Nature vs Nurture

The debate within biology, psychology, and sociology regarding nature versus nurture endures, as the relative impact of genetic and environmental factors on human development is complex.

With the gratuitous use of a baby picture to get readers smiling out of the way, analyzing ‘macro’ offers similar challenges with complexity. However, rather than nature versus nurture, the paradigm is often cyclical versus structural.

For example, the structural trend and forces unleashed in the 1990’s were reasonably well known contemporaneously, as Moore’s law was driving an epic growth in computing power. The information age went into hyperdrive with the ubiquity of the internet facilitated by broadband access. A transcendant era of access to information, analogous to the early 16th century explosion in the use of the printing press, was birthing - how exciting!

The resultingly ‘obvious’ nature of the structural forces, along with a healthy dose of easy money from the Federal Reserve (shocker!), culminated in the tech and telecom mania. Huge amounts of capital were deployed to try and capitalize on the trend, but then something funny happened on the way to paradise - the cycle intervened.

I still read/hear people recount that the 2001 recession was triggered by the horrific events of September 11th, 2001. In reality, the National Bureau of Economic Research declared the recession had begun in March that year, with that judgment rendered via this press release from November 26th, 2001. Ironically, that release came just as the economy was emerging from the recession - you can find historical NBER cycle dates here.

Why get into this level of detail? The chronology of that cycle offers an example of the interplay between cyclical vs structural. The information age was in the midst of accelerating. As we now know, things like cloud storage and computing, ‘big data,’ and mobile computing via smartphones would follow. For those who invested in Amazon, for example, capturing this structural trend has been hugely rewarding. However, even Amazon was not immune to cyclical forces:

We can see from this split-adjusted weekly chart of Amazon from the start of 1998 through March of 2003, that despite the epic nature of the opportunity to come, the stock declined 95% from its December 1999 peak to its October 2002 low! From that low, the stock is up about 450 times in price as of this week.

Huge amounts of malinvestment took place during the mania - remember Global Crossing, Worldcom, Nortel, Lucent, etc? This old page lists tables showing the evolution of market caps during the cycle.

When the cycle turns, market forces have a way of overwhelming ‘pivots.’

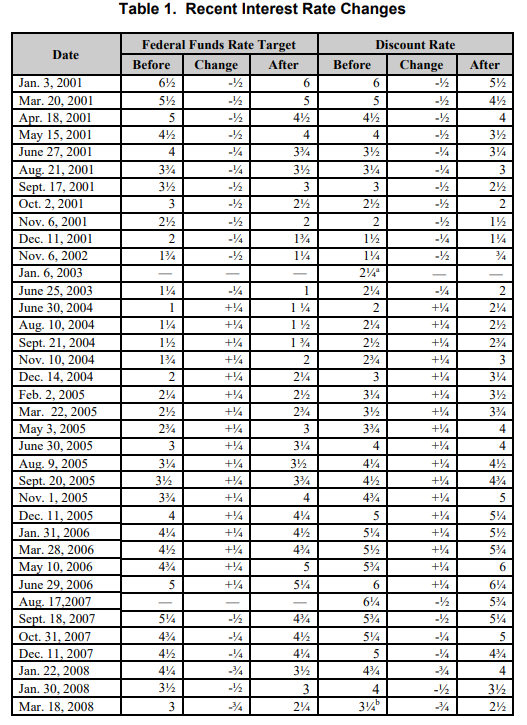

That is a graphic pulled from a Congressional Research Service report dated March 19, 2008, or five days after Bear Stearns was acquired by JP Morgan in a ‘shotgun’ merger facilitated by the Federal Reserve Bank of New York via the Maiden Lane entity. Note the series of interest rate cuts into the cycle turns in 2001 and 2008. The Federal Reserve ‘pivots’ did not result in a sprinkling of fairy dust to overwhelm cycle forces.

Even the announcement of QE I in late November 2008 took place amidst widespread business cycle contraction. It, along with the revocation of market-to-market accounting from FASB, likely did ameliorate risks of a 1931-style banking system collapse, but signs of a global upturn in the business cycle began to emerge in January 2009. Basically, the cycle was already beginning to turn and QE had helped ‘chop off’ the left tail rather than overwhelm the cycle.

‘Zombie’ companies are those which do not make enough money in order to service the interest expense on their debt. The graphic above was shared just over a week ago on Twitter. Will the Fed pivoting at some point in the coming weeks/months amidst a global recession overwhelm the current cycle? How much malinvestment has taken place since the Global Financial Crisis?

Economic contraction shifts the context from that of liquidy to solvency. In periods like late 2018, when the US economy was in the midst of a slowdown, throwing liquidity into the system proved to reinvigorate speculation, as significant issues related to solvency had not yet emerged.

Protecting the solvency of federally chartered banks is one thing, as was done on a large scale in 2008-2009, but will the Fed be willing and able to ameliorate potential insolvencies of 700+ non-bank corporations? How about all of the small and medium-sized businesses which limped through the pandemic only to be confronted with the first global recession in forty years? Emerging market nations? European banks, corporations, small and medium-sized businesses? How about property developers in China?

Even if one has a hugely bullish and/or optimistic outlook for a structural theme in the coming years, I believe it wise to consider what typically takes place during contractionary business cycle downturns. An awareness of how important cyclical forces are is paramount. The Worked Shoot was started to focus on analyzing and navigating these cycles….along with the gratuitous use of baby pictures.

Have to think that Jumia has similar characteristics to Amazon. Not easy to make the case but if future growth does not occur in Africa than where?