Window of Vulnerability

Window of Vulnerability

It's the Economy....Stupid

I will leave the wannabe geopolitical analysis to others, as doing so would be like me pontificating on how to conduct brain surgery. The one thing I will say that directly pertains to the terrible situation unfolding in Ukraine relates to the essence of why I started and named this account ‘Kayfabe Capital.’ The lines between narrative, propaganda, and reality appear extremely blurred, with the potential for ‘fake’ violence exploding into real violence significant. Given the broader societal ‘earthquake’ I have been referencing since the beginning of this letter back in late November 2021, a scale-invariant escalation would, unfortunately, be unsurprising.

As for how this may impact the business cycle and markets, I revert back to my analytical process. It can be ‘boring’ to do so with so much unfolding, between war, global sanctions, etc., but is what I may be able to offer in order to add value to readers.

The global economy was firmly entrenched in a growth rate slow down heading into the current geopolitical crisis. Even prior to the invasion, I referenced that the stage of the business cycle was likely entering a ‘window of vulnerability,’ which is to say that growth had slowed enough that potential shock(s) could kick off a recessionary feedback loop.

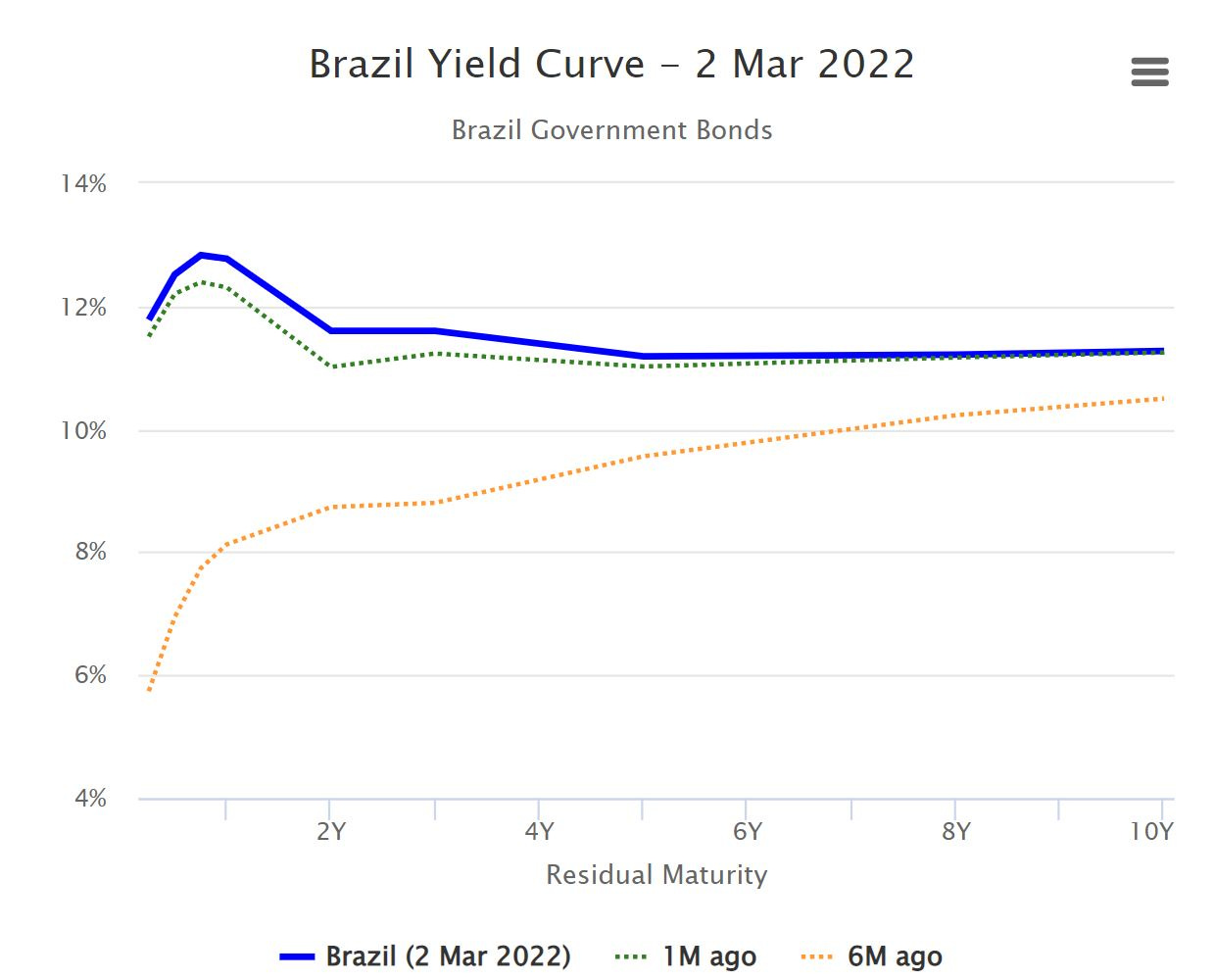

Another theme I have been focused upon has been the likelihood that the US would be towards the tail end of this cycle; meaning other major economies would roll over first. China has led the way, and now we are seeing worrying signs across various large emerging economies. Here is the yield curve in Brazil, for example:

That follows what had been an inversion developing in Brazil’s forward curve late last year. With many commodity prices exploding and emerging market currencies going down significantly versus the US dollar, full-blown financial and political crises in those countries most impacted may just be getting started, unfortunately. The recent large upturn in agricultural commodities is particularly worrisome.

