A Young Powell

The Worked Shoot was launched just over a year ago to provide a vehicle for me to try and help anyone crazy enough to listen navigate what I expected to be an extremely challenging business cycle and financial market period. So far, 2022 has lived up to the ‘hype.’ Could 2023 throw an unexpected curveball into the mix? Could a soft landing or mild recession generate a potential echo in history, back to the roaring 1920s?

There were obvious and important differences between that and the present era, with a version of a gold standard in existence at that time. However, some of the parallels are of note, and something historically atypical happened during the roaring 20s- a period when the stock market blew right through a recession.

The official NBER cycle dates for the thirteen-month-long recession were from October 1926 to November 1927. It was the second relatively mild recession subsequent to the recovery coming out of the 1920-1921 depression, and the stock market hardly blinked.

That was a weekly chart of the Dow Jones Industrial Average over the period, with smiley and frowny faces having marked NBER cycle dates.

Is it possible that a ‘Fed Pivot’ could result in a period similar to the late 1920s? Could a relatively mild recession in 2023 result in massive Fed and fiscal stimulus that reignites financial markets? Anything is possible! However, is it likely?

First, some other important differences between that era and the present. The 1926-1927 recession has been given the “September 11th, 2001 treatment” within historical accounts, IMO. Similar to many to this day stating that 9/11 ‘caused’ the 2001 recession, it had already begun in March 2001 and actually concluded shortly after, that November.

Similarly, the 1926-1927 ‘legend’ has been that Henry Ford’s decision to abandon the Model T car and shut down his company’s manufacturing to shift to the Model A, along with the 60,000+ workers displaced, had caused that recession. The Ford decision occurred in May 1927, well after the recession had already begun, and was partly made due to the accompanying weakening in demand.

The 1920s were a period emersed in changes to the financial system, with the Federal Reserve having been started in 1913. This Bank of International Settlements paper from September 2003 offers some interesting research and characterizations of the period:

The 1920s saw the spread from Britain to America of the investment trust, an entity that had existed in England for half a century, but now in a variant that allowed the manager of the trust to buy stocks on margin, raising the fund=s leverage. This anticipates a theme we develop later in the paper B that the consequences of credit expansion and the extent of the boom thereby induced may depend on the structure and regulation of the financial sector. Individual investors were similarly permitted to purchase shares for 10 per cent down, borrowing from their brokers who in turn borrowed from the banks. Capital gains on the representative portfolio of nearly 30 percent in calendar year 1927 and more than 30 per cent in calendar year 1928 encouraged the belief that stocks could only go up.

How about that section on individual investors- BTFD, baby! The US experienced a large relative degree of credit expansion following the Fed’s creation:

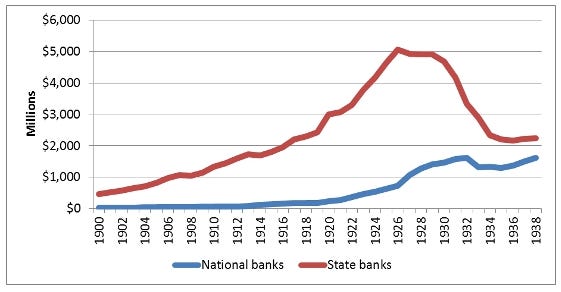

The Fed has long been the inspiration for various conspiracy theories, but its history and incentives seem pretty clear, IMO - facilitate credit creation and advance the interests of its constituents, which started as national banks and migrated towards what we now call the ‘Too Big to Fail’ banks. Part of this migration in power manifested during this 1920s period, with various reforms, including the McFadden Act of 1927. Regardless of one’s views on whether such changes were a good idea, the practical implications were the following:

That chart showed that national banks’ real estate lending went on the ascendancy in 1927, with state banks limping through the late 20s, and then ‘enjoyed’ a dinosaur-level extinction event during the Great Depression.

