Look East...Just Not Too Far

China has been a focus for many regarding potential risks this cycle, and probably for good reason. China has had huge malinvestment fueled by ‘huger’ credit growth, a property bubble that appears to be imploding, very low monetary velocity with total debt to GDP approaching 300%, and all with deteriorating demographics. However, most of these issues are widely known and discussed. My attention has been drawn a little less Far East to Europe.

While recent headlines have understandably been focused upon Ukraine and the huge spike in energy prices, there have also been rumblings that started in broader financial markets. Similar to the US and much of the rest of the world, consumer inflation has erupted to a multi-decade high:

This has transpired with the amount of negative-yielding bonds having peaked at over $18 trillion, with most of that within the Eurozone.

Convexity is an important metric when considering the relationship between bond yields and prices- more convexity means bigger moves in price with changes in rates. Deeply negative yields resulted in BIGLY convexity. Here is the 10 year German Bund price:

The yield has gone from about -0.50% just a few months ago to about +0.20% this week, with that having resulted in about a 7% drop in price for the bonds….or about 35 years of 0.20% simple interest. Markets have begun to reprice, but like the US Fed, the ECB has not even responded with raising rates…yet.

This shows the front end of the Eurozone yield curve via 2 vs 1-year interest rate swaps, and shows that the curve is ALREADY inverting before the ECB has even acted!

But it is not just the curve beginning to invert, as Eurozone credit spreads have begun to move higher, even as stock markets like the German DAX have remained relatively resilient:

After having tightened for years following the sovereign debt crisis in 2012, when Mario Draghi infamously proclaimed that the ECB would do whatever it would take, rates and spreads have also begun to widen for southern sovereigns like Greece:

While the German 10 year has gone up about 70 basis points, Greek’s have gone up by almost 200. Here is an example of Eurozone investment grade corporate yields:

All this has been unfolding within the context of a global economic slowdown, in which leading indicators remain pointing in the wrong direction, and global liquidity is contracting….BEFORE the ECB or Fed have raised rates a single time!

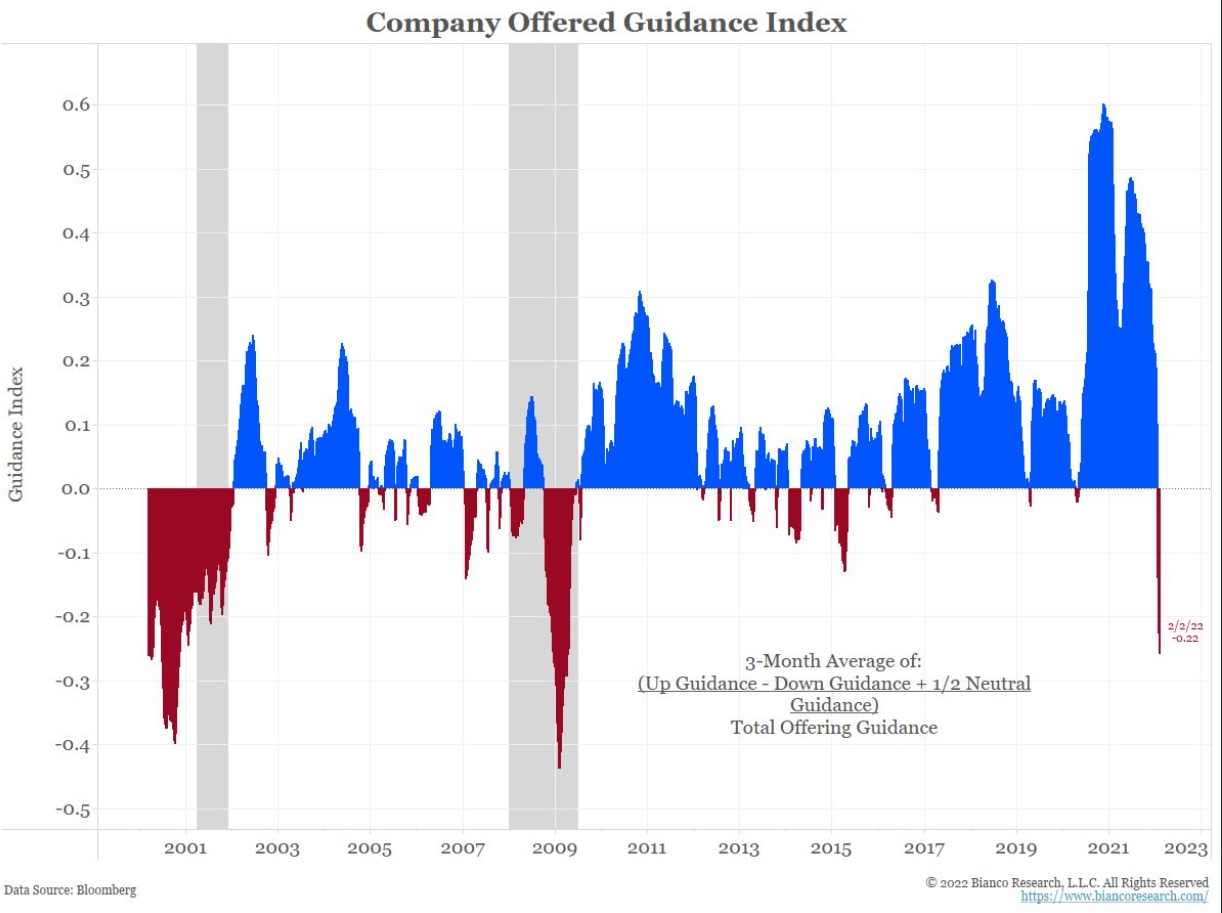

That chart shows how negative corporate earnings guidance has turned in the US- note the amplitude and prior comparable instances.

So a global economic slowdown, with the two biggest central banks still to begin raising rates, while consumer inflation pressures remain at multi-decade highs, yield curves flattening and/or inverting, retail traders buying meme stock call options, and also this:

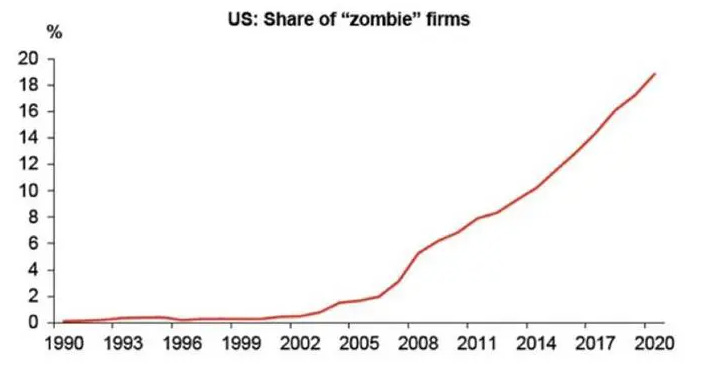

That is a chart of US companies who have interest costs higher than profits, and that is with the cycle of tightening financial conditions in its relative infancy. Yes, mega capitalization US corporate balance sheets are cash-rich overall, but like aggregate net worth data for the nation, they mask a large underbelly of financial strain and potential despair.

With increasing political divides going pancontinental, and protests emerging in such ‘maniac’ nations such as Canada and Finland, is anyone familiar with any European history when societal acrimony is on such an upswing?