Cycles are a Bitch

Cycles are woefully underappreciated in the realm of economics and financial markets, IMO. As with much of contemporary life, many seem to get wrapped up in narratives and descend into confirmation bias. My goal today is to KISS the cycle- keep it simple, stupid.

Firstly, it is important to acknowledge that the vast majority of economists are not students of the business cycle- they are closer to astrologers/alchemists than ‘scientists.’ I largely ignore what mainstream economists produce/say, outside of trying to gauge how far off the consensus may be versus reality.

Here is what I think we know- reliable economic indicators (I prefer ECRI’s) began rolling over last spring, with the global industrial cycle leading the slowdown. Those indicators had turned up sharply in summer 2020, as the world began to ‘restart’ following lockdowns.

Note the huge upturn in shipping activity and the world business cycle shown in the chart, courtesy of CrossBorderCapital. That upturn in industrial production was then followed by an upturn in ECRI’s leading indicator for US inflation in the autumn, which we have certainly seen subsequently, with recent readings for inflation at 4-decade highs.

So those indicators anticipated the upturns, with industrial growth being flagged in the spring, followed by US growth last summer, and then recently inflation - all suggesting growth cycle downturns. That condition is NOT the same as forecasting a recession, or deflation, but rather a slowing of growth rate in the economy and inflation. For example, a potential deceleration from 6% to 3% would be a ‘growth rate cycle downturn.’

Why is this important? From a cycle perspective, slowdowns either result in a soft landing and re-acceleration in growth which extends the business cycle, or the reflexive feedback loop of recession is triggered and an economic contraction ends the expansion. As the chart above suggests, market economies respond to price signals. The recent initial Q4 GDP report for the US came in at 6.9% - some ‘slowdown’! The composition of the report, along with a plethora of other data signals, suggests a significant deceleration in demand with large inventory builds occurring. Yes, building empty cities or manufactured goods which sit in warehouses for months do boost GDP as they are ‘created.’

As a slowdown unfolds and moves closer and closer to the zero bound, the economy becomes more vulnerable to shocks. A shock can be a war, a financial sector meltdown, or lockdowns from a pandemic - conceptually, the ‘what’ is less important than the ‘why.’

For example, the US economy was actually in the early stages of re-accelerating via a growth rate cycle upturn in early 2020 just as the pandemic descended upon the world. The economy was in an extremely resilient condition, yet the shortest and sharpest recession on record transpired - lockdowns were like a 1,000-ton boulder that was dropped on the world’s strongest pool cover. Even an extremely resilient economy was no match for lockdowns.

Each recession and cycle is different in detail, but the sequencing is usually pretty simple. The 2020 recession was unusual for the obvious reasons just described. However, globalization over the past 50 years has added another layer of complexity, as the business cycles of geographic regions and countries have become more intertwined. Global recessions, like the one in 2008-2009, create an even larger feedback loop across the world.

For the current cycle, regions and countries outside the US were the first to roll over and slow - emerging economies and China being central. Those countries have been enduring significant inflation, with the added kicker for many emerging market countries, of having had significant financing risks due to US dollar-denominated funding requirements. Here is a 10-year chart of the US dollar versus Chilean Peso, with Chile having been one of the more fiscally prudent emerging sovereigns historically.

There have been some recent signs that China’s slowdown may be decelerating, but they are not yet significant enough, IMO, to become sanguine from a cyclical perspective. Many emerging economies are now a year into monetary tightening cycles, with their yield curves having already, or beginning to, invert - meaning short-term rates become higher than longer-term rates. Flattening yield curves have been far better at ‘forecasting’ economic slowdowns, and inverted curves at forecasting recessions, than alchemi…I mean economists.

So from a business cycle perspective, the Titanic has turned down and leading indicators that are designed to identify when things may turn back up are still pointing down. That does not mean a recession is fait accompli, but risks are likely rising fast and the economy/pool cover becoming increasingly vulnerable to smaller ‘boulders.’

That is the objective portion of this week’s commentary, so now we move on to the subjective. There is much confusion amongst investors as business cycles transition through various stages. At present, I think there is a potentially huge analytical error that has taken root and could catalyze various ‘shocks.’

