Pavlov's Investors

What is going on in markets relative to positioning and sentiment? Like Pavlov’s dogs, investors have been classically conditioned over the past thirteen years to count on the ‘Fed put,’ and the buy the f’ing dip (BTFD) into each and every market decline. Even during the acute market panic of March 2020, retail investors drooled as the bell rang and dutifuly BTFD.

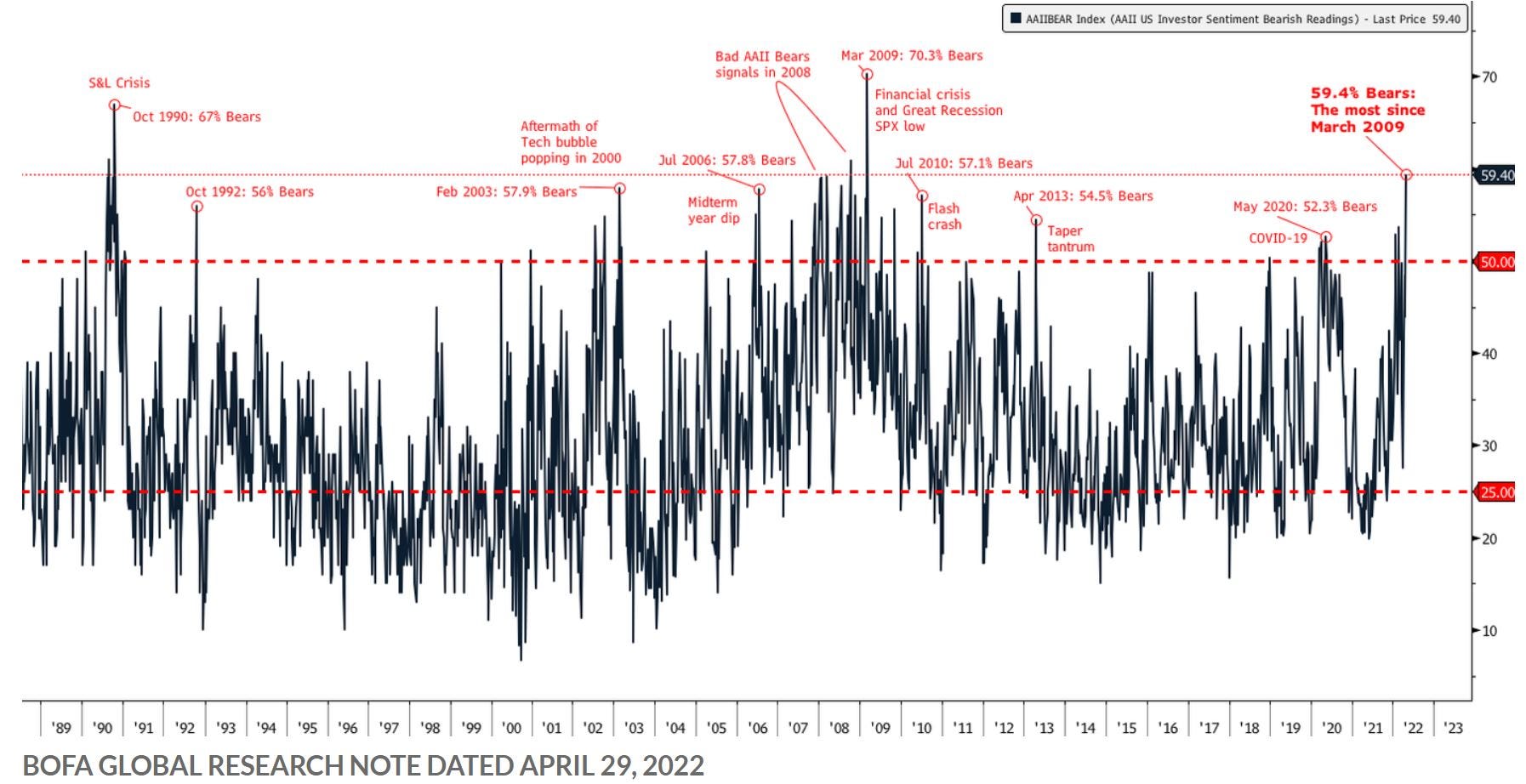

In the era of unrelenting information, it can be difficult to source quality and extract signals from the noise. For example, per this article from earlier in the week, apparently individual investor sentiment by the AAII survey is near the worst of recent history:

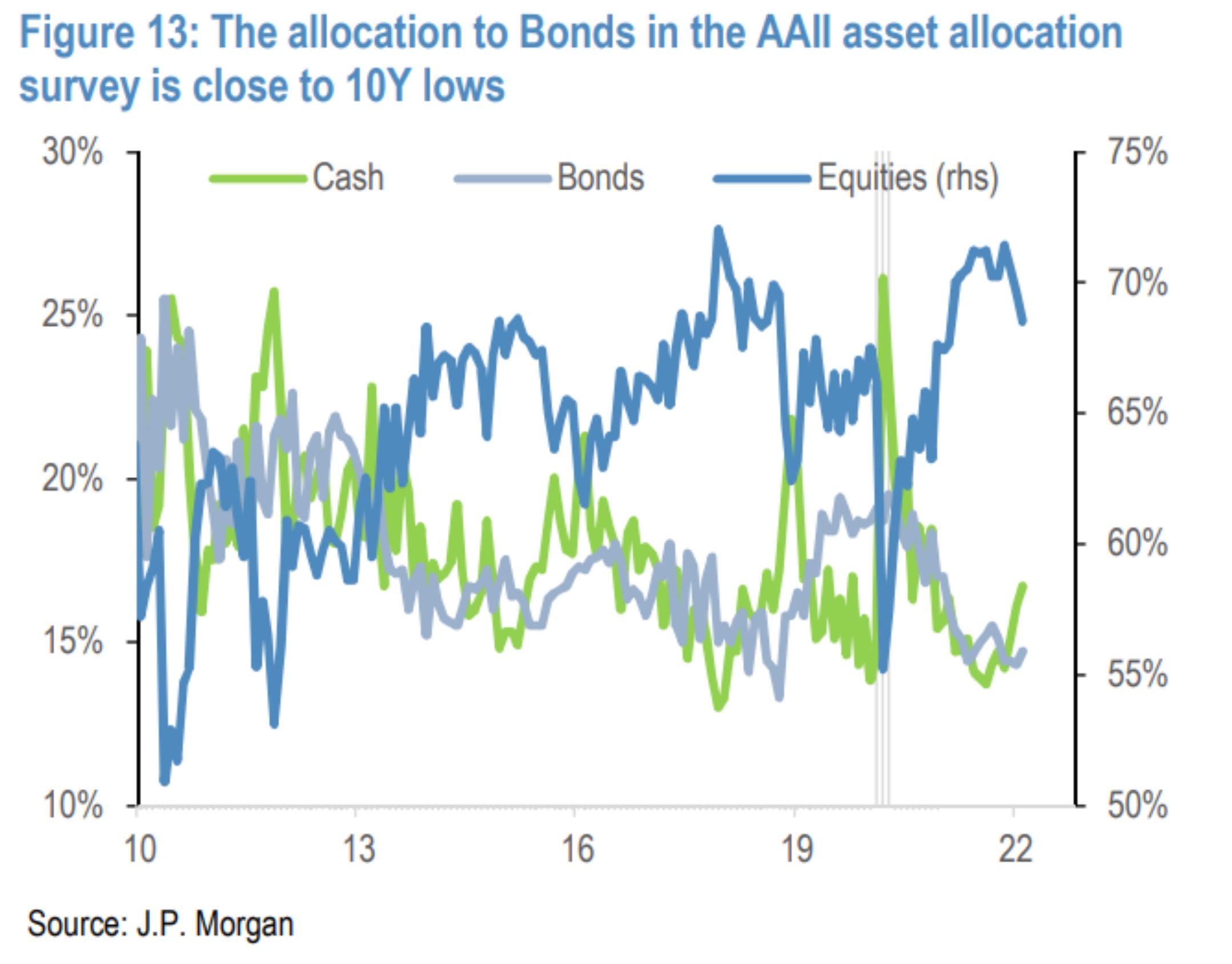

However, as this chart shows, which is through the end of March, positioning in this particular survey has not been tracking sentiment:

Data for April has been released, but I was not able to source an updated chart (lazy!)- equity exposure increased in April back to above that of January, and almost at 70%, while it is exposure to bonds which has been reduced significantly. This is just one of many surveys, and it has a very inconsistent track record as to being helpful in forecasting markets. But at this point believe it is generally representative of the broad dichotomy between sentiment and positioning.

