Kiss It Patiently

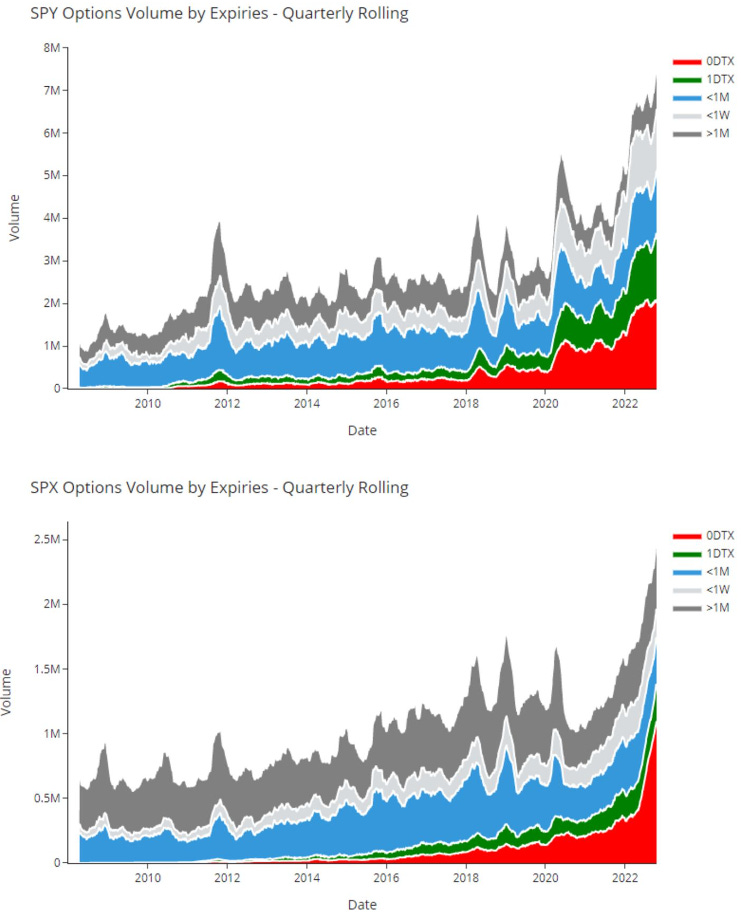

Most of us have become dopamine addicts, and I believe the trend towards the casino-fication of the stock market since the onset of the pandemic is an example of this issue writ large. Courtesy of Jesse Felder:

Unless you are a ‘Fintwit’ obsessive or heavily involved market participant, these graphs may not contain much information without any explantion. The 0 and 1 DTX lines reflect the volume of trading in options contracts that expire on the same day or in 1 day from when they were bought.

In recent years, the explosion in options trading has resulted in Wall Street doing what any good casino does - feed the addiction and make it more widely available. With something like SPY (S&P 500 Index exchange-traded fund) now having expiries every Monday, Wednesday, and Friday, OF EVERY SINGLE WEEK, the stock market has entered a sort of casino hell in which this activity has become a ‘tail wagging the dog’ situation.

I am not going to try and get into the specifics on market structure/plumbing and the various risks this all likely introduces. Rather I started today’s The Worked Shoot with this information in order to contrast it to the actual topic. It can be difficult for people sitting at the Blackjack table for hours on end to maintain perspective on simple things, like whether the sun is out or not! Friday morning’s Nick Timiraos article and the reflexive market response are the latest example of the dopamine degenerates taking action!

It was hard enough to navigate the Fog of Cycles before we all became degenerate dopamine addicts, and now the ability to step back and KISS things is more important than ever. This is a topic I have covered before and will be revisiting regularly and in different ways. Most recently, we took a walk down memory lane via Timeline Tango as a refresher on how long it can take for cycles to unfold and play out. Back in April, What is a Recession, Really? touched upon the business cycle at that time, and that is where we’ll spend the rest of this letter.

Starting late last year, the setup for a business cycle peak and potential reversal into recession became evident within my process. Subsequently, events have unfolded in a fairly typical cyclical fashion, including all of the noise that comes with the Fog of Cycles. The two negative GDP prints in the US for Q1 and Q2 intensified the noise to epic levels, as the reports distracted from the understanding of what a recession actually is- and it is not 2 consecutive negative GDP reports.

