The Transitory Pivot

The Transitory Pivot

Or is it a pivot to transitory?

The Worked Shoot is back after a week’s hiatus due to being father/husband of the year and forgetting that my family all had off from work and school last Friday. What a wild and fun two weeks it has been in markets!

From a cyclical timeframe, events have been unfolding in line with the expectations I have been laying out so far this year. A synchronized global recession appears to be unfolding, with the US towards the tail end of the countries rolling over into business cycle contraction. Markets have responded in a very typical way, with the US Treasury yield curve now severely inverted, credit spreads beginning to widen out (if not yet dramatically), and the stock market has been under severe strain, as volatility ripples through foreign exchange and fixed income markets.

I think it may be helpful to revisit two terms to which I have developed a gag reflex when hearing or reading: “pivot” and “transitory.” Let us take them on one at a time:

Central banks always eventually reverse policy paths, or else rates would go to negative or positive infinity! Of course the Fed will eventually stop raising rates and probably engage in open mouth operations - i.e. try to influence markets through rhetoric. The overwhelming factor which the “pivot junkies” continue to ignore is the business cycle context. A Fed which changes course, as it did in 2019, while the business cycle was already poised to accelerate, is not the same as a Fed that changes course after a contraction has already begun. During the last two recessionary cyclical bear markets, the Fed reversed policy direction throughout the duration of those cycles! The same will undoubtedly occur once again this cycle - at some point. That is not to suggest that a wild market response may occur when they indicate a pause, a pivot, or whatever - I am guessing that will happen. But it is more likely to be part of normal bear market rally dynamics which always occur within recessionary cyclical bear markets.

Inflation and the word “transitory” have become hotly debated. I have touched upon aspects of my views in prior letters but will attempt to simplify and lay out how/why I think the majority of people are getting the structural forces wrong - and being focused on “transitory” is a big part of the problem, in my opinion.

I covered some of this in Regime Change back in April. What I have called the ‘Lacy Hunt Paradigm’ remains intact, but the complex issues since the beginning of the pandemic have created a lot of confusion regarding the nature of cyclical versus structural forces. The misguided expectation of a short-term, or transitory, nature of the pandemic-fueled factors has ramped up the confusion materially, in my opinion.

The dramatic increase in consumer price inflation worldwide has been a cyclical phenomenon, but as of yet, the structural factors have not changed. Many misunderstand or underappreciate the significance of the confluence of cyclical factors and are now extrapolating them as being structural.

For example, global supply chains are a hugely complex system, and the breaking down of that system was/is far more impactful and long-lasting than many appreciate. It may take years for the system to rebuild and repair into whatever its new iteration will be. That process was/will be further complicated by the orgy of US stimulus, which combined with the dramatic shift in consumer behavior and cheap and widely available credit, resulting in an even bigger targeted orgy of spending on goods.

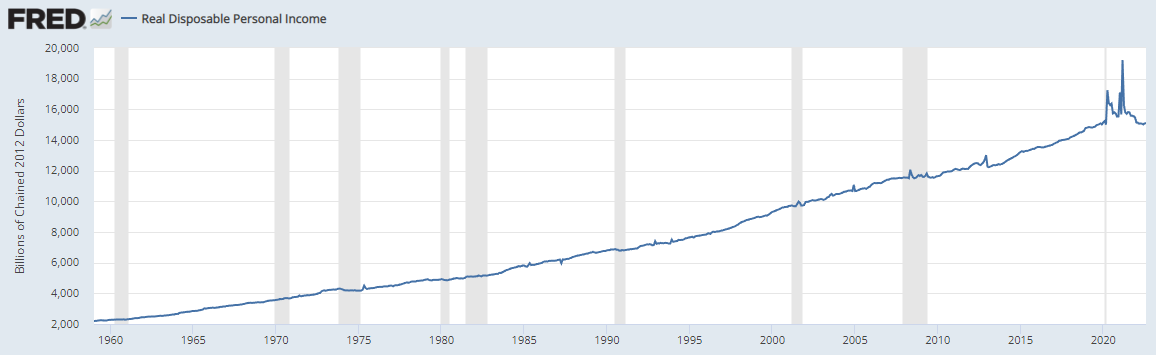

I have shared this chart before, but not with this much history - note the degree to which real disposable personal income spiked via the huge stimulus packages during the pandemic.

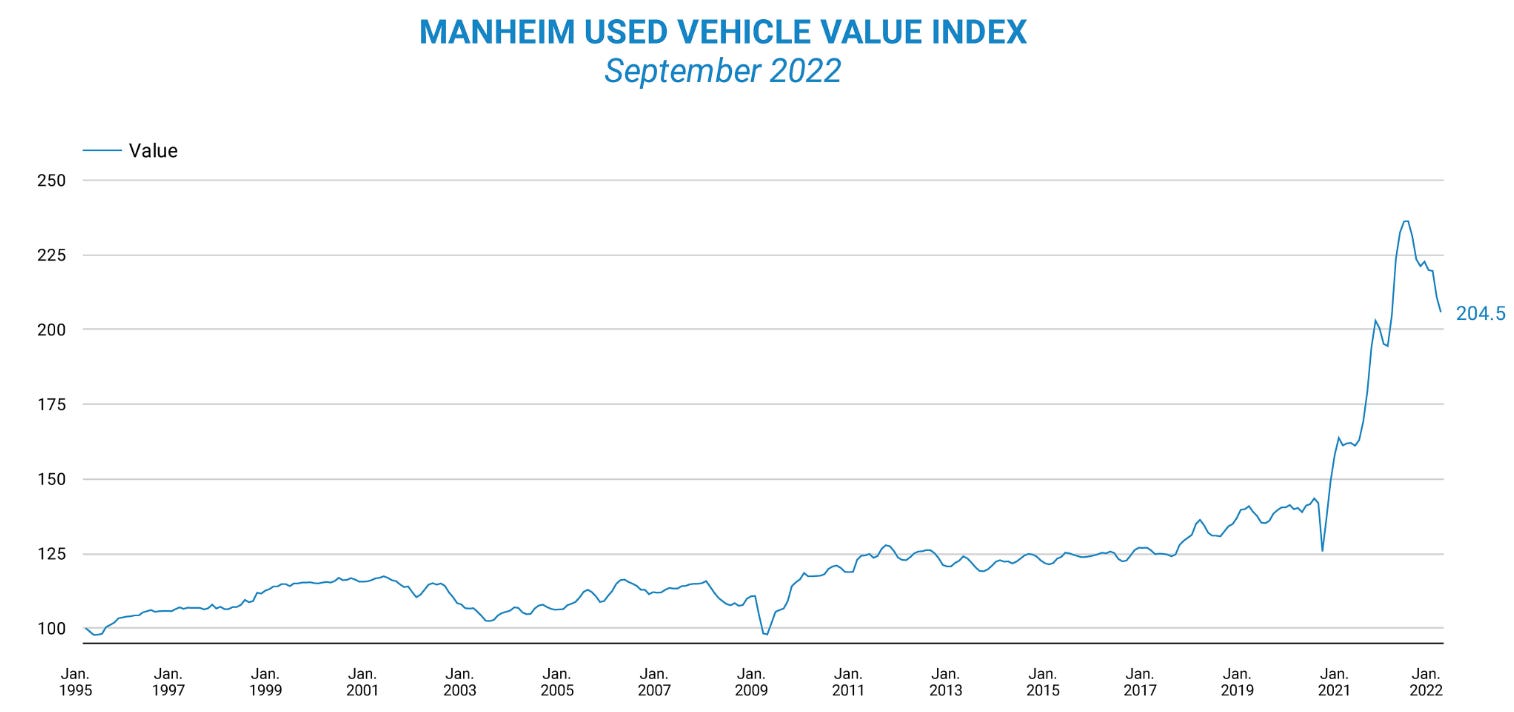

Now imagine that gusher of money funneling into a relatively narrow channel of the economy that was experiencing collapsing global supply chains! Look at that spike in consumer spending on durable goods. These dynamics were/are nonlinear - i.e. price does not respond in an orderly way. Rather it results in what used car prices have done:

The system was/is complex, but the concepts are very simple. Ramp up demand while supply drops, and magically the most fundamental law of economics takes over.

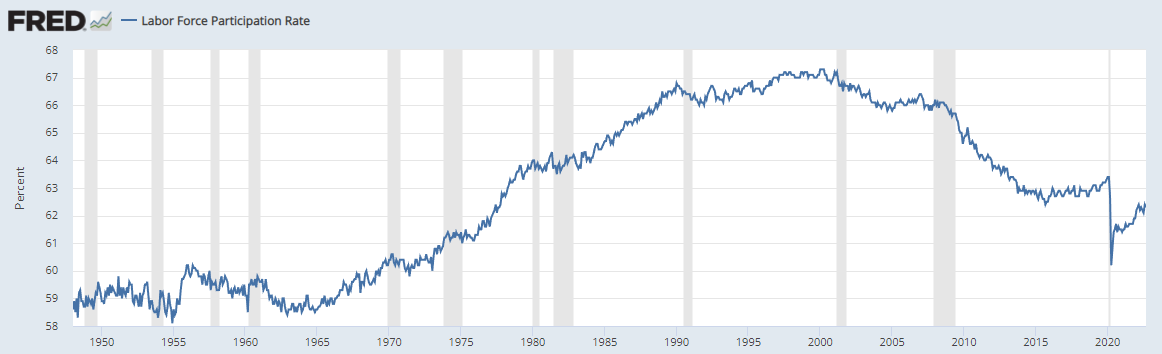

Ah - but what about the labor market and a wage-price spiral? Yes, the official unemployment rate that most people cite (U-3) is around record lows, but it is within this context:

The labor force participation rate has been dropping for years, and the pandemic resulted in a further shock. Many of the baby boomer generation who were approaching retirement, and had enjoyed the largest asset bubble in world history, decided to leave the labor force- at least for a while.

