Two Utes

The investment industry perpetrates kayfabe on the public, as large institutions that lack the ability to make significant asset allocation decisions without having a material market impact, project those limitations onto individuals. If they were to try and make significant changes to asset allocation in a matter of weeks, or even months, they would cut off their own nice to spite their face.

The result is often a game of relativism rather than absolutism. The vast majority of individuals live in an absolute world, whereas the majority of the advice and products they consume are anchored in a relative one. This gap can be inconsequential for many years, and then become hugely relevant for some segments of investors. Today’s ramblings will use the utility sector as an example to explore this distinction.

The sector has historically been considered a defensive one, or suitable for “Widows and Orphans” given the relative stability in revenues, being highly regulated, and history of paying significant dividends. Many who live in the relative world and decide to shift to be more conservative, will overweight sectors like utilities and healthcare, and underweight sectors like technology and consumer discretionary.

The early portion of my investment life took place during the technology and telecom mania of the second half of the 1990s. Many may have heard or read about the eventual demise of the likes of Worldcom, but the period had a very specific nuance within the relatively small world focused on investing in utilities.

I remember this vividly, as I was an analyst at a wealth management firm at the time, and a long-term client in retirement decided to leave early in 2000. This was after having had more than 15% per annum average performance over the prior decade, most of it being in retirement.

I had a long meeting with the client to recommend that they reduce risk dramatically, including establishing a new position in a boring old electric utility fund. Ultimately, the client decided to have a friend, who was a physician and had recently retired early to trade stocks full-time, help manage their assets.

It was a wild….I cannot remember the name of the utility company, but I believe it was based in Montana, and it changed its name from something like “XYZ Electric” to “Dynamo.com” and saw its stock explode….temporarily.

