Pivot Posers

The ‘Powell Pivot’ and glorious recountings of December 2018 seem to be fairly common on Fintwit- like old friends sitting around a campfire sharing memories of the ‘good ol’ days.’ The Wizard of Oz may be jealous as to the extent to which the legend of the Fed’s powers has grown in recent years, but today we have a look behind the curtain.

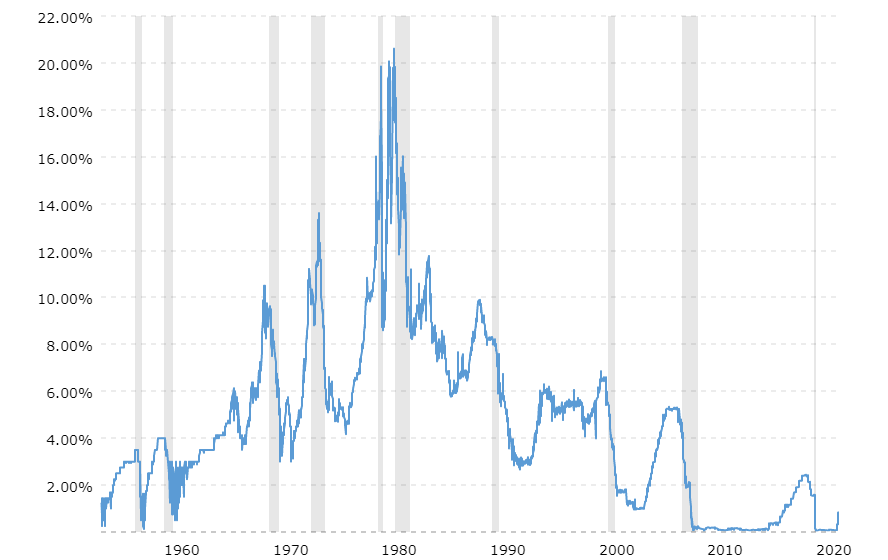

Some appear to be lusting after a pivot in Federal Reserve policy as an ‘all clear’ sign for Pavlov’s Investors to be rewarded for what has become an urban legend: the Federal Reserve orchestrates and controls business cycles. That is the work, or the fake narrative about the powers of the Fed. Here is a chart showing the Federal Funds Rate since 1954 with recessions highlighted:

History shows a pretty strong correlation between tightening cycles and recession, with subsequent pivots to cutting rates pretty normal. Let us break out these 10 recessionary periods for a closer look. Each pair of charts show Fed Funds Rate followed by the S&P 500 Index (SPX) just below.

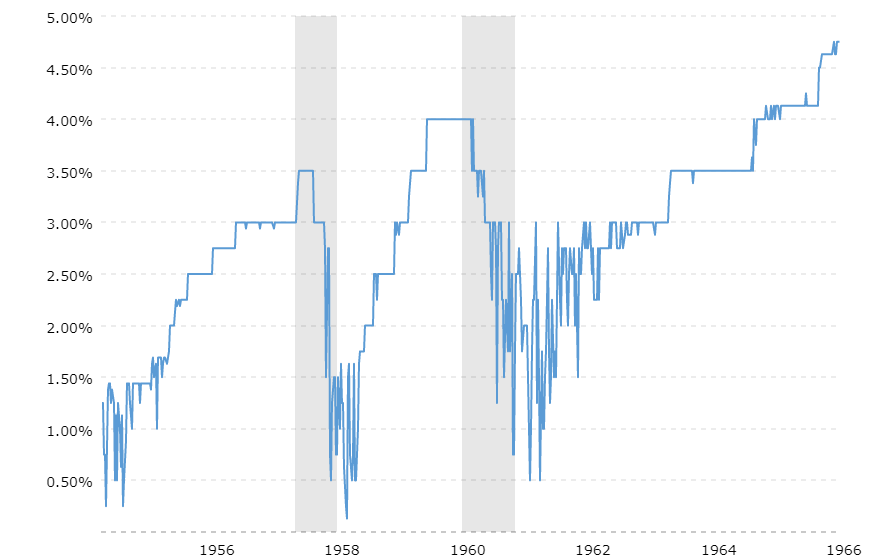

The tightening cycles for both of these recessions coincided with SPX topping prior to the start of each recession and bottoming after the policy pivots and after the midpoint of the recessionary periods. The pivots occurred early in these two recessions.

