Sagarmatha Inflation?

Sagarmatha Inflation?

Nepali-based inflation forecasting

Boy oh boy are we all in some deep doo doo (technical macro phrase just in case you have not heard of it before). In an election year with a badly underwater incumbent party, and with inflation as the number one political hot potato. Today’s relatively ‘hot’ CPI report will make for some tasty news headlines and the political calculation for the November election could be locked in already. Institutional power requires a degree of credibility, even if it is primarily made up, and Fed officials’ recent behavior suggests they may be under pressure in this regard. The ‘Jerome Powell Apology Tour 2022’ looks like it may continue for the time being.

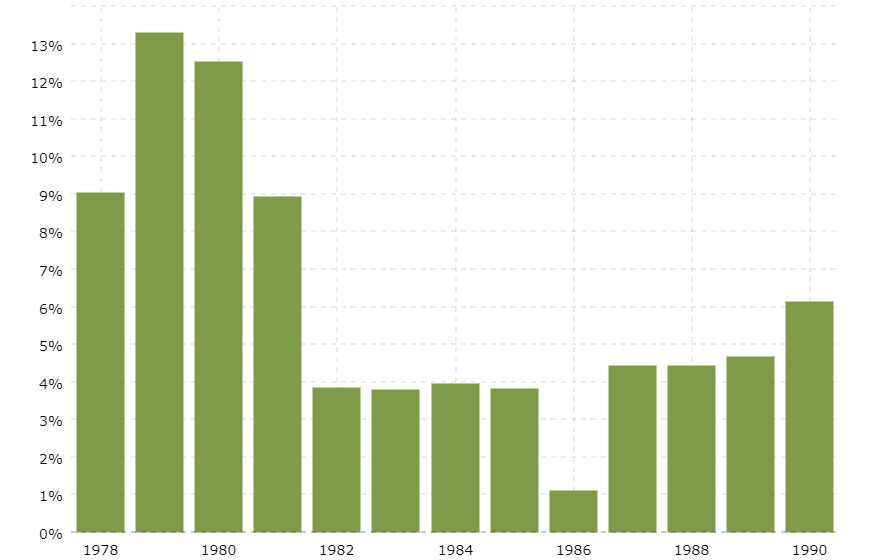

Inflation is often relatively sticky and slow to shift, with consensus expectations and perceptions of those shifts adding another layer of complexity. For example, here was the annual CPI rate during the period many people are currently referencing, or the last time it was reported in this neighborhood:

Note the significant decline from 1982 through 1986, as the annual reported CPI fell to below 4%. Here was the yield on the 30-year US Treasury Bond over the period - see if you can identify what looks ‘weird’:

What in the hell were investors thinking in 1983, 1984, and 1985? I can guess what Dauphin Deposit Bank was thinking, per this 1996 article:

Dauphin Deposit Bank has settled with customers who fought the bank's attempt to eliminate accounts which were "guaranteed" to earn no less than 10 percent.

Under the agreement the bank will terminate the 18-month variable rate accounts; in exchange those customers will receive new certificates of deposit.

In 1983 Dauphin Deposit Bank, which is owned by the same holding company that owns the Bank of Pennsylvania, offered the guarantee when interest rates where in the double digits. They also allowed depositors to add funds continuously to the 18-month variable rate accounts.

With interest rates for those accounts now about 5 percent, the bank sought to close the 4,500 accounts with the guarantee because it was taking a loss.

They basically sold CD’s for retirement accounts that guaranteed a MINIMUM of a 10% rate in perpetuity! By 1984, CPI was under 4% yet 30-year Treasuries yielded almost 14%, for about a 10% real yield. Apparently, the bond vigilantes of the era were morons?

Here is the 30-year yield since just prior to the global financial crisis:

What the hell are investors thinking?!?!? With reported CPI (more on phoney baloney CPI here) at well over 8%, how is it that the long bond is trading around a negative 5% real yield? Are the current vintage of bond vigilantes cut from the same cloth as their moronic forefathers?

I write these things with tongue in cheek, as the situations are naturally different and in a complex way, but the underlying idea is similar. Markets, including the supposedly ‘smarter’ bond market, can be pretty dumb sometimes, particularly at potential secular turning points. Habit, conditioning, and backtested quant models can take time to evolve.