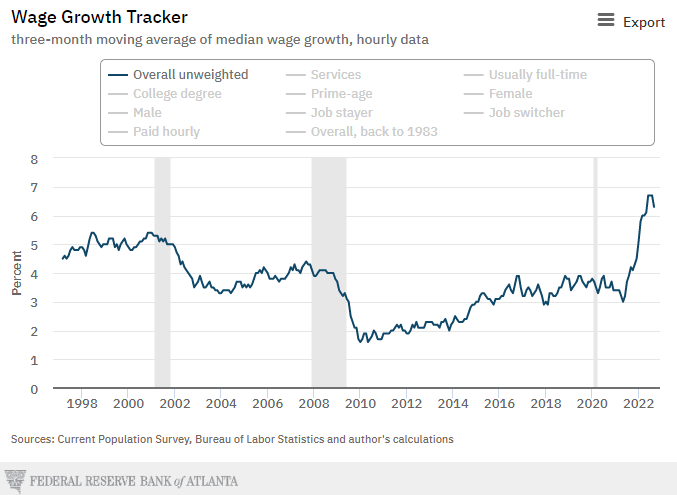

If labor markets were too tight overall, meaning there was an actual wage-price spiral which is to endure on a structural basis, then what’s up with real wages?

Nominal wages are certainly up, as reflected by this Atlanta Fed tracker, but those nominal increases have come amidst the largest cost of living shock in over 40 years. As I have referenced in the past, the official inflation metrics have intentionally been rigged to report lower inflation, and even those continue to be over 8% per this week’s CPI report. For a better sense of what is actually going on in the real economy, S&P 500 company revenues are up in the mid-teens year over year. Let’s split the difference and posit that most people are experiencing 10%-12% CPI-type inflation - so much for that ‘tight’ labor market!

Of course, the huge shocks to the system have resulted in significant misallocation of labor - meaning there are a lot of segments of the economy in dire need of labor due to the same sort of factors that drove used car prices. Labor markets are not nearly dynamic enough to adjust to the sorts of supply/demand shocks that took place, so labor shortages have become widespread as a result. I believe these are also all issues driven by the very specific cyclical factors unfolding.

Throw in the normal ‘python-style’ nature of cyclical inflation dynamics, and many appear terribly confused about what has been and continues to transpire. It takes a while for these forces to work their way through the system, but ‘working’ they are. ECRI’s Future Inflation Gauge, which has been accurately forecasting inflation cycles for decades, began to roll over this summer - likely marking a cyclical peak. It has not yet begun to drop dramatically, but then why would it? The python does not gulp down inflation like it is using a beer funnel.

The idea that the cyclical inflation forces would rectify themselves quickly was behind the “transitory” characterization - that was objectively wrong. But that was a timing issue rather than relating to the attribution of the underlying dynamics. This has resulted in many of the “QE is printing money” mafia (I am a former member!) engaging in orgasmic confirmation bias that it was the Fed that caused this inflation crisis and that the 1970’s have now returned.

This leads me back to the same conclusion explored in Regime Change - the underlying factors of excessive debt and demographics have not changed. The drivers of low/declining monetary velocity have not changed. What could change is how the relative impotence of monetary policy in the face of a severe global recession could result in chapter 2 of the pandemic-era fiscal mania being written.

Washington D.C. never lets a crisis pass without using it to ramp up the grift and kleptocratic allocation of resources, but the vig appears to be going up. The political establishment has merely slowed down the grift, as was on full display with the recent kayfabe-inspired (fake name!) Inflation Reduction Act. Imagine what may emerge if/when the reality of a full-blown severe global recession hits the economy. How much deficit-fueled ‘stimulus’ will be doled out to the masses to placate as even larger chunks get allocated to the usual suspects?

What are the chances that the misallocation of resources and cyclical volatility unleashed by chapter 2 of pandemic-era policies will somehow be less disruptive and more efficient than chapter 1? My guess is pretty low. However, the path to get there is where I believe the nuances laid out in this piece are so important.

Ironically, the misattribution and misunderstanding of the current cyclical inflation dynamics, including by central bankers, are likely to result in a deflation shock - a sort of boomerang effect of the inflation shock. I’d expect things like that Manheim Auto Index to collapse in much the same way that it exploded higher.

It will be this deflation shock that may pave the way for Regime Change amidst the Bizarro Recession, and subsequently birth the economic bastard child of the 1930’s mother and 1970’s father. That is my current base case, but the ‘trigger’ will be when/if the Future Inflation Gauge begins to drop precipitously. I will also be interested to see how the long end of the US Treasury curve acts through such a period, as am not sure when/if it begins to price in the Regime Change scenario.

Thanks for sharing. I appreciate your thought process

Great stuff. Thank you.