Deficit Drama

While Twitter can be a hellscape of trolls and a blackhole of time-wasting, I have been fortunate enough to meet (virtually!) a lot of really smart, experienced, and generous people. When people I have grown to respect layout analyses contrary to my own and approach things from a different perspective, it causes me to revisit and reconsider.

An example of this confluence occurred this past week, as Florian Kronawitter laid out his current thinking in his excellent substack, which echoed various concepts I have been reading and hearing from others for whom I have respect - I encourage all subscribers to The Worked Shoot to read Florian’s analysis and consider subscribing to his substack - even though I am jealous he is far better looking than Kayfabe:

Is the level of the US federal deficit something material enough to prevent a recession, or perhaps ameliorate one enough to make the impacts far less severe than I have been expecting?

After starting this substack and the related Twitter account, it’s generally been referenced as “macro”. That is not the way I think about the Kayfabe Capital analytical framework, as it is not rooted in analytical domains that have historically been attached to macro - i.e. academic macroeconomics, foreign exchange, international trade, interest rate markets, etc.

The Kayfabe framework is a weird blend laid out in this substack’s first post, which has about 1,000 views vs what is currently a subscriber list of about 1,900, so for those who have not yet read that post and watched the linked videos, doing so will provide more context for these weekly ramblings. Much of what is commonly referred to as economics and macro are not germane to the framework, or from my perspective, gets conflated amongst the four Kayfabe pillars.

For example, the mess that is the US Federal Government’s fiscal outlook is a material long-term issue, and one to which I have referred in the past - the CBO’s sans-recession projects being one element.

However, within my process that is distinct from the potential cyclical impacts of what is currently an extremely high deficit for this point in the business and inflation cycles.

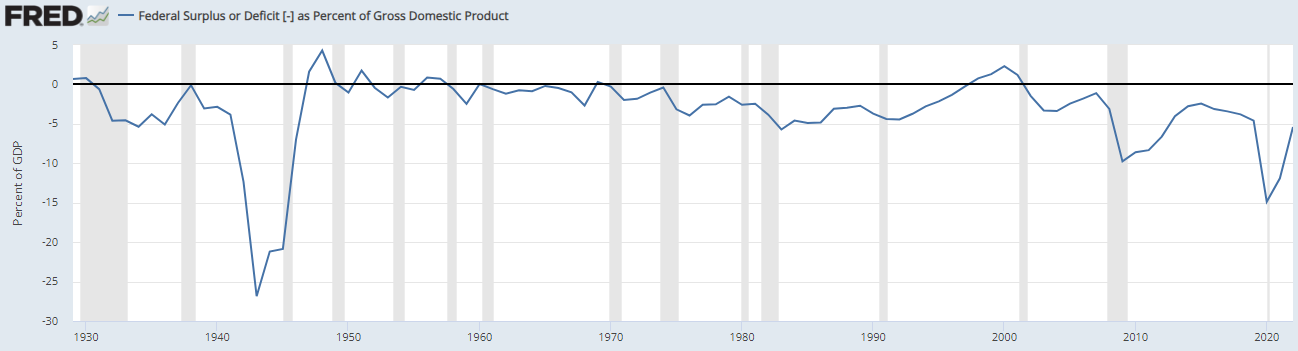

That is a long-term view of the US federal deficit (mostly) relative to Gross Domestic Product (GDP) through 2022. The picture is getting worse this year and at around 8%, as the growth in receipts has fallen with spending still increasing at a faster rate.

Florian lays out a cogent case, and it caused me to go back and look at some prior cycles specifically from the perspective of government spending.