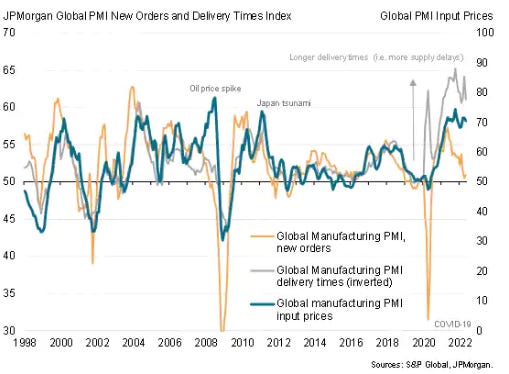

However, recession is an inherently disinflationary force. With the Fed now potentially locked into tightening through the summer, the pathway into recession appears a very high probability. Evidence keeps rolling in that the last two legs of the table may be succumbing to a recessionary feedback loop. Global manufacturing had already rolled over:

Global PMI new orders have now fallen close to contraction level sub-50:

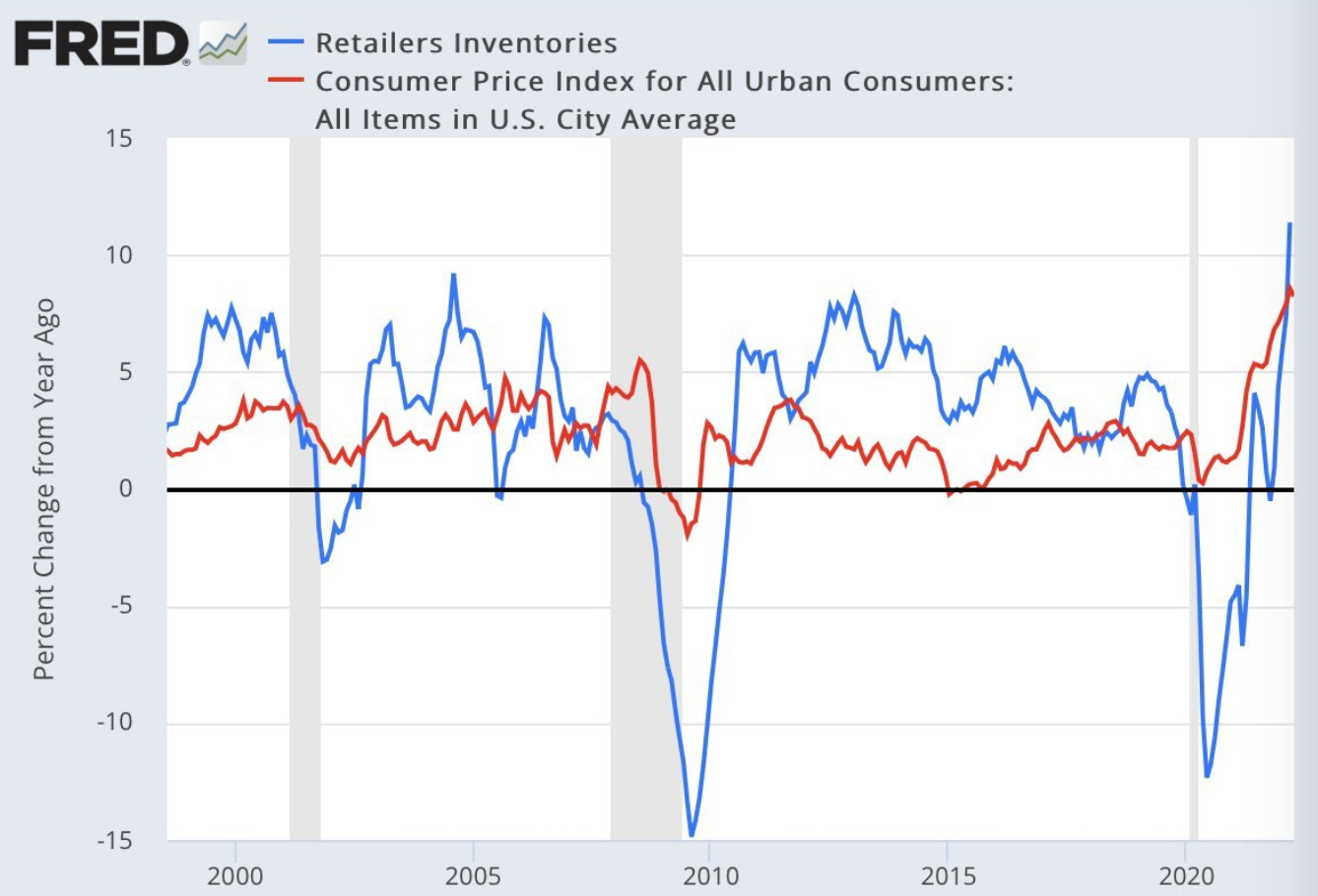

For the US specifically, things like retail inventories jumping sharply:

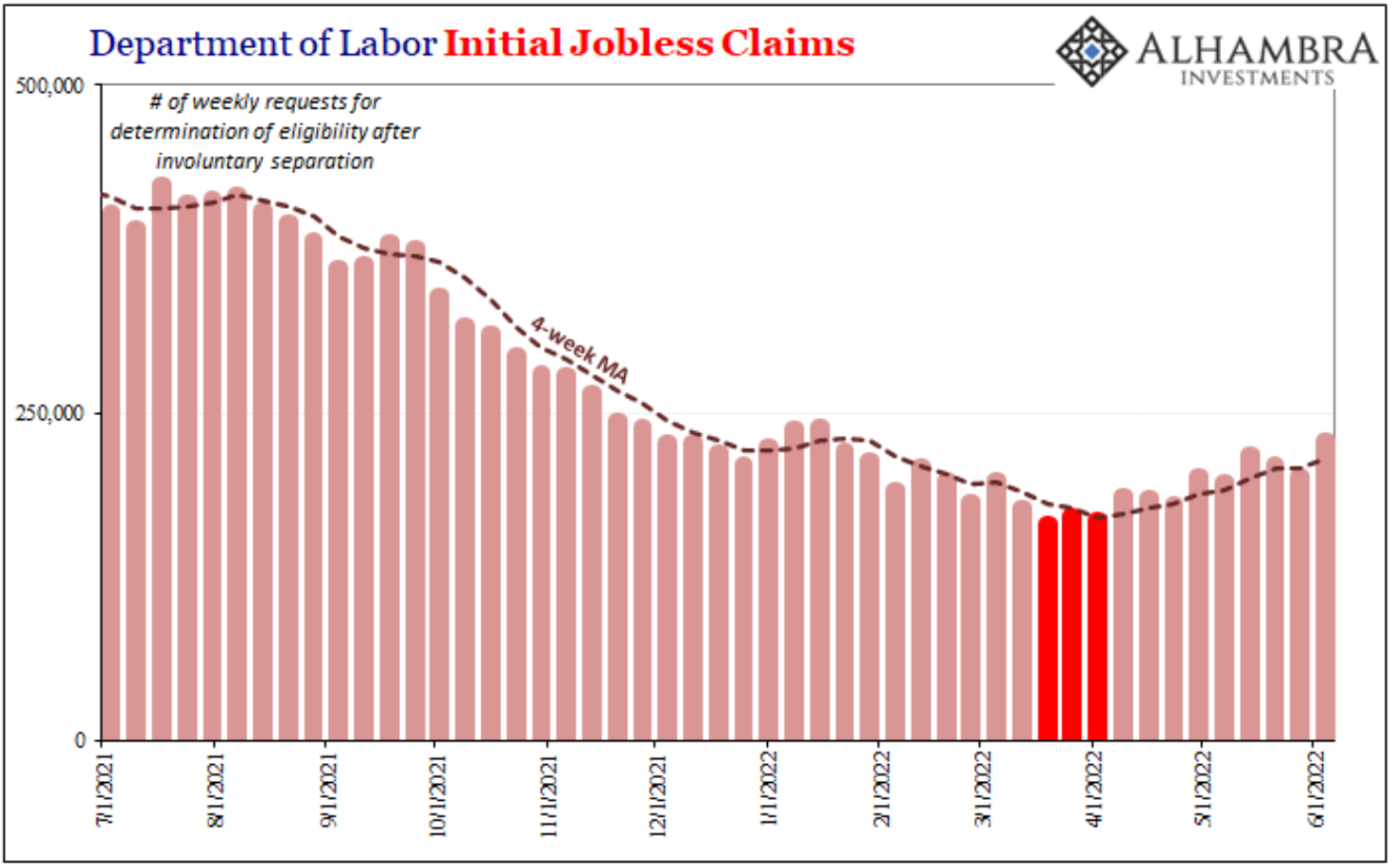

And per Jeff Snider, jobs data in the US has begun to soften on the margin:

Per Liz Ann Sonders, jobs postings data from Burning Glass has rolled over sharply:

As laid out in Regime Change on April 22nd, I remain open-minded as to whether a significant secular timeframe shift may be starting, but as the 1982-1986 period suggests, such transitions can reward remaining intellectually nimble.

A pipeline of demand destruction-driven liquidation of inventory builds could create conditions in which reported inflation numbers soften some in the coming months, as things like hedonics may kick in with greater effect due to potential increases in price dispersion. A full-blown global recession could also create a significant interlude for the favorable long-term backdrop for economically sensitive commodities and related extraction industries.

Even if CPI simply plateaus for a couple of years like it bottomed from 1982-1985, whose to say the 30-year cannot go back to 2.5% on it’s way to 10%, which would be a sort of bizzaro version of the move from 10.5% to 14% on its way to 7.5% in the 80’s?

Regarding interest rates "reversing"... some have been advocating bonds (not exactly sure which part of the duration curve) as the justification is that they will mean revert at some point. Seems plausible but this could be a long way off. Wondering how others see this "investment opportunity".