The German Bundesbank declared 9 days ago that their economy was likely entering a new recession, though the narrative was largely focused upon omicron. Are recent events likely to accelerate or ameliorate the potential recessionary feedback loop in Germany? The German DAX seems to be awakening to the risks:

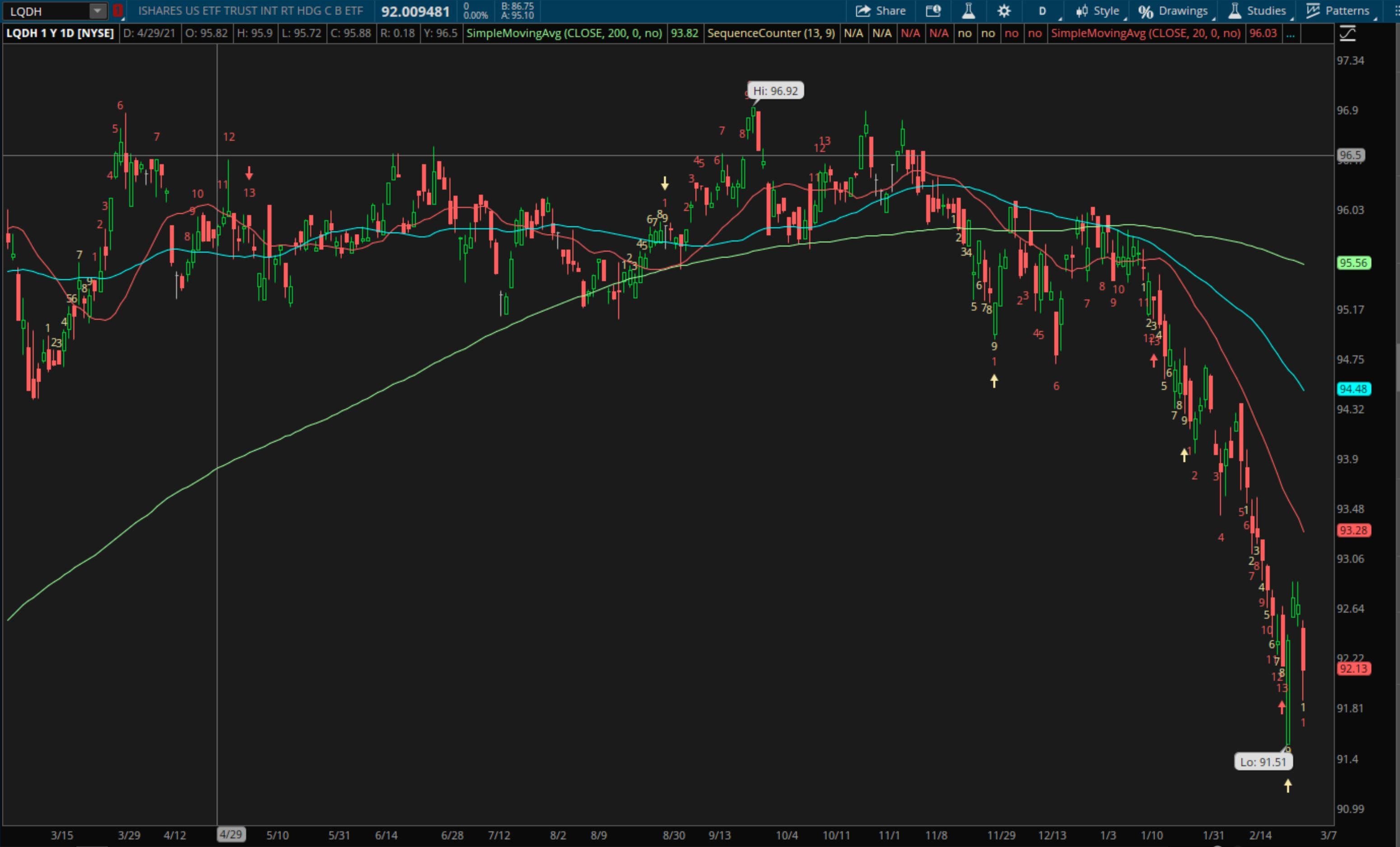

Here is a 1-year daily chart of an ETF which is a decent proxy for US investment-grade corporate bond credit spreads:

Looking at it from this perspective, one could draw the conclusion that spreads have widened quite a bit! Here is a monthly chart dating back to the middle of 2014:

That drop in 2016 was amidst a global growth rate slowdown which resulted in a soft landing rather than a US recession. We can see that spreads are likely to have a lot of potential room to widen should the global slowdown evolve into a recession which drags the US economy down with it.

Is the US well-positioned for a potential recession? The Fed remains oriented towards tightening, though that may be fluid depending on how things evolve in the coming weeks. Huge spikes in many commodities and additional supply chain issues surrounding the geopolitical crisis are likely to further complicate extracting signals from noise relative to inflationary forces and trends. Before all of these recent developments, here was where real weekly average earnings in the US were, with the graph courtesy of Hoisington Asset Management:

Any recollection of where crude oil prices were in July 2008? Despite the US economy being seven months into a recession most remained oblivious to, WTI crude marched on to peak above $147 a barrel, before crashing to below $34 over the subsequent six months.

30-year US treasury yields peaked at a little over 2.50% just under a year ago, and in close proximity to the global economy beginning to decelerate. The recent flight to US dollar assets and treasuries has pushed the yield down to about 2.10% as of this writing. With many still understandably focused upon the huge upturn in inflation, markets are beginning to discount the risks of a deflationary/recessionary bust, in my opinion. Perhaps it is not too late for things to stabilize and a recessionary feedback loop not taking hold in the US. Maybe peace can be negotiated relatively quickly and liquidity and counterparty risks related to sanctions can also be alleviated before contagion spreads.

However, given where US markets are trading, they are nowhere near discounting current risks, in my opinion - kind of like when the Brazilian Bovespa was similarly in La La Land as it made an all-time high in June 2008.