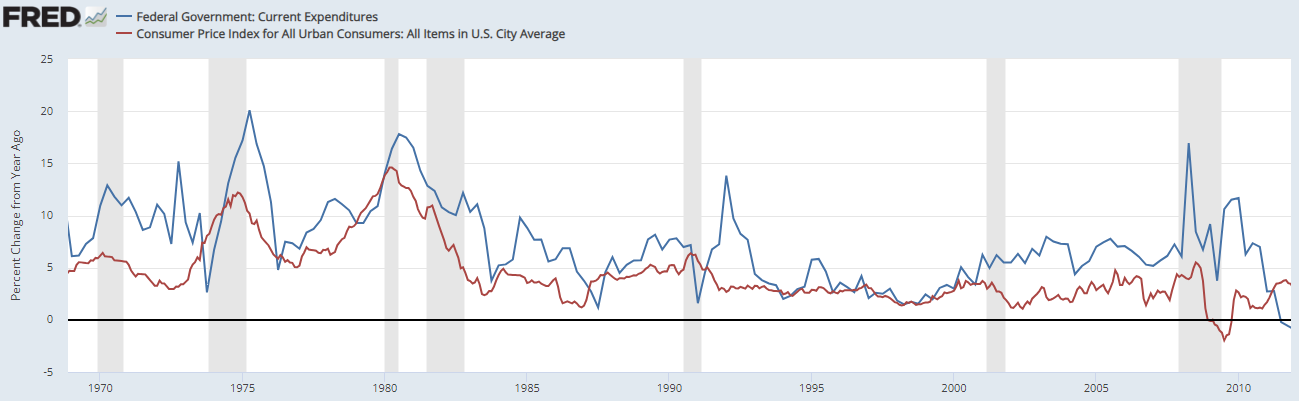

The first image covers the two recessionary cycles of the 1970s, while the second is those of the 2000s, and shows the year-over-year rate of change in the current expenditures component of GDP. The 1970s displayed a significant acceleration in the rate of federal spending, while the 2000s recessions were accompanied by lower levels of spending growth and tax cuts/rebates. Obviously, neither the elevated spending nor the tax reductions were able to abort the recessionary feedback loops that had already begun.

This image shows the year-over-year change in current expenditures with the All Urban CPI since the late 1960s, and we can see the lagged correlation of spending versus inflation cycles. The late 1960s saw a large increase in spending via “guns and butter” policies, but directionally the cyclical relationship persisted. While the 2007-2009 cycle included some higher headline CPI reports, much of that was due to the large spike in energy prices.

While I remain a devout critic of how tortured and misleading contemporary government inflation statistics have become, the following image falls under the category of “all models are bad but some can at times be more useful”:

This image compares what is called Sticky Price CPI with expenditures, where we can see the differences in inflation cycle composition in the 1970-1983 cycles versus subsequent cycles. For example, despite the ramp in energy prices into July 2008, broader gauges of the inflation cycle did not move into a broader cyclical upswing.

In contrast, here is an image of just Sticky Price CPI through the present:

I have excluded expenditures because the wild swings via pandemic-era spending distort images, but we can see from the above that Sticky CPI was comparable to that of the 2001 peak and below that of 1990 prior to the invasion of Ukraine, subsequently eclipsing the level of 1990 peak, and appears to have made a peak for the current cycle. I want to stress once again that I am more concerned analytically with the relative levels and direction rather than the real-world accuracy of the computational methodology.

Does a certain level of fiscal deficit drive consumer price inflation? Do government spending levels or the rate of change (or the rate of change of the rate of change!) appear to have been determinants in past cycles?

Conceptually, these are topics I have broached in the past, if indirectly: particularly in Regime Change and Bizarro Recession.

