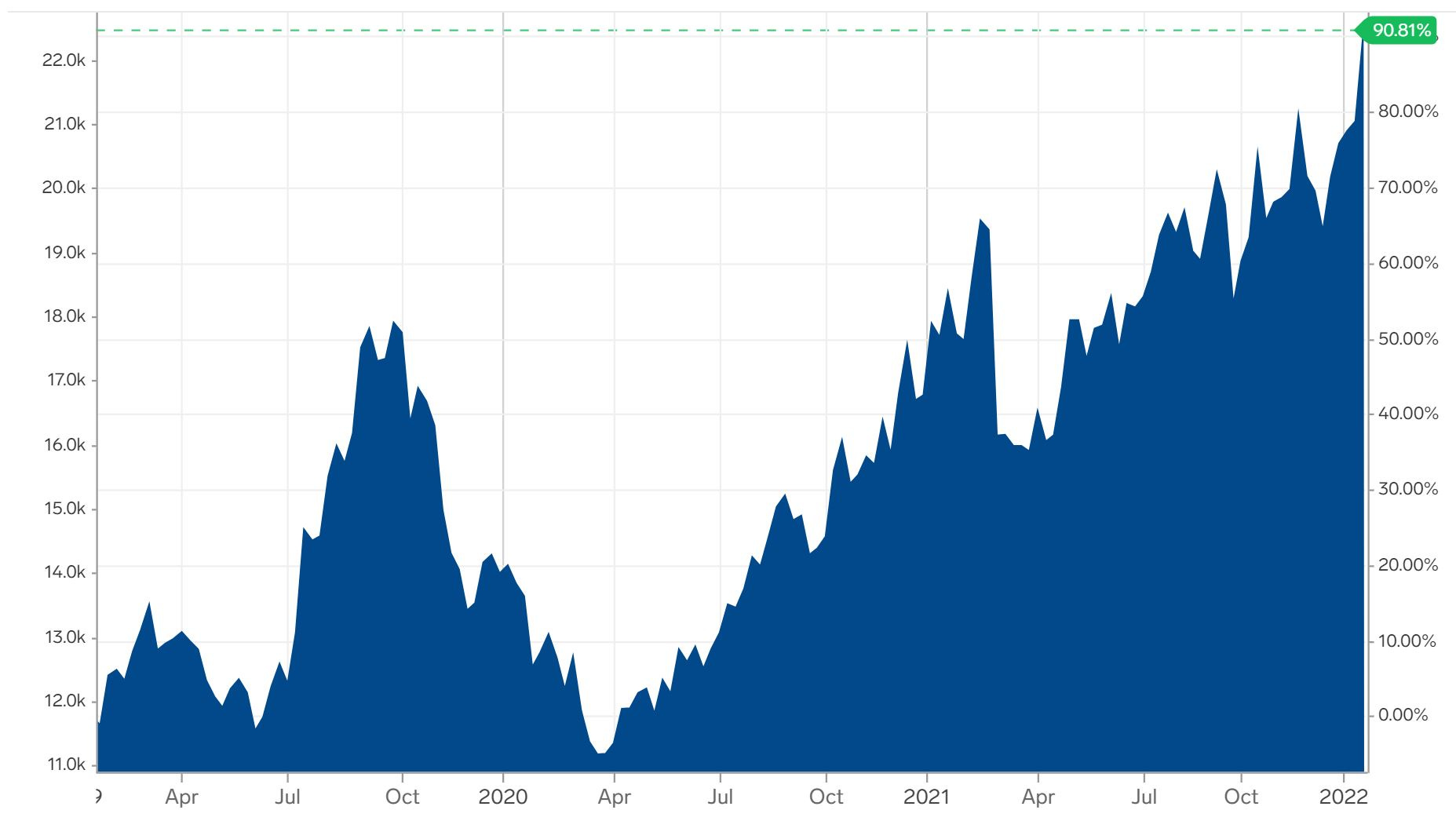

Some of the less liquid and smaller base metals remain at or near cycle highs- here are tin and nickel, for example:

As I wrote recently, the 2007-2009 cycle included a slowdown that turned into a recession, yet crude oil plowed ahead to an all-time high seven months into the recession! Paying attention to a wider breadth in commodities can help flag cycle dynamics, as more and more rollover as cycles mature. It makes sense in this cycle, given the downturn in China appears to be leading, that the commodities more sensitive to that development would weaken first.

