Bob Dylan, LLC

Registered Investment Advisers, or RIA’s, manage somewhere around $100 trillion in assets in the US. One of the competitive advantages touted by the industry is their legal mandate to perform their jobs as fiduciaries, which means they must place their clients’ interests ahead of their own. This was/is supposedly different than the old commission-based compensation system which was ubiquitous for decades.

With that asset base, 1% of AUM would be fees around $1 trillion! In order to earn those fees, they typically perform asset allocation/portfolio management duties, some do varying degrees of financial/estate/tax planning, with a small number offering pseudo family office-type concierge services. To put it bluntly, they have been huge beneficiaries of the ‘Lacy Hunt’ regime chronicled in this letter in April, as stocks and bonds remained in relentless bull markets, with only brief interludes, for over a decade. Unfortunately for many, I fear:

Having grown up in a working class family a block up from a trailer park, perhaps like many people, I placed physicians on a pedestal. That kayfabe persisted until I met my wife when she was attending medical school, and over the subsequent weeks, months, years, and now decades, the reality became clear. They are no different than mechanics, plumbers, ……or financial advisers - basically a normal distribution of competency.

But as we saw during the pandemic, a supposed system that was ‘bottoms-up,’ in which the patient-doctor relationship was supreme, had the tails of the distribution chopped off as a matter of top-down public health policy. Regardless of one’s view of whether that was warranted, good policy, or ultimately resulted in worthwhile net outcomes, it happened.

Doctors who advocated for early treatment and using repurposed drugs were censored, shunned, and attacked by their employers, and government bureaucrats. Perhaps some were/are quacks that would have killed patients, while others may have figured out efficacious early treatments. The specifics on that domain are above my pay grade.

However, the sanctity of one-patient-one-doctor was a sort of ‘shoot.’ The pandemic resulted in the kayfabe-style delusion about the patient-doctor relationship being destroyed for many. Preference falsification appears to have become endemic over the duration of the pandemic, with official public health policies which were very difficult to understand if they were actually driven by the interests of….public health - for children, in particular.

Of course, the regulatory capture, hospital system rollups, etc. which empowered and encouraged all this to occur took decades to form. The pandemic served to expose what had become inherently unstable underlying system dynamics. I think the investment advisory industry is on the cusp of a similar tectonic shift where a vast delusion will be destroyed for many.

Similar structural factors exist in the advisory industry, as weird as it may seem to compare the two. The regulatory capture appears systemic across industries, and the confluence of large custodians and the ‘cult’ of passive have made the industry similar in the ‘rollup’ sense. Like doctors working for the big hospital systems, financial advisers are basically cyborgs working as part of the Borg’s hive mind.

The incentives are aligned with being part of the collective, as clients losing 50% of their assets is not viewed as an existential business threat as long as one remains within the hive mind. Maintain that strategic asset allocation, and a sort of business risk immunity is conveyed upon thee - at least from a regulatory perspective.

Whether it is lifestyle funds within corporate retirement plans, ETF portfolios, or the cult of Bogle, the industry has evolved into a hypercritical state similar to where the healthcare system was pre-pandemic, in my opinion, all while collecting huge fees under the delusion that they are acting as individualized financial fiduciaries.