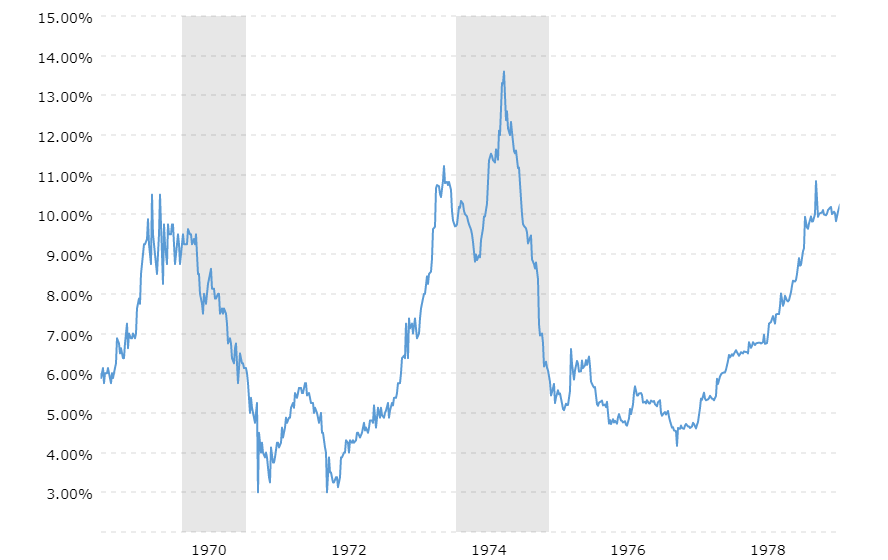

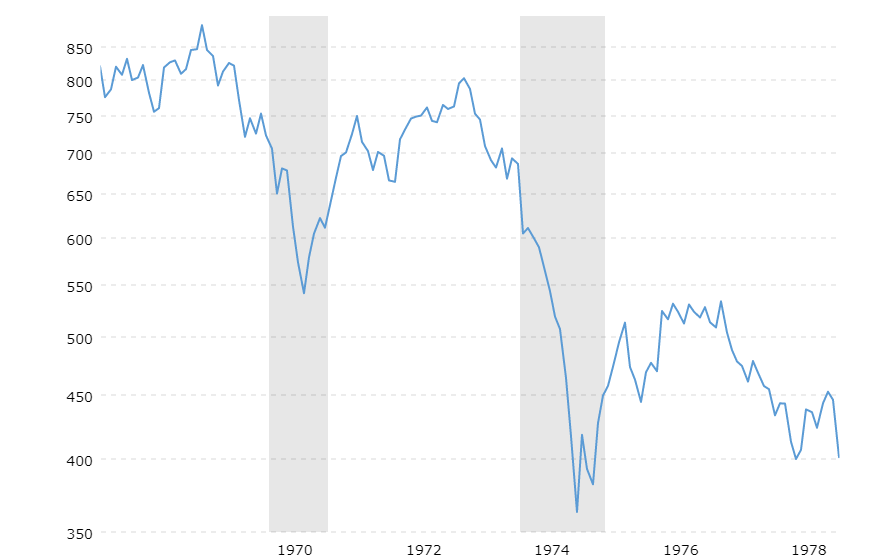

The next two recessions showed similar buildups, with Fed tightening coinciding with SPX topping prior to the recessionary periods. The 1973-1974 period was notable with a ‘triple pivot,’ as the Fed initially began to cut rates early in the recession, then raised rates again, before cutting aggressively through the second half of the recession. SPX was not a fan of any of the three pivots during the period.