As I covered last week, Quantitative Easing (QE) and the relative expansion of central bank balance sheets have served to inflate asset prices. It has largely been huge shifts in supply and demand curves that have fueled the large upturn in consumer inflation rates. Many see central banks as being woefully behind the curve and badly in need of raising short-term interest rates to try and curb consumer inflation. From a monetary perspective, that makes little sense, outside of intentionally trying to start a business cycle contraction which shifts the demand curve (i.e. recession) in order to subsequently shift supply curves in response.

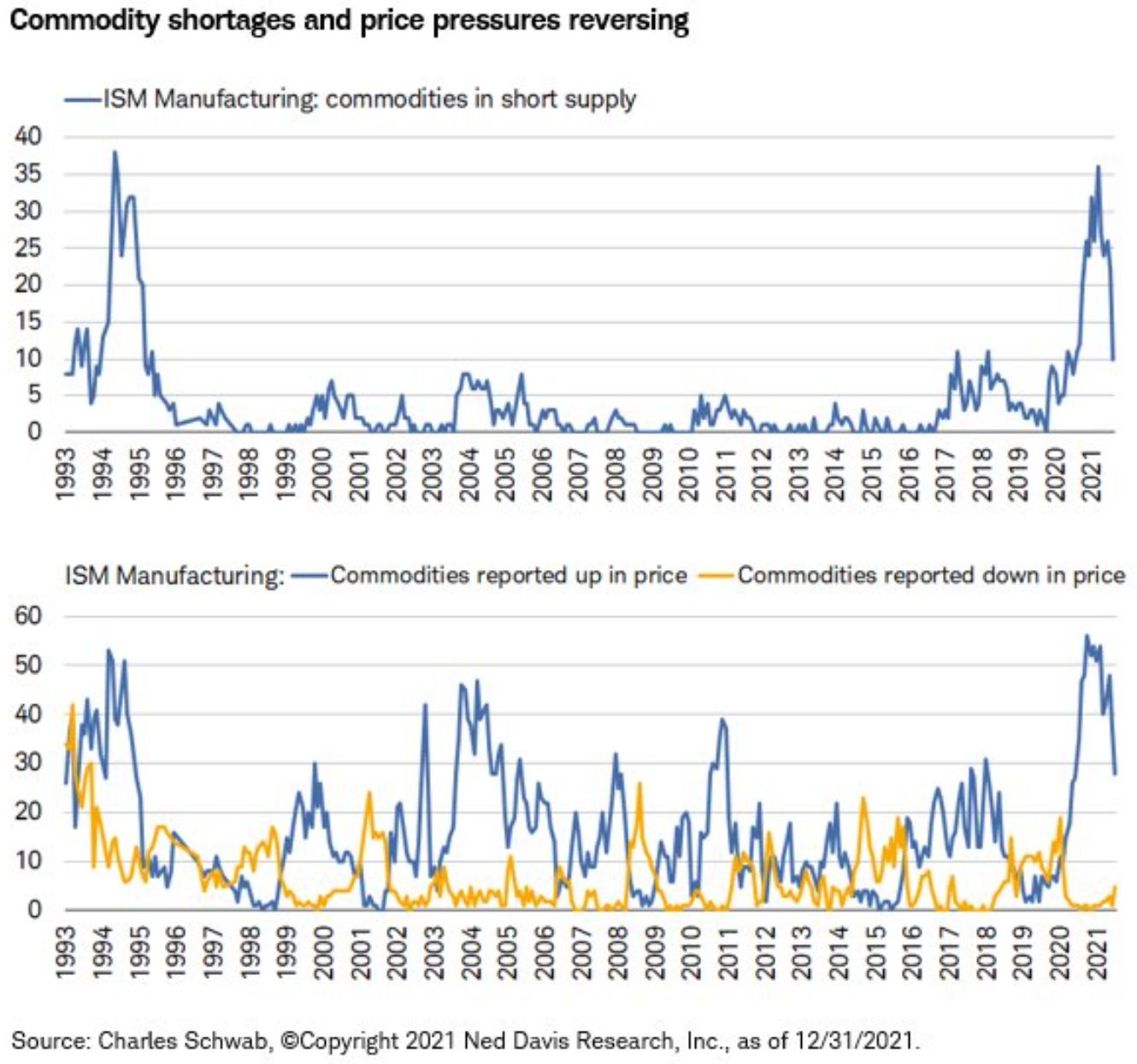

In other words, it is an incredibly blunt instrument for addressing the underlying drivers of the consumer inflation upturn. What it is NOT a blunt instrument is financial assets. As shown above, in the ISM chart, the market economy is already beginning to adjust to the shifts in supply and demand curves without central bank intervention. Here is another example:

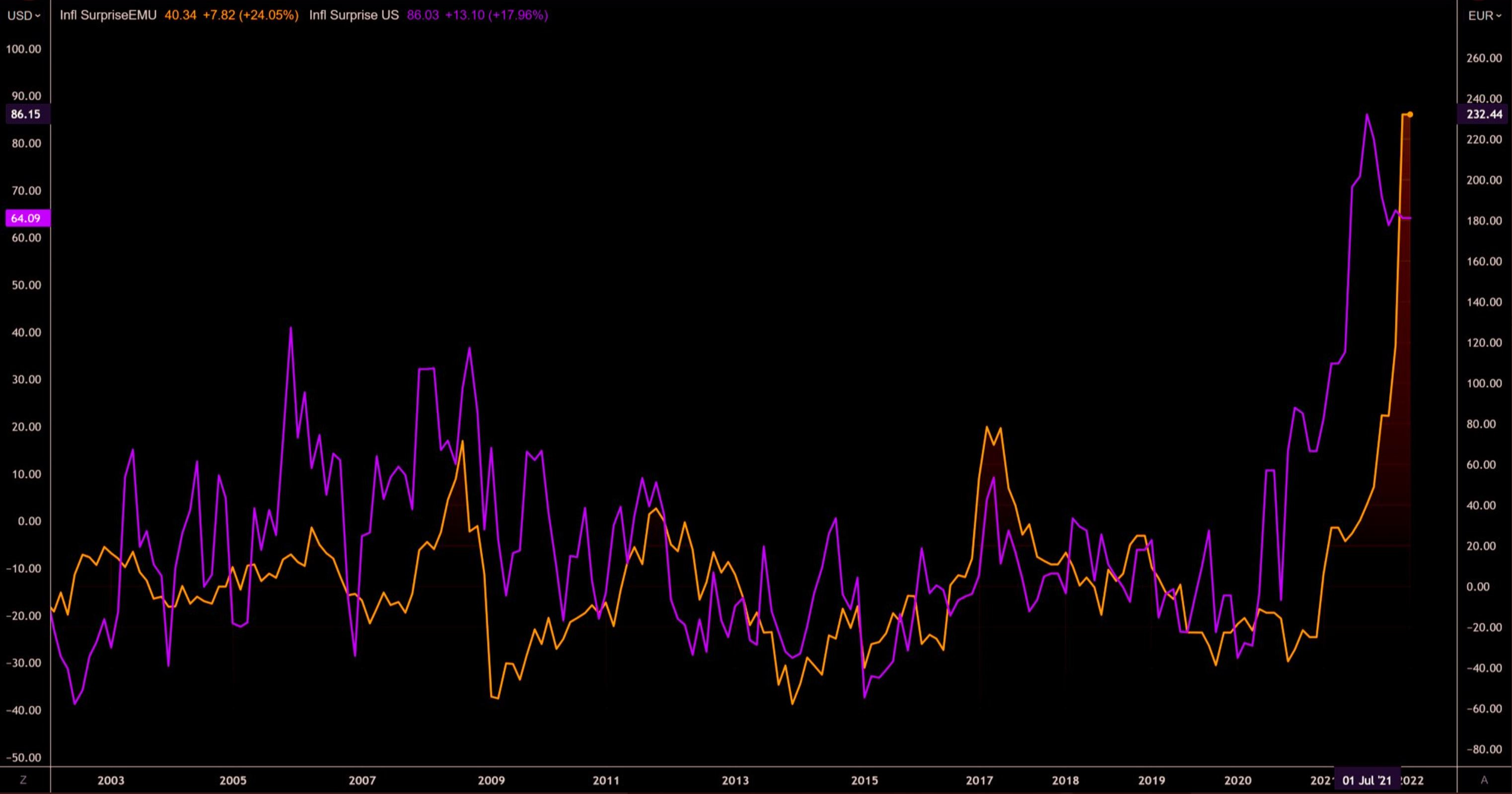

US inflation data is already starting to ‘surprise’ to the downside, with the Eurozone (high consumer inflation data reported today, as they have their own specific energy crisis) likely to follow the US.