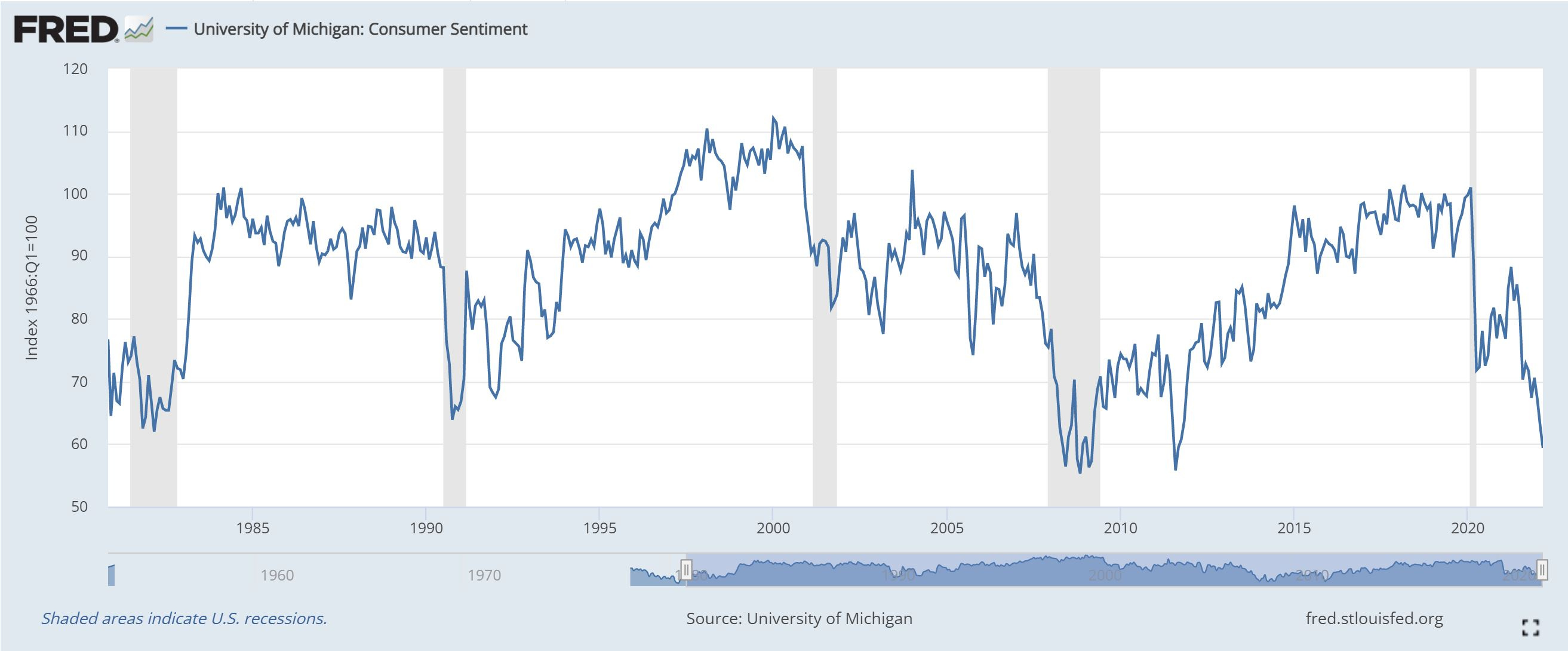

Here is the latest on consumer sentiment- similarly in the toilet:

40+ year highs in inflation, war in Europe, talk of global famine, emerging from two years of pandemic - there are ample reasons for people to be concerned! And yet, with all that concern, the conditioning remains strong.

Despite having declined about 50% since the end of last year, and 70% since its all-time high from February 2021, the ultra-high growth strategy ETF, ARKK, has seen positive net inflows of over $900 million since the start of 2022:

Some have speculated when this ‘cult’ of behaviour may end, and with the conditioning seemingly persistant and pervasive for over a decade, I have no idea!

However, this is all relatively first order thinking, IMO. In addition to the constancy of inflows via 401k and other retirement plan accounts, which Michael Green of Simplify Asset Management has analyzed and chronicled expertly for the last few years, there have been reflexive flows and strategies which have emerged surrounding that ecosystem. You show me a reliable and consistent flow of ‘dumb money’ and I will show you Wall Street actors who figure out a way to make money off of it.

Whether it is the execution algorithms being deployed on behalf of large passive/index investment companies, the creation process of exchange traded funds, or the execution algorithms used to buyback stocks on behalf of corporate treasury departments, these are all seemingly like shooting fish in a barrel for quants. Kind of like arbitraging off-the-run with on-the-run treasury bonds (LTCM!) - easy money!

But as the scope of these flows have increased, so has the awareness of the opportunity to capitalize on them. As competition grows, like when most of Wall Street started piggy backing LTCM’s flows into trades, arb spreads shrink, and prospective returns fall. So what is any self-respecting Wall Streeter likely to do when confronted with the prospect of lower returns, combined with close-to-free borrowing costs courtesy of a clueless Federal Reserve, all while playing with other peoples’ money? Increase leverage!

I do not have any direct knowledge of the following- this is pure speculation and theory on my part. However, it appears that we have faced a wall of volatility selling in options markets in the last couple of years when the increasing fear and anxiety within market participants begins to get reflected in markets. Here is the VVIX over the last five years, which is a measure of the volatility of the VIX - or the volatility of volatility:

Despite all the supposed fear this year, the vol of vol has remained very well behaved and actually shifted its range lower during the latest move lower in markets.

Here is a long-term chart of the ‘VIX’ for the Nasdaq 100 index (NDX), symbol VXN:

Note that volatility remained almost exclusively above current levels for almost three years during the unwind of the great telecom-tech bubble unwind from early 2000 until post-Gulf War II in 2003!

I suspect Pavlov’s Investors may continue to respond to their conditioning for the time being, but I have less confidence as to the staying power of leveraged Wall Street wiseguys who have been shooting the fish in a barrel. They are seemingly a part of the societal sentiment, yet still counting on the ‘game’ continuing under the same rules. We may be close to a time when they have run out of ammo and the fish start shooting back. Perhaps the ramifications of such a deleveraging may be enough to shock Pavlov’s investors out of their trance? I remain agnostic on the question for now. In the mean time, the real shock may be how high price of volatility could go.