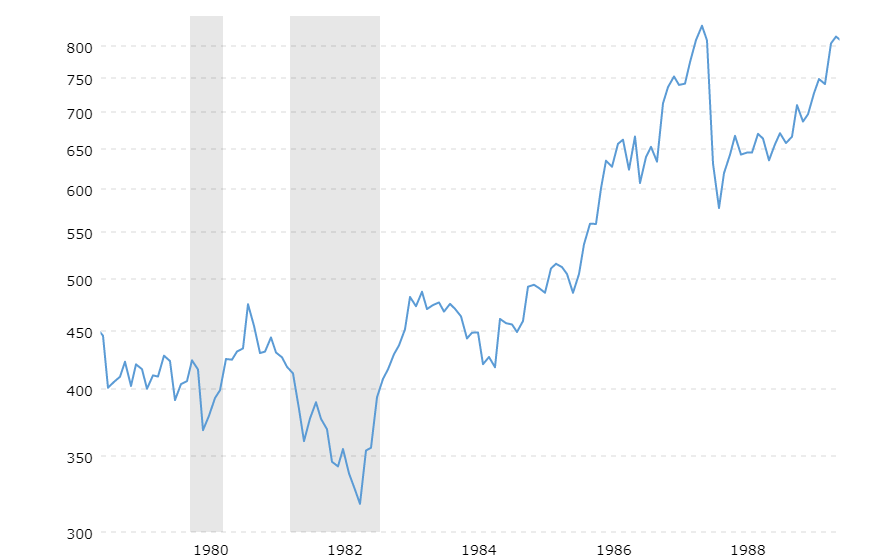

These two recessions covered the much-discussed Volcker era, as short-term rates eventually were raised to over 20%! We once again saw SPX peak as the tightening took play prior to each recession, but the 1980 low did coincide with the pivot from rates dropping from almost 20% to about 9% - score one for the Pivot Posers! The next recession loomed on the horizon, however, and exacted its pound of flesh from the Pivot Posers, as the pivot in rates coincided with an acceleration down in SPX. The August 1982 low was the ‘big one’ and ushered in an 18-year period some refer to as a great moderation.

The great moderation era was only interrupted by one recession, which took place around the time of the first war in Iraq. However, the 1987 stock market crash, which did not coincide with a recession, caused a panic at the Fed and its newly minted Chair, Alan Greenspan. Fed Funds peaked in spring 1989 and that pivot preceded the subsequent recession by more than a year, with rate cuts accelerating through the recessionary period. SPX bottomed around the midpoint of the recession.

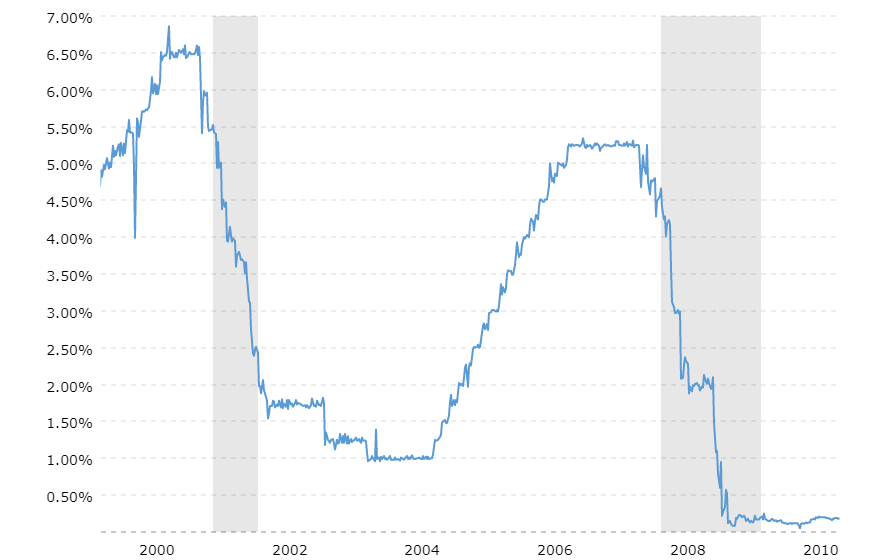

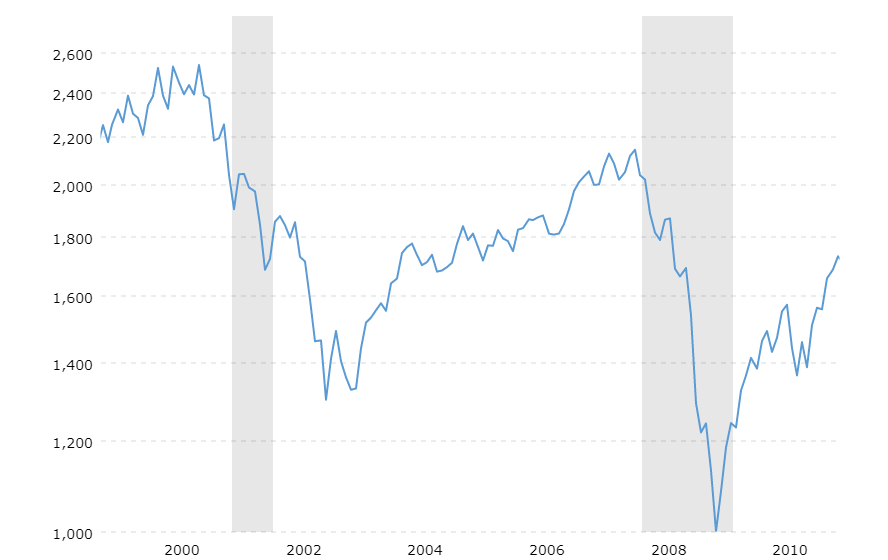

As the moderation period ended with the post-dotcom mania era, the next two recessions once again followed the pattern of SPX peaking as the tightening cycles matured and prior to recession having commenced. The Fed pivot actually occurred prior to the start of both recessions, with SPX not bottoming until well after the recession ended in late 2001 for the first, while towards the end of the recession that accompanied the Great Financial Crisis of 2008-2009.