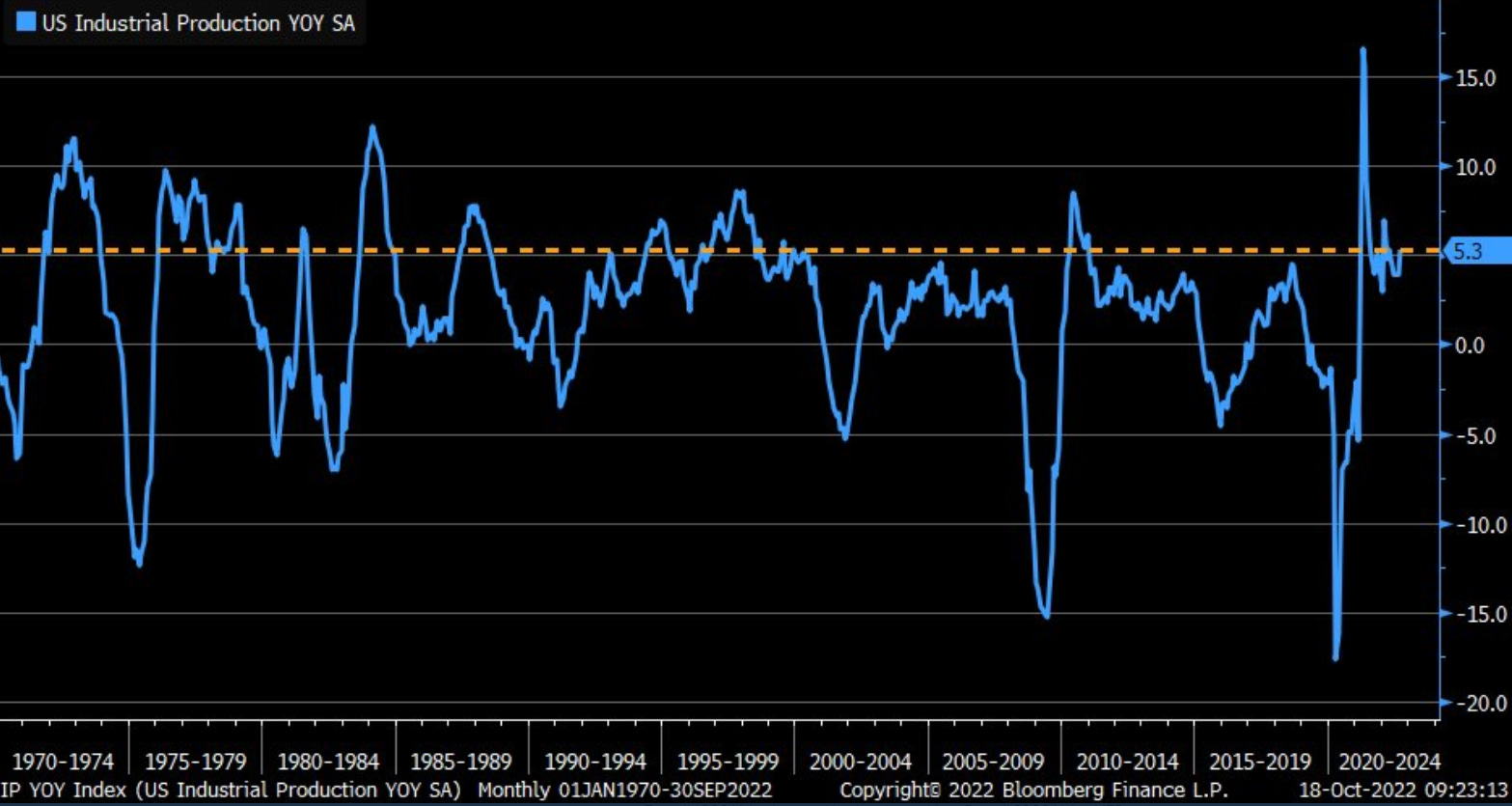

This is vitally important - recessions are when a feedback loop of falling sales, incomes, production, and employment spiral in a contractionary way. Does this chart look like industrial production has been contracting?

I doubt I need to share any employment-related graphs, with unemployment claims and U-3 unemployment reports remaining at or near cycle lows. How can there be a business cycle contraction when two of the four legs of the table have not been in contraction?

It is quite possible that the first Q3 advanced GDP estimate report due to be released next Thursday will be significantly positive. As Q2 GDP in 2008 indicated, positive GDP quarters have been reported and do occur intra-recession, which is why it is so essential to understand what a recession actually is!

All us dopamine addicts want events to transpire yesterday, whether it is the business or inflation cycle. The confluence of lack of patience with ignorance/misunderstanding is quite dangerous for investors attempting to operate on a cyclical timeframe. But the economy and inflation do not care about our addiction. The implications of this are significant. My speculation has been that a US recession has been ‘baked into the cake’ and likely to emerge late in Q3 and/or into Q4. That timeline still seems reasonable to me.

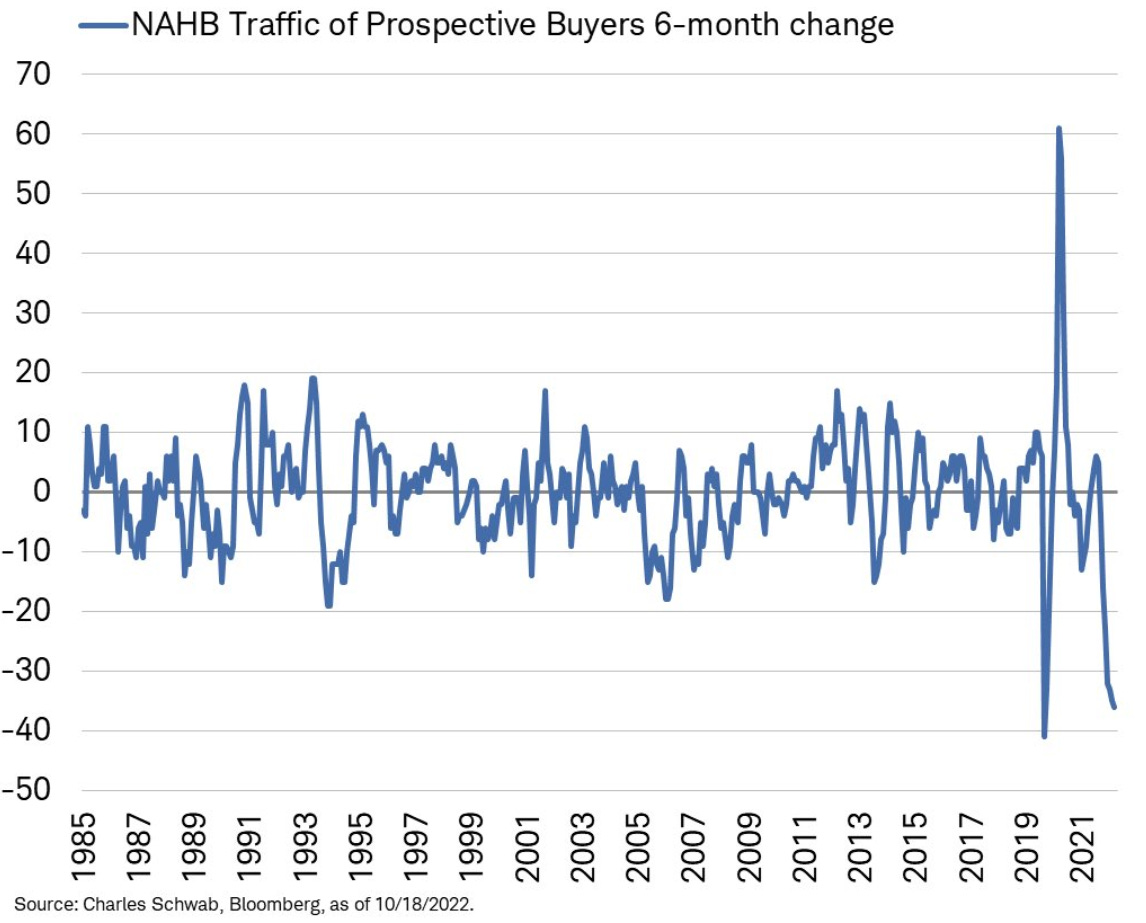

Regardless, the reality of a US recession, and its likely unfolding amidst the first global recession in over 40 years, is still in its infancy. With leading economic sectors like housing just recently tipping over, things like production and employment issues, and the feedback loops into consumer incomes and spending, have not even really started yet. Here are a few housing-related charts courtesy of Liz Anne Sonders’ Twitter feed:

Mortgage rates have moved dramatically higher….which has resulted in:

Mortgage applications dropping sharply……which has coincided with:

Home buying traffic declining precipitously and occurring while:

The supply of new homes has reached levels that preceded the major business cycle contractions of the past sixty years.

It will take time for these cycle-timeframe forces to work their way through the economy, and this is all transpiring with central banks, including the US Federal Reserve, still tightening monetary conditions. There is a reason people reference ‘long and variable lags’ with regard to monetary policy changes, as it takes time for these things to transmit through the hugely complex global economy.

The Conference Board’s Leading Economic Index has just recently gone negative for the US:

So to Kiss It Patiently:

The first global recession in over 40 years is unfolding

The US leg of that recession is likely just beginning or will shortly

Leading indicators are still pointing down with no signs yet of a cycle trough

The vastness of negative feedback loops triggered by business cycle contractions remains dead ahead.

In the absence of leading indicators beginning to stabilize, and given initial conditions and the nature of a synchronized global recession, trying to anticipate the anticipators is foolish and I would argue reckless.

Using lagged data on the remaining resilient parts of the economy and ignoring what leading indicators and initial conditions suggest is also foolish and reckless.

Of course, none of this has anything to do with whether red or black comes up on Friday’s monthly OPEX, or Monday’s, or Wednesday’s, or next Friday’s, or the following Monday’s, etc.

Just please don’t gamble the rent money and be mindful of leading indicators.