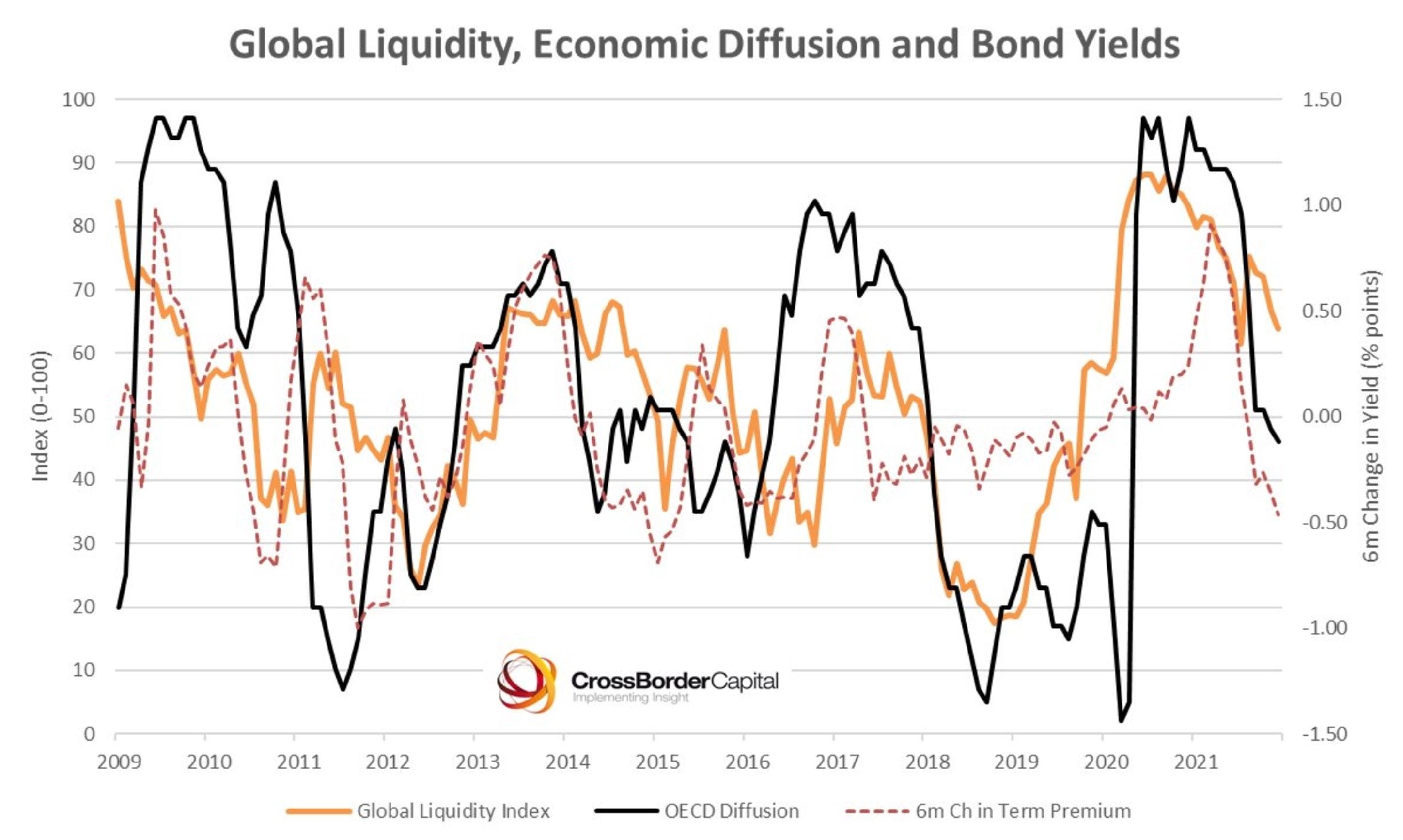

So what happens next? Here is a graph showing various metrics designed to monitor global liquidity conditions:

We can see in this graph the timing of the metrics rolling over preceding the downturn in the industrial cycle last spring, and they remain in rapid decline. This is occurring with ECRI’s leading indicators not yet suggesting that the slowdown is due to be over at least for the next 1 to 2 quarters, and with central banks around the world either well into tightening cycles, such as emerging markets like Brazil or at the onset of tightening cycles, like in the US. Interestingly, China cut rates on the margins earlier this week.

In addition, global bond markets have experienced bearish flatteners in recent weeks. That is when bond prices decline, with interest rates going up across maturities, but with shorter-term rates going up faster than long-term rates. The term structure of the yield curve shifts higher but gets flatter while doing so. That is often accompanied by economic slowdowns and can precede inversions, which is when longer-term rates decline below short-term rates.

How have US investors been responding to these developments? Like Pavlov’s dogs, they’ve been well conditioned to…..buy the f*cking dip!

The recent implosion in the most speculative segments of the market, with many names down 50%+, echoes of the year 2000, IMO. Similar to that period, retail investors are all ginned up and still pouring money in, as the Fed will surely bail us all out should things get worse….right?

So what is an asset allocator/investor to do in this backdrop? Be careful! That is my first idea, which is that this is a setup where protecting capital is paramount. In a period in which liquidity is contracting, those who build liquidity can own very valuable optionality - i.e. be in a position to acquire attractive assets as others deleverage. Guess who has been building a massive cash war chest over the past year? Warren Buffett!

Contrary to his country bumpkin ‘buy and hold’ brand, Buffett has been a ruthless deployer of cash optionality as Berkshire has grown to a size where more nimble market timing is pretty much impossible. Buffett was an active timer in his hedge fund days back in the 1960’s- for example, he closed his fund and went to cash/bonds in 1969 and waited until the 1973-1974 bloodbath to redeploy in size.