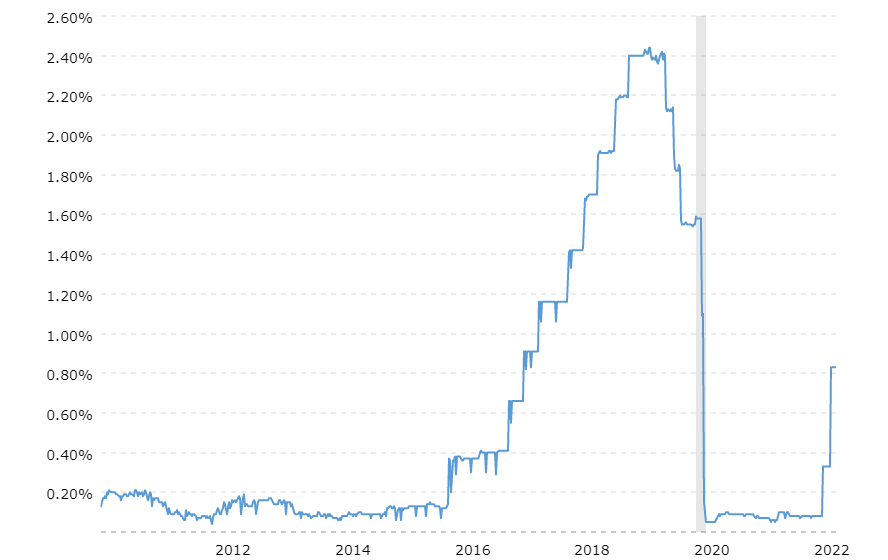

The post-GFC period included an extended period of what became known as ‘financial repression,’ with rates kept close to zero until a tightening cycle commenced in late 2015. SPX experienced two periods of extended consolidation during that period during growth rate slowdowns in the US economy, but neither resulted in recession. The 2020 shock took place over a year after the Powell Pivot, with accelerated cuts commenced early in the recession and SPX bottoming subsequently.

What has been the point of this stroll down memory lane? Recency bias is only natural, and the shared experience of recent history is one of soft landings and a single example of the Powell Pivot occurring within the context of a slowdown which was likely on its way to avoiding recession prior to the onset of the pandemic shock and accompanying lockdowns.

But what about the soft landings which took place in prior periods? Yes, there were periods like the one coming out of the 1969-1970 recession where a tightening cycle took place and resulted in just a stock market correction. Another took place after the 1990 recession and culminated in a soft landing in 1994. However, those periods took place following recessionary periods in which the inherent creative destruction of recession unfolded. Such destruction is typically earmarked by newsworthy insolvencies such as Penn Central in the former, and the S&L crisis in the latter.

The 2020 recession was accompanied by more government deficit spending as a percentage of GDP in less than two years than in the entirety of the New Deal era of the 1930s. The result has been a veritable army of zombie companies and related employment from businesses that stayed afloat with the help of the massive deficit spending. There has been little creative destruction since the GFC.

What are the odds the Fed will successfully engineer a soft landing this cycle? Based on a simple review, they appear relatively low, with the collective ‘feeling’ towards those odds disproportionately skewed due to recency bias. However, given the history, I reject the concept of ‘engineer,’ as the institution’s supposed competency and power should reflect a far better track record if they were not the Wizard of Oz.

Ultimately, the 800-pound gorilla in the room will be whether a recession is likely to unfold. The Fed’s track record has been poor in pre-emptively pivoting and a recession not occurring - a classic correlation vs causation issue.

This has been the case in all sorts of macro environments, whether inflation was high or not. The Fed pivoting is highly unlikely to save the economy or markets if a recessionary feedback loop unfolds. If it does, then the Fed will very likely pivot and it will coincide with things getting worse - not better.

Thanks for your hard work Kayfabe. Good stuff. I've been around long enough and don't suffer from recency bias. The GFC was one thing. The everything bubble is another. Many thanks to you, George and those who are willing (and able) to share first class knowledge.