What is a Recession, Really?

What is a Recession, Really?

Urban Myths Abound

What is a recession? We all hear and read about ‘recession’ periodically, and how politicians and central bankers try to move heaven and earth to prevent them. But what is a recession?

The National Bureau of Economic Research is the official institution in charge of dating US recessions ex-post, and here is how they define it:

The NBER's traditional definition of a recession is that it is a significant decline in economic activity that is spread across the economy and that lasts more than a few months. The committee's view is that while each of the three criteria—depth, diffusion, and duration—needs to be met individually to some degree, extreme conditions revealed by one criterion may partially offset weaker indications from another.

Note there is not a specific reference to GDP nor that it has to decline for two consecutive quarters, which became the ‘urban myth’ definition popularized starting in the 1970’s. They use the three D’s - Depth, Diffusion, and Duration as part of determining when recessions occur. As a long-time fan of ECRI’s leading indicator-driven analytical approach, I typically think in terms of their 3 P’s - Pronounced, Persistence, and Pervasive.

Recessions are a complex feedback loop across the four legs of the economic stool which comprise the “Diffusion/Pervasive” component: employment, income, production, and sales. Once an unknowable threshold is reached within the business cycle, weakness in these areas feedback into one another and become a self-reinforcing and destructive force.

I will not get into economic theory here, but will simply say that my personal view is that recessions are as natural to economics as winter is to weather. Imagine if we had a bunch of academics injecting and withdrawing things into the atmosphere trying to ‘manage’ the weather to try and eliminate winter.

Much of the economics profession attempts to model things using all sorts of complex statistical models, but they are generally linear and quite poor at forecasting. I would argue they are a classic case of Kayfabe. For example, the fake post-Boskin Commission inflation data permeates throughout things like GDP, productivity, etc. When the basis of measurement of ‘real’ is fake, then the stratified layering of what is real and what is fake is mind-numbingly complex. Now feed all this fake into a stochastic model with some elegant calculus and what do you get? Elegant garbage.

I first did a review of the US economy early in this substack on December 8th last year. Much of that piece remains germane, but with one hugely important complicating factor - what had been the potential early signs of a peaking of the growth rate in inflation was poleaxed by the invasion of Ukraine and subsequent sanctions. ECRI’s future inflation gauge turned back up, though I have not heard or seen any updated public comments as to their specific inflation forecast.

Much of what is now unfolding was reasonably foreseeable using a leading indicator-centric approach, with some simple consideration of initial conditions. For example, here is a chart from John Hussman from his January 14th commentary:

Note how much the pandemic-era government stimulus impacted corporate profit margins. But it was not just corporate profit margins - here is some consumer-related data:

Real disposable income spiked as stimulus checks combined with shifting behavior patterns drove a ton of discretionary money into consumers’ pockets. Some of that fueled the goods-based shift in the supply and demand curve I wrote about last week.

With stimulus payments ending and inflation hammering real incomes (even using the fake inflation data), the growth in consumer credit has jumped. Here is revolving credit specifically:

Here is ECRI’s US Coincident Index they first posted on Twitter most recently on April 21st:

The most recent post for the growth rate of their weekly leading index was March 25th:

All of this is US-centric in addition to the stagflationary environment unfolding in Europe, and continued lockdowns in China. The US economy has been slowing for nearly a year, even as the labor market and corporate profits had remained relatively strong. But cracks in the business cycle have been forming for months, and the US is part of the larger global economy which has its own interconnected reflexivity.

As we go back to the four legs, Amazon just reported year-over-year sales growth below the fake rate of inflation. Lagging production data remains positive but with decelerating growth, and some higher frequency data like freight rates for trucking have dropped significantly in recent weeks. As Lacy Hunt wrote last week, upwards of 170 million people in the US have had their real incomes decline over the past twelve months, again even using fake inflation. Those are two very wobbly legs and one that may have just started to wobble. Surely the 4th leg will save us?

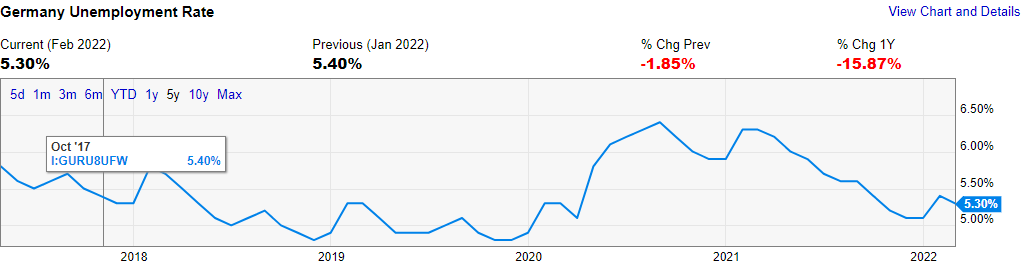

Guess who’s unemployment rate had already bottomed prior to the invasion: