The Fed is Either Incompetent or Duplicitous

The Fed is Either Incompetent or Duplicitous

.....or Both

I had not watched a Federal Reserve press conference in a while prior to yesterday, and was quickly reminded why - what a kayfabe mess. According to the Federal Reserve Chairman, the following are apparently simultaneously ‘true’:

The Fed badly misjudged the current inflation cycle

The US economy is doing extremely well and will continue to do so, with virtually no recession risk this year

They are intentionally going to tighten financial conditions to fight inflation via interest rate increases and reducing their balance sheet, which he admitted will slow the economy

The Fed continues to target financial market and price stability, even as the former is not within their dual mandate.

With reported inflation at about 8%, they will proceed gradually and seemingly with little urgency to to raise interest rates further from 0.25%, because the economy is so strong it can handle the ‘tightening’

Jean-Claude Junker, the former head of the Euro-Zone, stated the following over a decade ago:

‘When it becomes serious you have to lie.’

There are a lot of serious things unfolding at present, and the scope and degree of lying appears in line with the spirit of Mr. Junker’s comment. Watch what they do, and not what they say.

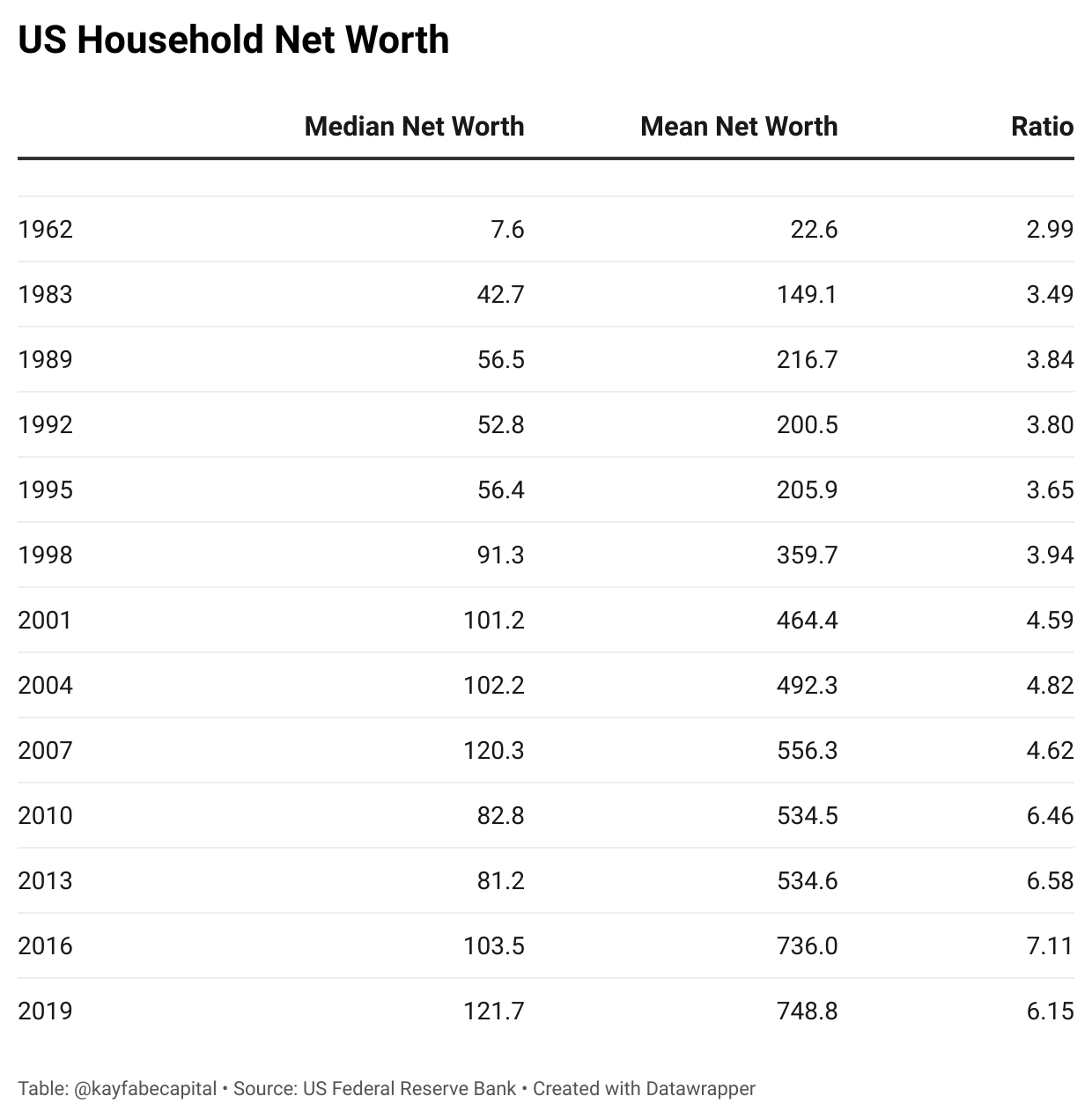

I wrote about the impact of the shift to ‘fake’ inflation data in December, and have often commented about the disingenous nature of the supposed ‘dual mandate’ of the Federal Reserve. The Fed has intermittedly published a report over the years studying US household financial conditions, and here was mean and median net worth in the reports available since 1962:

I’ve added the ration calculation in the righthand column to show how much the mean has shifted relative to the median over time. The last report was 2019, which was prior to asset prices going parabolic since the pandemic began, including stocks and real estate. Note how the ratio began to really take off subsequent to when official inflation data was changed following the Boskin Commission?

Inflation is a regressive force and impacts lower income people disproportionately, and not just within wealthy nations such as in much of the West. People in emerging market nations are being pummeled financially by what has and is transpring. The prioritization of financial assets over seemingly everything else is immoral, in my opinion. Unfortunately, it appears to remain entrenched.

We saw further proof of this over the past week, as huge commodity trading firms, which most people have never heard of, are now lining up for government bailouts. Will anyone be surprised if, like we saw in 2008, central banks and governments prioritize the interests of the monied elite over everyone else? Inflation running at 10-15% and crushing a huge proportion of global population? Let them eat cake.

Now you know why I do not watch the press conferences. It just gets me worked up and angry- apologies for the venting.

With the plethora of lies being spun, what is reality and where may things be headed? For better or worse, here is my base case.

Supply side shocks will remain and get worse, as countries shut off exports as people panic to secure resources. This will likely lead to shortages and continued and more pervasive price spikes, some of which could be even more shocking.

The global economy was already vulnerable to shock heading into this, and will tip into recession, and possibly worse.

The price spikes will be relatively acute, while the economic ramifications will be slower to become evident, with governments and central banks slower to respond with large policy interventions as a result.

Price spikes will create demand destruction and physical shortages drive industrial shutdowns, with a relatively brief period of ‘stagflation’ where official growth data continues to suggest inflation is the bigger problem versus recession. However, that will create a boomerang effect as the recessionary feedback loop launches.

A growth/recession scare will then ensue, with reported inflation still high, as the economy begins to contract significantly. Reported inflation rates will then drop sharply.

Yet another ‘judgment day’ will arrive.

With the economy in recession and financial markets likely in dissaray, governments and central banks will once again be presented with a decision as to whether market forces will be allowed to impose discipline upon the reckless, or whether the status quo continues.

The former may look something like various forms of government subsidies to the broader citizenry similar to those dispersed during the pandemic, to provide support while widespread bankruptcies and restructuring took place. Basically, a social safety net to facilitate badly-needed mopping up of the mess created by chrony capitalism-fueled moral hazard and massive misallocations of capital over multiple decades. My guess is such a scenario is unlikely.

A more likely scenario may be some safety net being offered to the broader citizenry, while widescale bailouts once again emerge. We already have begun to see hints of this recently with gasoline tax ‘holidays’ while the nameless commodity firms lineup for handouts.

A big question may be what the required level of support will be needed to ‘buy off’ and/or distract the citizenry, whether that can be done through the exisiting quantitative easing regime, or a more radical move towards something like Modern Monetary Theory unfolds.

The potential differences between these two paths are fundamental relative to the impact on financial and hard assets. In addition, countries may follow different paths as domestic political situations and cultures vary. These issues are probably 4 or 5 ‘moves’ down the line for investors in the chess game of markets, but will be topics upon which I revisit regularly in the coming months. Prepare to plan.