Happy Anniversary!

This week makes it one year of The Worked Shoot, with this having been the first post: Welcome to Kayfabe - whatever the hell that is. I thought the anniversary presented a good time to review a couple of things. First of all, there are now over 1,000 crazy people who have signed up for a business cycle and financial markets-focused newsletter with a Ric Flair and professional wrestling-inspired theme. That is something I am proud of, but also encourage you all to seek immediate professional psychiatric help.

Over the past year, there have been 48 pieces published, and I want to thank all the people who have shared them, as well as the scores of people whose work I source and get inspired by. I try to direct to primary or secondary sources for the graphics I use, so please keep me on my toes if there are any oversights.

For relatively new subscribers, and or those who have not done so before, I strongly recommend revisiting that first piece, and perhaps the year-end summary piece from last December 29th, Where are We in ‘The Process', to have a context for what the hell is going on with this crazy endeavor.

I have kept this letter primarily focused on the cycle-timeframe dynamics unfolding, and refrained from much in the way of investment and portfolio construction ideas. I am considering doing more of that via the new Chat feature Substack recently launched, so leave comments below or hit me up on Twitter if anyone is looking for Ric Flair-inspired ideas. There would be no personal advice - strictly a forum to bounce ideas off one another.

With that housekeeping out of the way- there has obviously been a huge rally in liquid risk markets over the past two months, with reported inflation beginning to come in below expectations. This apparent cyclical peak in inflation was not a surprise to those who value ECRI’s leading indicator-driven process, as their Future Inflation Gauge (FIG) had caused them to forecast over the summer that a cyclical peak would be arriving in the coming months.

For more information on the FIG, inflation cycles, and some history, this half-hour presentation from May 2021 offered tremendous insight- perhaps most importantly how the Fed is unlikely to have suddenly awakened to know what they are doing.

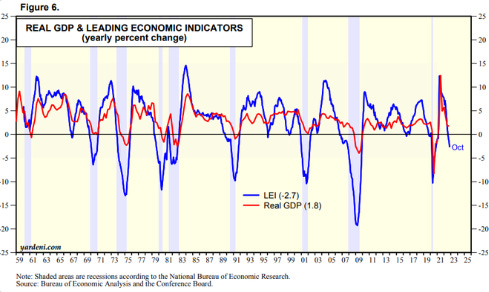

Along with the inflation cycle having likely rolled over, leading economic indicators have as well.

That was a graph of the official LEI, which was originally constructed by ECRI founder, Geoffrey Moore. It is for the US economy, but there are also global cycles, as well as cycles for each country and region. As of their last public statement in October, ECRI’s longest leading indicator for the global business cycle was at levels comparable to where it was just prior to Lehman Brothers’ collapse accelerating the 2007-2009 US recession.

What is notable about these, in my opinion, is the lagged nature of the US economy this cycle. This is atypical of recent historical cycles and could be fueling specific cycle timeframe narratives and denialism. Talk of a soft landing or just a ‘mild’ recession has become pervasive from what I hear/see/read.

Such narratives are not uncommon as business cycles unfold. For example, in 2008 a common narrative at the time was the supposed ‘decoupling’ of the BRIC emerging market economies from what was unfolding in the US and many developed markets.

This was a daily chart of the largest Brazilian stock market ETF (EWZ) over the period, with smiley faces marking major event-driven lows in the major US stock indexes, such as quant blow-up in August 2007, SocGen in January 2008, Bear Stearns in March 2008, etc.

While EWZ declined in sympathy in the short term during those three periods, the general trend higher persisted into an all-time peak in June 2008. Crude oil would peak the next month at over $147 per barrel, and the ‘decoupling’ narrative remained widespread until the post-Lehman panic when EWZ declined about 50% over the subsequent six weeks.

Going back one cycle, the late 1990’s boom was the time of ‘old vs new economy’ companies and stocks, as the hypergrowth expectations for tech/telecom/internet, along with easy monetary policy, fueled a bubble. Many small and micro-cap stocks in old economy businesses, like industrials, materials, etc. were left for dead and traded at very low long-term valuations. This was a chart for the Royce Micro-Cap Trust, a closed-end micro-cap value fund (a decent but not pure proxy due to swings in price relative to NAV- sue me for being lazy):

The smiley faces here represented major inflection points in that cycle, with the LTCM panic lows in autumn 1998, the ‘left for dead’ lows in 1999, then 9/11/2001, followed by the triple bottom for the broader stock markets in July/October 2002 and finally March 2003 at the start of the invasion of Iraq. There was a narrative amongst some at the time about how cheap the stocks were (and they were!), yet they just kept getting cheaper.

Get to the point already! Both of those market segments had real fundamental reasons to be bullish on a multi-year basis, but ignoring the impacts of business cycle dynamics could have resulted in poor timing, lack or loss of patience, risk of panicking with the mob, etc. In just 13 months EWZ would more than triple off its autumn 2008 low, and RMT more than doubled over the subsequent 4+ year bull market.

A peak in the inflation cycle should not be a signal that ‘all is clear’ for investors with a cyclical timeframe, IMO. I have laid out in past Worked Shoots why this cycle could result in Regime Change amidst a potential Bizarro Recession, but those scenarios include a disinflationary, or perhaps even deflationary, shock ushering in a change to underlying structural dynamics of the past two decades. Inflation rolling over, and then potentially surprising at the velocity of its decline, are part of that ‘script.’

Even segments with attractive long-term fundamentals are likely to be babies thrown out with the bath water at some points as a recessionary bear market unfolds. Explosive moves higher like the recent one can be seductive and cause fears of missing out, but Kiss It Patiently. Strategic investors with a cycle timeframe view can utilize these bouts to reposition and fortify in order to better secure the resources and liquidity available to catch your designated babies.

Definitely interested in some Ric Flair inspired discourse and ideas!