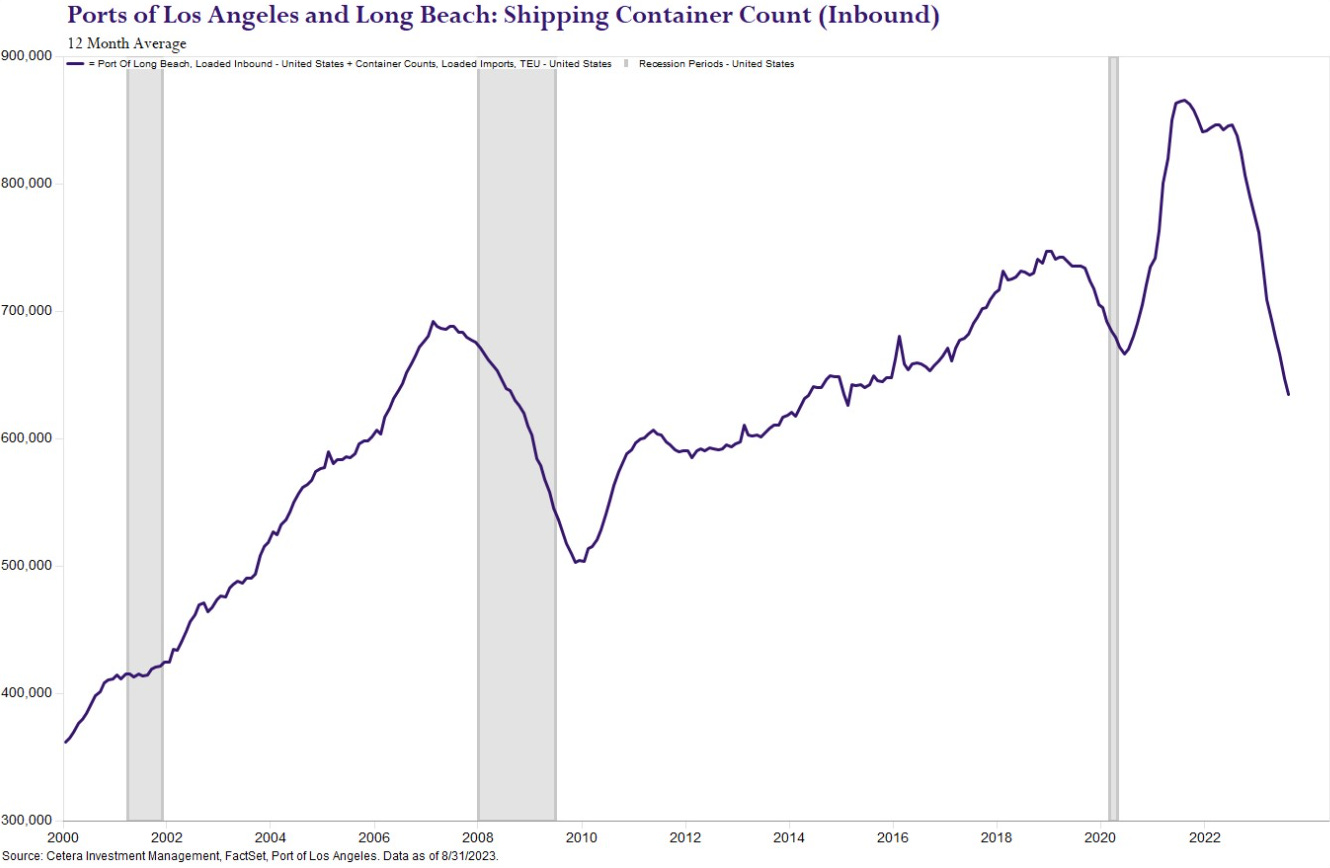

The scenario laid out in Regime Change regarding the risks of prolonged supply chain issues has not played out for now, as the acute issues have been at least partly ameliorated, as reflected in things like shipping volumes through ports falling dramatically:

While the duration of the inflation cycle was likely extended a materially worsened by the aftermath of the invasion of Ukraine, it is an inflation cycle nonetheless.

As laid out in the Regime Change piece, the cyclical upturn in inflation was driven by many factors, including lockdowns, shifting consumer behaviors, massive US government stimulus direct to consumers, and supply chain disruptions. Federal spending and the level of the deficit were certainly an important part of that equation, but only that - part of the equation.

The specific nature of the spending was important (direct-to-consumer bank accounts), and a variable I had not known about at the time, the ridiculous Employee Retention Tax Credit persisted in sending tens of billions on average a month out to largely wealthier taxpayers appears to finally be winding down. With student loan payments just restarting, evidence of stimulus-era savings being used up across a majority of consumers, and the jobs market just recently turning down, will government spending increasing at a decelerating rate be enough to offset recessionary forces?

I do not see it as likely, with the composition of current fiscal spending moving in the wrong direction to stimulate consumer demand. As laid out in last week’s post, I see what I believe to be clear evidence of a recessionary sandpile avalanche picking up velocity and spreading. The “deflation gap” mentioned last year has been getting filled, as reflected in last week’s post via falling sales - i.e. higher prices ‘destroying’ demand.

Once the avalanching process commences, and with it the jobs market and the credit cycle, government spending and/or tax cuts become more muted in stopping the energy unleashed, and that is before contemporary potential issues with falling multipliers and marginal revenue product of debt related to government spending.

Outside of the potential catalysts laid out in Regime Change, there is one other major caveat to my outlook: a balance of payments crisis. I may revisit this in the future, but that is the sort of concern the Kayfabe Capital process has for the US in the back half of the Bizarro Recession scenario or later, which is to say after a severe recession and deflationary shock catalyze political upheaval.

For example, the current move in Federal Reserve Board members towards what I consider quacks (as opposed to incompetent flat earthers) manifests in that ilk replacing Powell. I see countries like Japan, the UK, and even members of the EU more likely to hit a balance of payments-related crisis in which their governments begin to have problems funding accelerating fiscal deficits in their own currencies at viable interest rates.

Great post Sir Kayfabe 👍🏻 Would just note the reasons why deficits rose in the 1970s was to respond to recession. This time it seems in anticipation. Just a thought

Love Florian, but thought his latest post was a hodgepodge of anything bullish to justify the market's YTD strength (e.g., viewing IOBR as economically stimulative is a head scratcher). It's obviously great that several macro bears who missed the strong fiscal component now see it, but to make money in the market you have to skate where the puck is going, not do a post-mortem of what happened.

The US fiscal impulse is going from +6% YoY in June annualized to -3% YoY by year-end. The USD will stay bid as the US deficit remains high and inflation sticky; liquidity continues to be pulled from the market; rate hikes continue to work their way through the economy; SLOOS contracts, etc. Could we get ISM above 50 for a month or two? Sure, but if anything that will really only have a pronounced impact on oil given the massive amount of supply Saudi has taken offline.

Great post as always.