Certainly, holding high cash positions in the midst of high inflation may seem counter-intuitive, which brings me to my specific idea. If you are not an expert asset allocator or stock picker, then it may make sense to allocate capital to someone who has shown that skill set.

Unfortunately, industry dynamics make finding potential candidates outside of those available to qualified investors (think hedge funds). Most asset management businesses have been wrecked by the wholesale move into passive indexing, whether through mutual funds or ETF’s. Many have been in survival mode and compounded the long-term legacy incentives to hug benchmarks. Active managers who hold 5% cash can be seen as taking huge career risks, let alone holding 50%+!

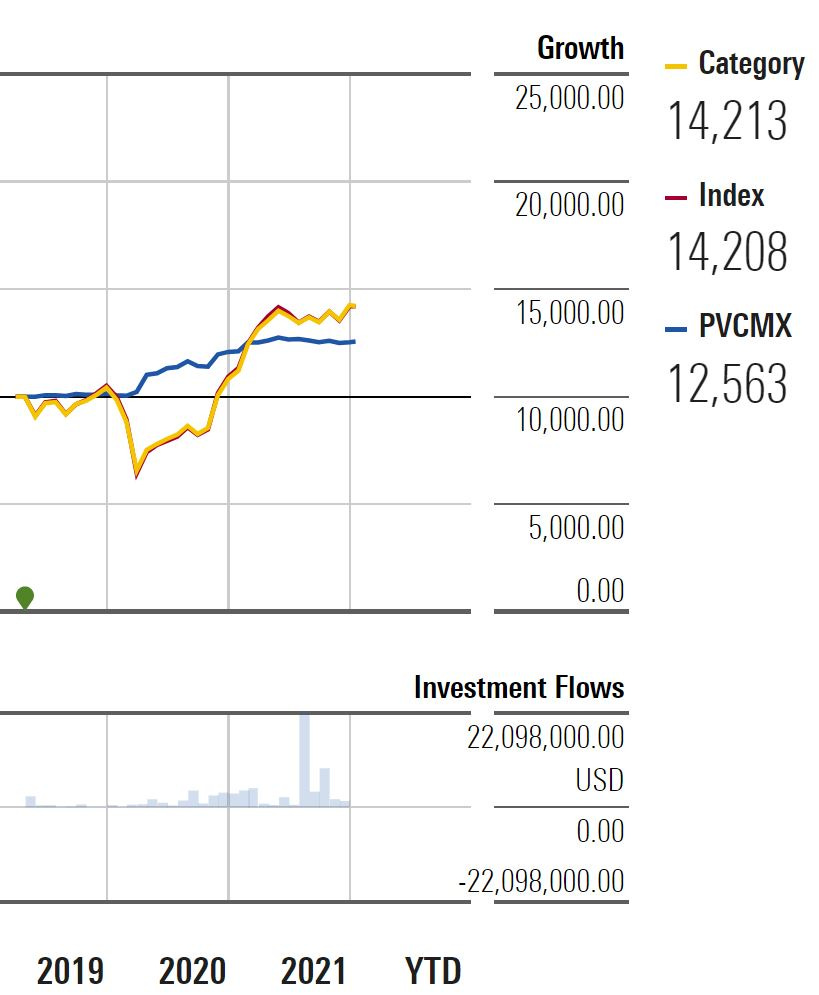

This brings me to Eric Cinnamond and Palm Valley Capital Management. Firstly, I have no connection to the firm and never met or spoken with anyone affiliated with the firm. I have been a long-term admirer of Mr. Cinnamond, as we are about the same age and have tracked his career since he was at a fund company called Intrepid Capital Management. He’s offered the same strategy across various firms since the mid-1990’s, and started the Palm Valley Capital Investor (PVCMX) fund almost 3 years ago. The fund has just $81 million in it per Morningstar as of yesterday, and the track record looks ‘not great’ compared to the assigned benchmarks since its founding. However, as they say, past performance is not a guarantee of future results.

As of September 30th, 2021, which was the last public filing information, the fund had over 80% in cash. If you look at the NAV chart of the fund since inception, we can see how the fund did not decline with it’s peer group or assigned benchmark in the 2020 market drop:

Note the obvious ‘benchmark hugging’ of the peer group! No wonder people are less and less willing to pay for ‘active’ management. The fund did quite well as Mr. Cinnamond used the optionality of his cash into the 2020 market dislocation and then subsequently underperformed as we returned to crazytown. Who in their right mind would consider a fund which has trailed its benchmark by almost 20% over the past year?

His fund did very well in 2002 and 2008, as his focus on absolute risk levels was rewarded. While no one is ever likely to be the ‘next’ Warren Buffett, if I was going to look for a specific version of Buffett, then it would be the 1960’s version when he was managing a relatively small pool of capital. Mr. Cinnamond has been disciplined in closing funds in the past once he felt size began to constrain his flexibility. My guess is the window to access his talent may not remain open indefinitely.