The credit creation boom of the 1920s manifested in various property bubbles, including an infamous one in Florida which attracted the likes of Charles Ponzi, in what became a sequel act to his first Ponzi in Boston during the early 20s. That bubble began to go bust during the 1926-1927 recession following a damaging hurricane, but the credit creation engine metastasized into consumer lending, commercial real estate (Empire State Building!), and financial markets. Once again from the BIS paper:

U.S. bank reserves grew faster in the second half of 1927 than in any other semester of the 1920s. This supports the notion that the ready availability of credit to the American economy was a factor shaping the expansion of the later 1920s. Moreover, that expansion was heavily driven by spending on consumer durables purchased on the installment plan (Olney 1990), using credit provided mainly by nonbank lenders (finance companies, which had developed previously to finance purchases of income earning durable goods like sewing machines and pianos but acquired new importance on the American scene when in the 1920s the major automobile producers established divisions and subsidiaries designed to finance purchases of their own durable goods), and by purchases of financial assets, financed with bank credit funneled to investors through their brokers (White 1990b). The consequences showed up not just in the stock market, but in the burgeoning automobile industry, the leading sector of the 1920s, and in the commercial property market, which boomed in virtually every American city. It is no coincidence, for example, that the late 1920s was the occasion for the appearance of the modern high-rise, when the skylines of many American cities were defined.

The credit boom enabled production to keep up with the explosion in demand, with consumer prices and interest rates remaining relatively low. The CPI from 1923 through 1929 was 1.8%, 0.4%, 2.4%, 0.9%, -1.9%, -1.2%, and 0.0%, as the gold-linked monetary system persisted. Indeed, consumer prices deflated per the CPI through 1927, 1928, and much of 1929. This chart shows various interest rates during the period:

We can see that the one rate which went appreciably higher towards the end of the 1920s was the one to finance broker loans, which were at that point engaged in the epic amount of lending to speculators.

Boom turned to bust in 1929. The Fed, concerned that the high level of the stock market was diverting resources from more productive uses and heightening financial fragility, began raising its discount rate in 1928; higher U.S. rates in turn curtailed capital flows to Europe and Latin America, forcing central banks there to tighten to prevent their currencies from weakening.

Various aspects of the era may ring familiar, but my concern is that those forecasting and/or relying upon a 1926-1927 scenario may be missing the potential that we already experienced it during the 2020-2021 pandemic period.

Margin debt exploded as markets exploded off the spring 2020 lows, and we are now beginning to see various other leverage-induced schemes born out of the zero percent interest rate era beginning to implode. The LDI-induced crisis in the UK pension system came out of ‘nowhere’ in September, with various other leveraged and illiquid schemes likely lurking in private equity, etc.

The orgy of pandemic-era capital flowing into the US, as well as many other developed economy’s property markets, was on an epic scale.

Is it possible that we had a bizarro sort of property market dynamic recently compared to the 1920s? This time the commercial markets boom peaked prior to the lockdowns and has limped through since, with the residential segment exploding. In just two years, growth in residential construction spending exceeded the amount spent in the six years preceding the 2006 housing bubble peak, which preceded the Global Financial Crisis (GFC).

While the monetary system is different and the associated policy responses are likely to be as well, the 2020-2021 period offered a lot of the elements present from 1927-1929, with the added complicating factors which accompanied the pandemic period, such as supply chain disruptions, the huge cyclical upturn in inflation, and the global financial war declared in response to Russia’s invasion of Ukraine.

To revisit part of the quote from above:

Capital gains on the representative portfolio of nearly 30 percent in calendar year 1927 and more than 30 per cent in calendar year 1928 encouraged the belief that stocks could only go up.

That period of mania took time to diffuse, as hope and optimism heading into 1930 appear to have been persistent, as characterized by Megan McArdle in the spring of 2009:

I don't want to push the Great Depression analogy too far, but what's surprising when you go back to primary sources from 1930 is the optimism. I don't mean to imply that everyone thinks things are just swell. But while you know that they are facing the worst economic decade of the twentieth century, they don't. They're expecting something more like the recession that followed World War I. People are cutting back, but they're still spending, particularly because companies are slashing prices to move inventory. It was the long grind of the years that followed, and the catastrophe of the second banking crisis, that scarred them permanently. And this shows up in the economics stats and the stock market, which did not, as we like to imagine, simply decline in a straight line.

That optimism took place during a massive rally in US stocks which persisted for six months after the initial crash in October 1929.

Cycles are all different, and as ‘they say' history rhymes and does not repeat. However, given what my analytical framework is currently suggesting, Jerome Powell’s fear of missing out on being the next Paul Volcker may ultimately result in his being considered another Roy Young.

In my opinion, investors would be wise to continue with extreme caution until long leading economic indicators turn higher.

Another excellent piece - Thanks!

Your writing is masterful. Thank you for sharing such rich analysis. Extra interesting and messy times ahead.