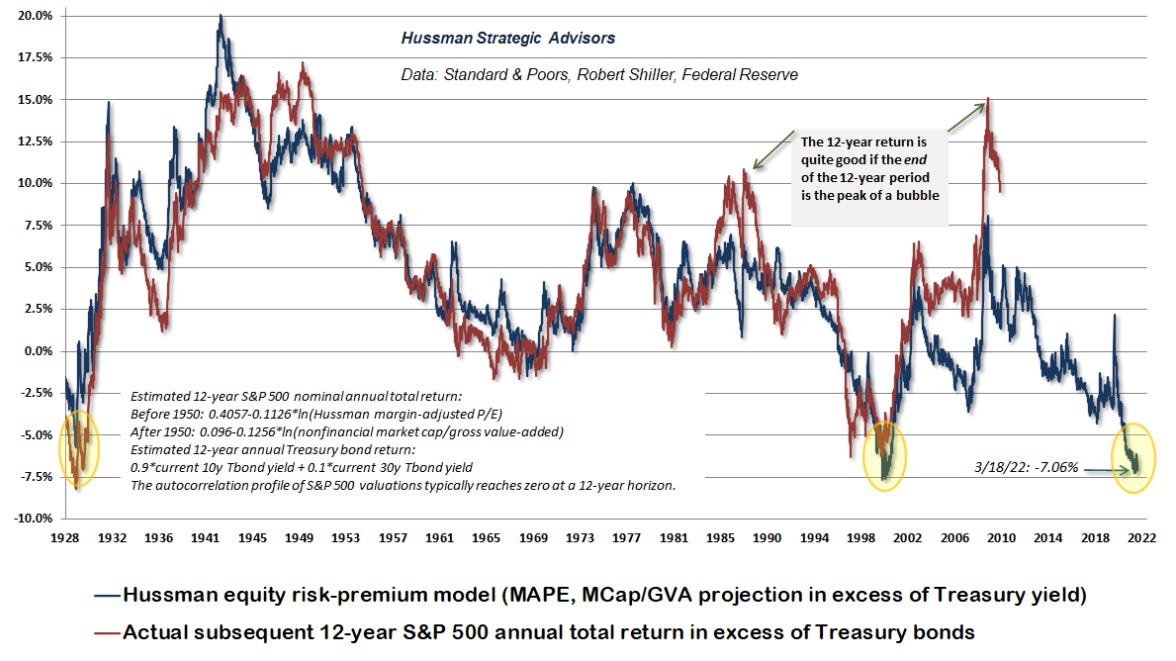

As the bubbles continued to inflate, charts like the one above from John Hussman’s March 2022 commentary were disregarded. An investment adviser who may have decided to pursue ‘early treatment’ likely confronted unhappy clients and even possible regulatory scrutiny. How could a financial fiduciary advocate for holding 60%+ of clients’ assets in a passive stock portfolio with expected long-term returns which were negative relative to the ‘risk-free’ alternative? Who in their right mind could have persisted with early treatment for 8+ years!? Reckless monetary and fiscal policies have incentivized the opposite of fiduciary.

A global recessionary-induced bear market will be the ‘pandemic’ event for the investment advisory business, in my opinion. Many will probably experience cognitive dissonance and blame events outside their control, both advisers and their clients. That damn Federal Reserve!

However, similar to what has occurred with the healthcare system, I suspect there will be a large number who realize that the supposed ‘fiduciaries’ are fake.

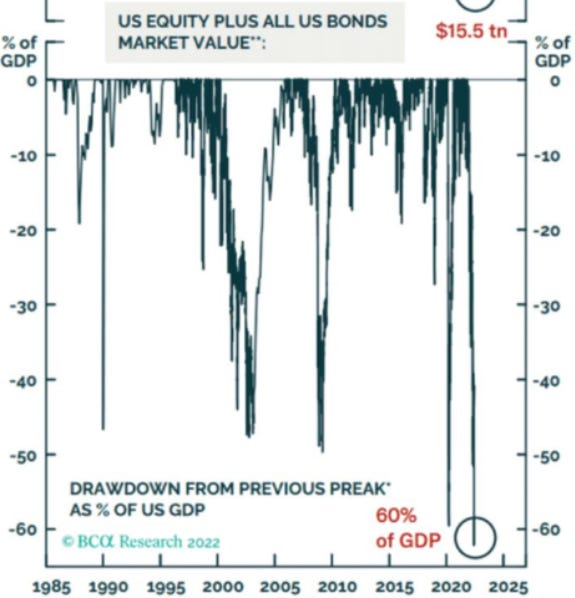

With equity valuations having reached levels never before seen, and the 10-year US Treasury having reached a 0.40% yield at the nadir of the March 2020 pandemic panic, this chart should not be all that surprising. For investors in or approaching retirement, at some point should a financial fiduciary have pursued ‘early treatment’? The wealth decline in stocks and bonds has already been colossal, and that has been with real estate values still going up sharply, equity valuations still high, and before a significant downturn in credit markets.

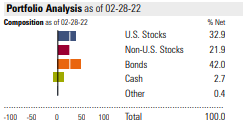

Just as the ‘non-profit’ health systems operate ‘for profit,’ the investment advisory business is not what it says it is. Here was the asset allocation of one prominent 2025 target date retirement fund with about $80 billion in AUM as of 2-28-2022:

The fund is down about 15% for the year. Many investors have probably been seeking counsel from their advisers, and getting the financial equivalent of ‘go home, take Tylenol, and go to the ER if you turn blue.’

There are ways to operate as a ‘subversive’ within the Borg, though they can be like finding needles in a haystack. I shared one in this letter on January 19th. It is a ‘fake’ small-cap value fund that was up 1.18% over the first six months of 2022 vs declines of over 14% for its peer group and relevant passive indexes. I am sure it will come as a SHOCK to everyone that the fund now has about $175 million in assets under management, though that is up from $81 million!

In an industry where ‘cash’ remains a four letter word, one must be creative. Systemic change would create paradoxical self-harm, which reinforces why it is unlikely on a proactive basis. The Titanic is too big to turn at this point, so better get on one of the lifeboats while you still can? Most ‘fiduciaries’ are unlikely to do anything even as The Times They Are A-Changin’.

100% agree. I used to work as an advisor...and too many times was confronted with compliance keeping me from....advising. I left a few years back and think often of my clients who could only hold max 2% cash and of the growth allocation (most over 50%)....20% was to be allocated to tech. And everyone got the call to buy the dip when the market was down 10%.

Christopher Cole of Artemis Capital called recency bias a systemic risk. This article is interesting in that it disputes the role of 'fiduciary' and uses the analogy of "non-profit" medical systems as being for profit (correct). The fact is that the FED's zero rate and "wealth effect" have profoundly framed investor expectations and basically it is hard to swim against the tide. But yes if an RIA suggests going to cash or some out of the mainstream strategy they will be met with push-back. The mindset (i.e. borg) is that the fed has your back, fed put, etc. etc. In other words most expectations are still an extrapolation of the last decade plus of policy folly as far as main street goes.