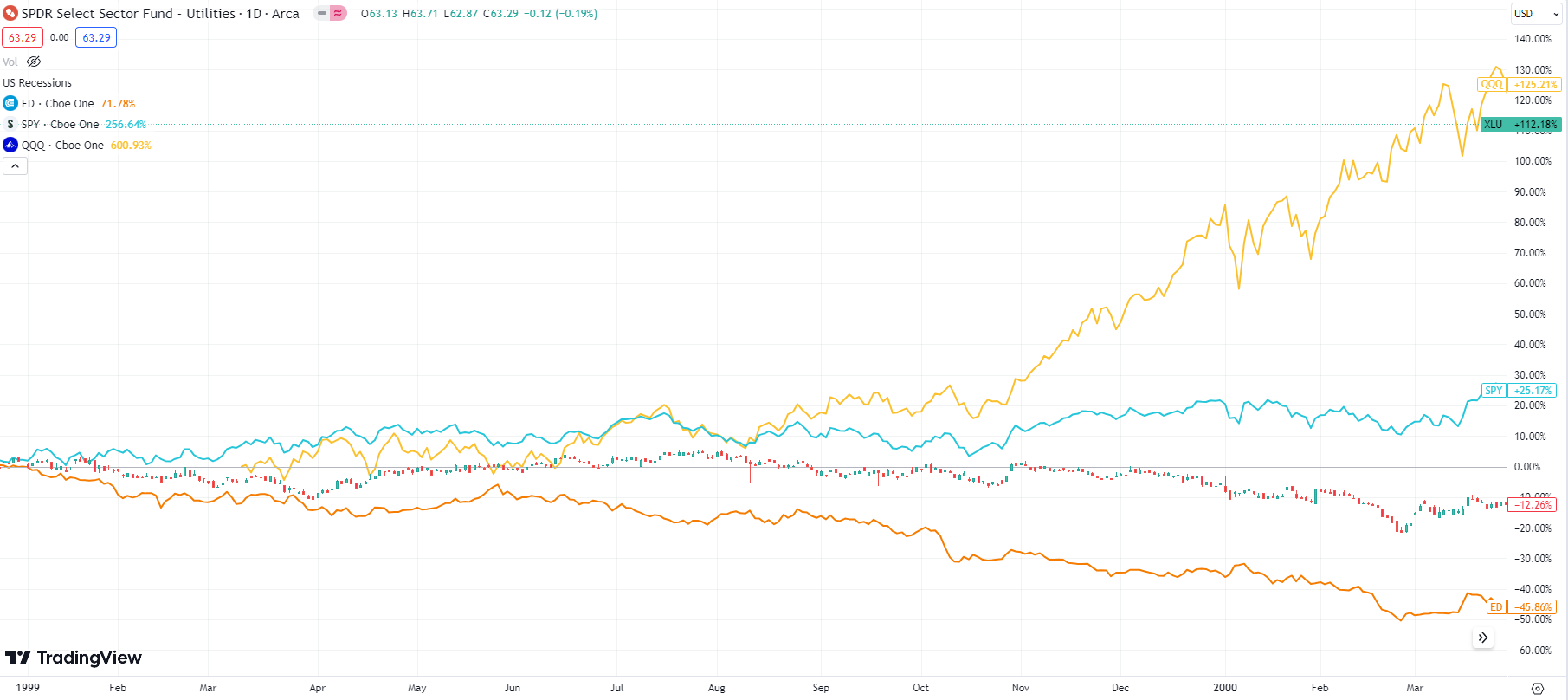

Here is what that crazy period from the start of 1999 up until the bubble peak in late March 2000 looked like for the utility sector SPDR (XLU), Nasdaq 100 (QQQ), S&P 500 (SPY), and “sleepy old” Consolidated Edison (ED):

Con Ed paid a dividend of $2.14 per share in 1999, and at the lows in March 2000 yielded about 8%. For additional context, the capitalization-weighted sector index (XLU) yielded a little under 4%, but by then the index had become heavily impacted by the price increases in the bubble stocks.

Important note - I selected Con Ed based upon recall and do not follow the company. Nothing in this post is intended as advice or recommendation on any specific security, ever. The specific securities are mentioned for illustrative purposes to highlight the kind of risk/reward dynamics present for individuals versus institutional investors within the current market mosaic.

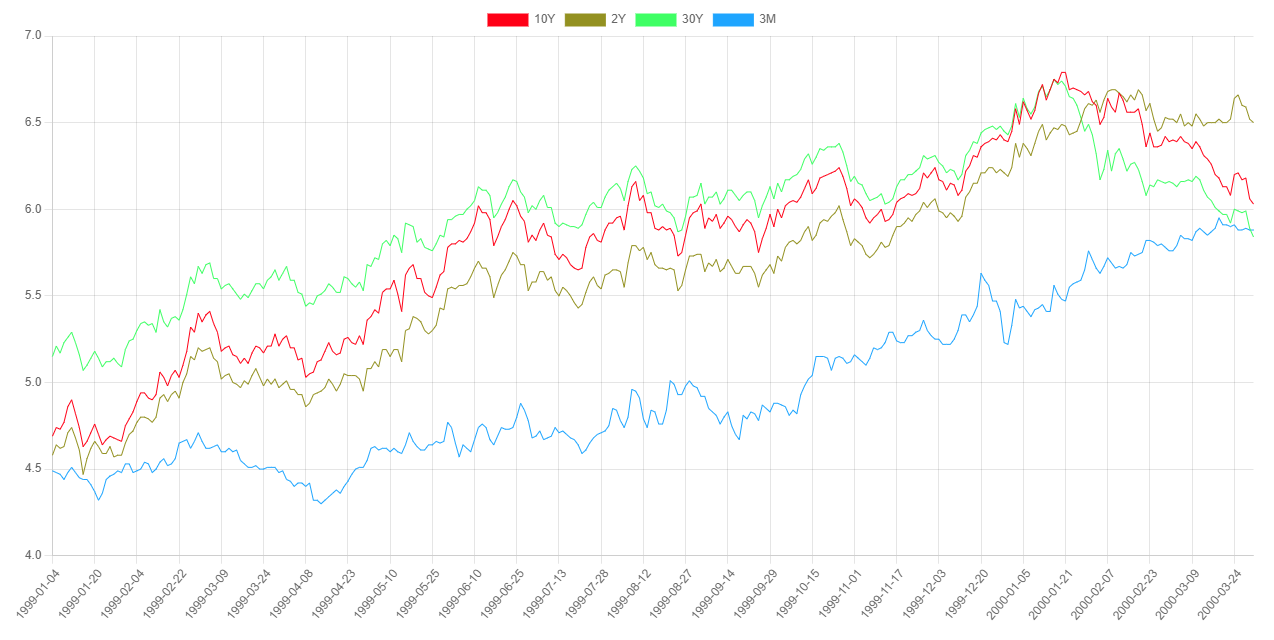

Here was various maturities in the US Treasury yield curve over the period:

The broad CPI year-over-year change for March 2000 is currently reported as 3.76%, with the core version excluding food and energy at 2.45%.