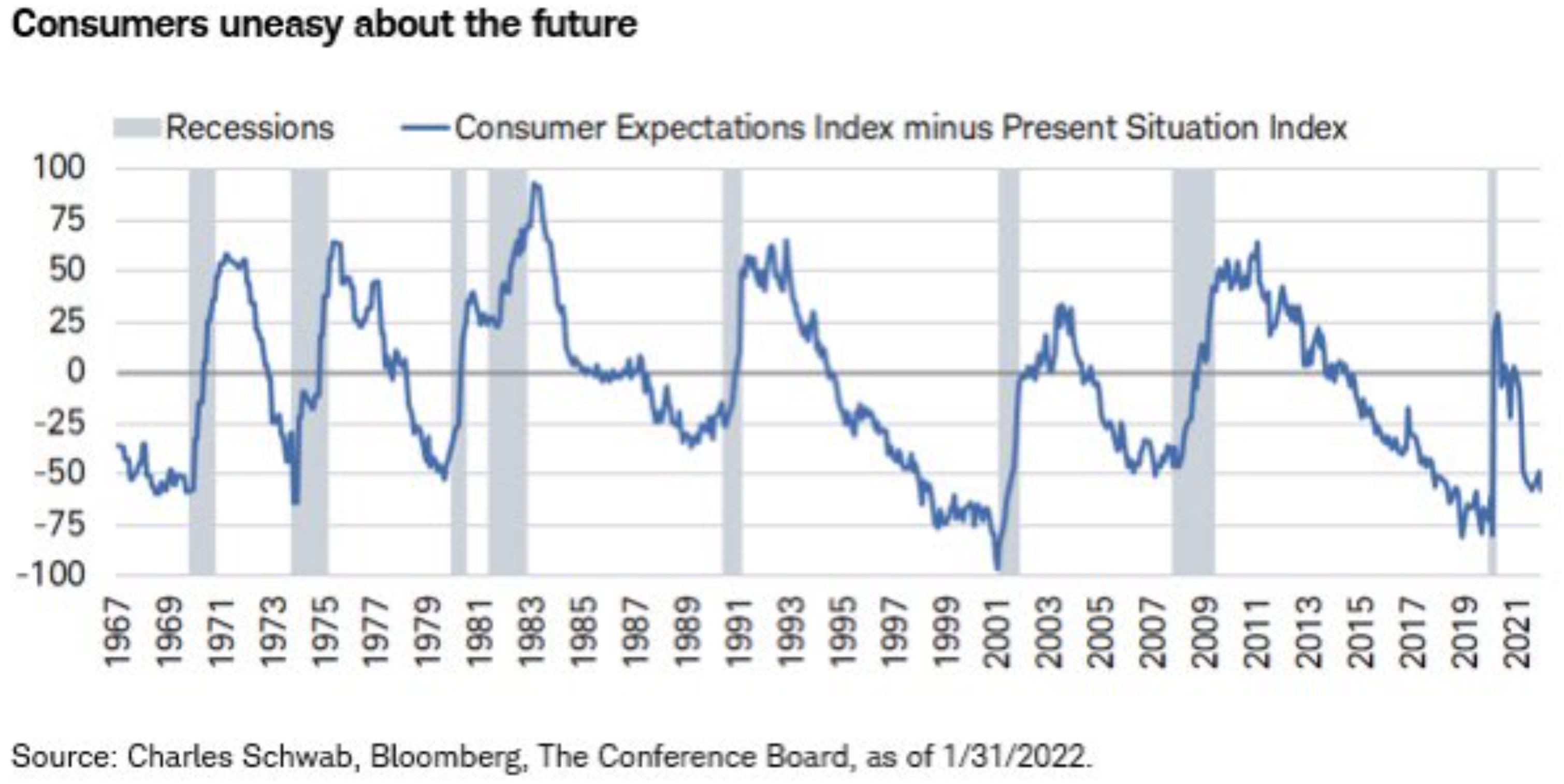

Higher consumer inflation is harming consumer confidence:

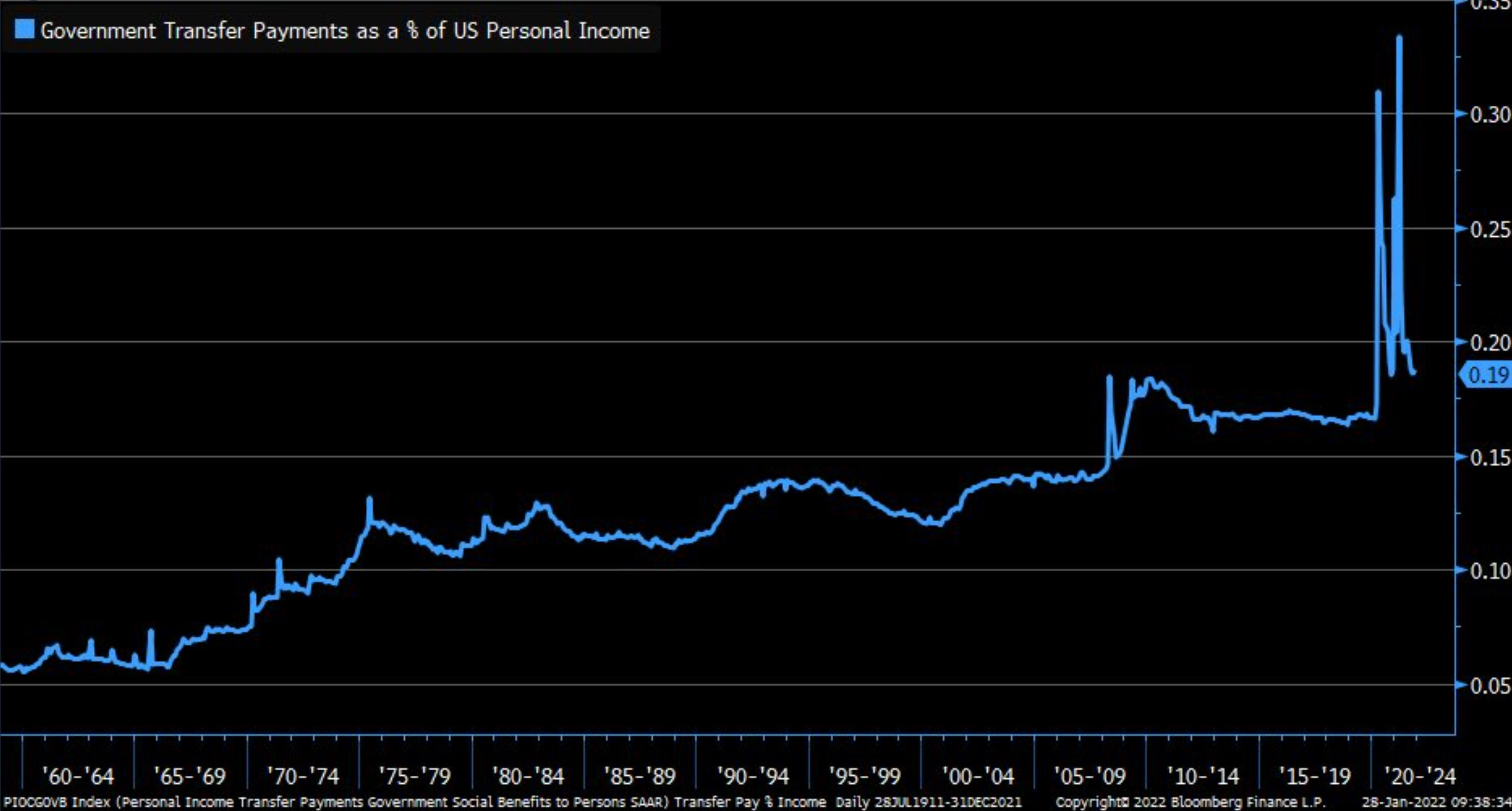

At a time when transfer payments from the pandemic-induced fiscal stimulus is ending:

All while microeconomic actors rationally respond to market economy price signals to try and ramp up production.

