Parsimonious Put

The now infamous “Fed put” was born in 1987, when a freshly installed Federal Reserve Chairman, Alan Greenspan, assumed office that August, only to be greeted with the October crash. Here was the front page of the New York Times from the day of the crash:

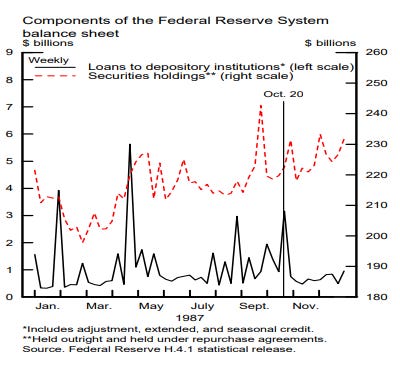

Anxiety over the crash having a similar signaling effect as 1929 was widespread. Greenspan responded with a statement of support on Tuesday, cut rates from 7.5% to 7.0%, and provided emergency liquidity. Here was the Fed’s balance sheet for the year:

Obviously, we know that a second Great Depression was not indicated by the crash. In fact, the crash did not even precede a recession, but rather a mid-cycle slowdown that subsequently reaccelerated - i.e. a “soft landing.”

The events that transpired in the autumn of 1998 were similar, in that the collapse of Long Term Capital Management emerged amidst a mid-cycle slowdown, and Greenspan and the Fed were there to add stimulus and also not-so-gently “encourage” the bailout of the hedge fund by the major Wall Street investment banks. Technically, no public money was involved in financing the unwind. The subsequent re-acceleration of the business cycle, along with Y2K-related stimulus, culminated in the dot com/tech/telecom mania in 1999-2000.

The Fed once again responded to the horrific events on September 11, 2001, though that occurred several months into the recession that began in the spring of that year. They responded once again in August 2007 and many subsequent times during the Global Financial Crisis, then again in the summer 2011, autumn 2012, December 2018, and March 2020. No doubt, they will respond once again at some point in the future.

However, the extended business cycle expansion post-GFC has fostered some dangerous expectations on the efficacy of the “Fed put.” The panic in March 2020 was technically part of a recession, but the traditional knock-on effects from the recession were overwhelmed by the 6%+ of GDP in excess fiscal stimulus the US federal government dished out. The result has been a 13+ year period in which the correlation of the Fed acting has become a belief in causation - i.e. as long as the Fed “pivots,” a business cycle contraction will not occur.

With the benefit of hindsight and the context of subsequent Fed actions, those utilized by Greenspan in 1987 were parsimonious - a piker put. But what is the “put,” really? The intent certainly exists for the Fed to act, and potentially in major ways, in order to attempt to buttress the financial system and economy. However, is it pre-ordained to be effective?

The chart shows federal debt held on Federal Reserve Banks’ balance sheets or a proxy for quantitative easing (QE).

What history suggests is that the relative effectiveness of the put correlates with whether or not its timing occurred during a growth rate cycle slowdown, or whether the reflexive forces of business cycle contraction are triggered. This is why a robust business cycle analytical framework is of paramount importance at present, in my opinion, and why I am spending so much time recently in The Worked Shoot on the topic.

The theoretical window for a Fed put to be effective would have been when a growth rate cycle slowdown was still plausible. Instead, because of the recent cost of living crisis, the Fed has been tightening through that window!

Broad measures of coincident economic activity for the US have already reached the zero bound, with leading indicators still pointing towards recession. Soft landings have occurred when leading indicators turn back higher without coincident data turning negative.

Despite the backdrop of near-zero growth, the Fed just raised rates once again and hinted at possibly two more 25 bps hikes between now and May. But even if the Fed pauses, that will transpire with recessionary forces likely already being unleashed, and leaving the Fed’s eventual response having to be the opposite of parsimonious in efforts to combat recessionary dynamics.

With a divided US congress less likely to be profligate outside of a dramatic crisis, we may get a case study to test whether the Fed put is real or fake. As a 6% of GDP orgy may not be in the offing, from a business cycle perspective, put me down as expecting the latter.