Here are the related yields as of the close of September 22, 2023, and the most recent CPI levels:

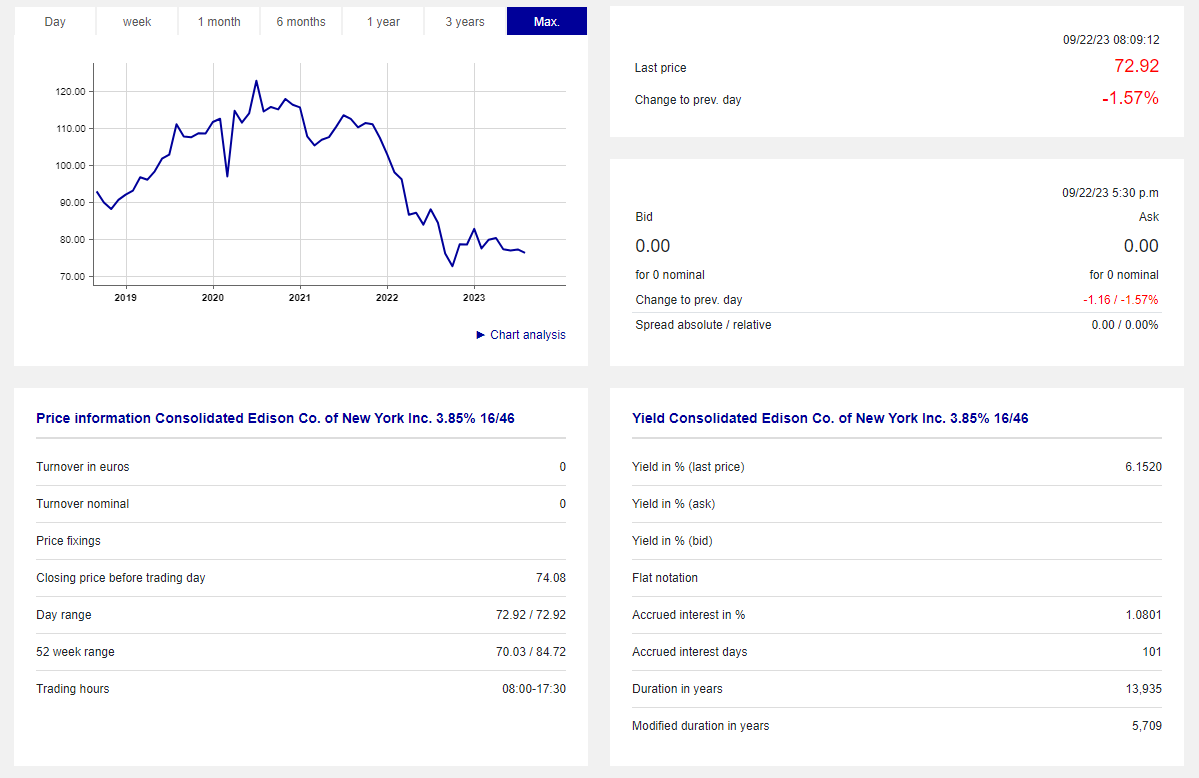

Here is some information and history on one of Con Ed’s long-term bond issues:

I cannot vouch for the accuracy of this information, and individual bonds are often illiquid - particularly for smaller retail investors. But a bond trading at 73% of par with a current yield of about 5.2%, and having about 37% of the current price in capital gains to be amortized over the next 23 years, is notable compared to a stock yielding 3.57%.

The recent mania has been fueled by the widespread adoption of passive flows, such as 401k and other retirement pools, robotically buying market indexes. As we see here with the utilities sector, relative or even absolute valuations are not part of the robotics. Mike Green has written and spoken about these issues and related dynamics over the past several years and remains a good source for related insights.

If your portfolio is not in the hundreds of billions or trillions in value, then why should you invest as if it is? This is another clarion call for individuals, particularly those within or nearing retirement, to resist the robots and use your general intelligence….the robots haven’t won….yet.