So we have a Fed under huge and potentially growing political pressure to ‘fight’ consumer inflation, with tools that don’t really enable them to do so, all while the market economy has already begun to do its ‘job’ for them. Unfortunately, market economies take time to respond, and that response timeline may not align with election cycles.

That chart/model suggests elevated risks of a global recession already exist, and this is before the Fed has raised rates even a single time! Surely investors understand the growing business cycle risks?

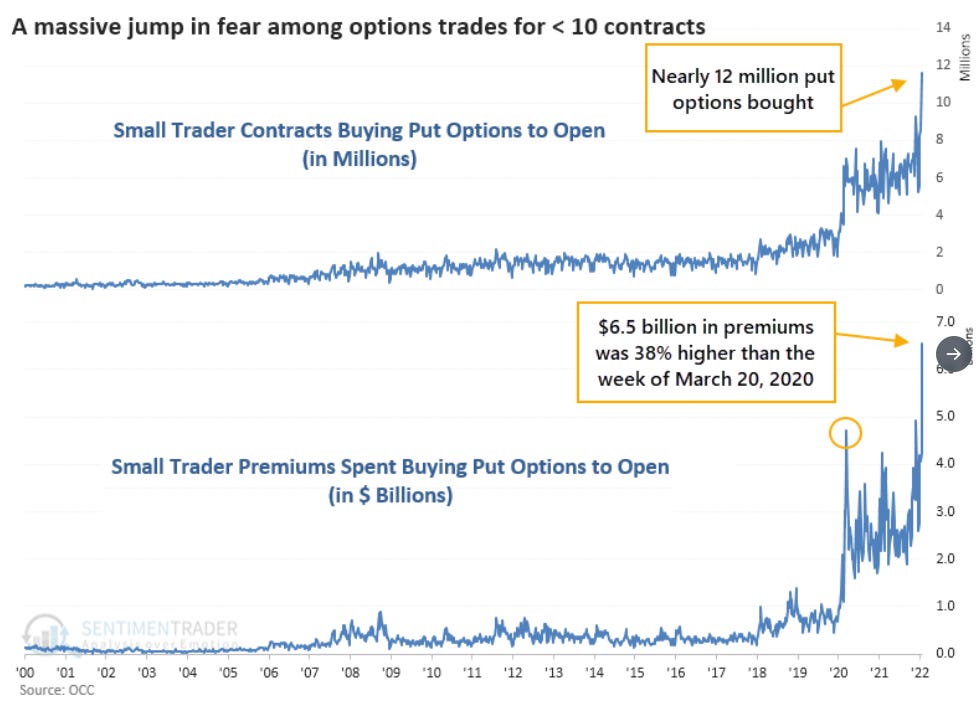

Go back up to the personal income chart and see how much pandemic-induced transfer payments boosted incomes- looky where some of that money seems to have gone with people ‘stuck’ at home, chart courtesy of Sentimentrader. Time to get rich trading options!

Now that everyone’s neighbor is gambling ‘trading’ short-term stock options, why not buy a ton of puts when the market is obviously going lower….it’s easy to get rich!

A sort of manic speculation appears to be unfolding, as people gambling with options are flipping from puts to calls, and probably back again until they collectively blow out their accounts. In the meantime, the big speculators appear to be counting on a ‘Powell’ or Fed put:

While the current market bounce off of last week’s lows may persist for days or even weeks, the cycle backdrop remains intact, IMO. The most explosive rallies typically unfold during bear markets, and we may very well be in the early stages of the ‘next one.’ They serve to lull bulls into renewed complacency, while knee-capping bears with vicious counter-trend moves….certainly not an environment conducive to gambling with short-term options by the masses.

can you provide a link to ECRI’s leading indicators and how you use them?

thank you. So far i have been reading everything you put out here. really interesting and well informed.