That Pip Nonsense

After last week’s foray into Inflation Idolatry, markets and the broader financial-world discussion appear to remain focused on the topic. The following chart is a decent representation of the inflation ‘echo panic’ that has set in following various economic data reports in January:

It shows inflation expectations for a 2-year term, which have ‘exploded’ higher from just over 2% in mid-January to over 3.26% and poked above where they peaked last year!

Surely, in a world of efficient markets, bond vigilantes, and a myriad of smart people analyzing and navigating bond and interest rate markets, this should be cause for concern that inflation is poised to re-accelerate.

Just how ‘smart’ are markets at forecasting the future of inflation?

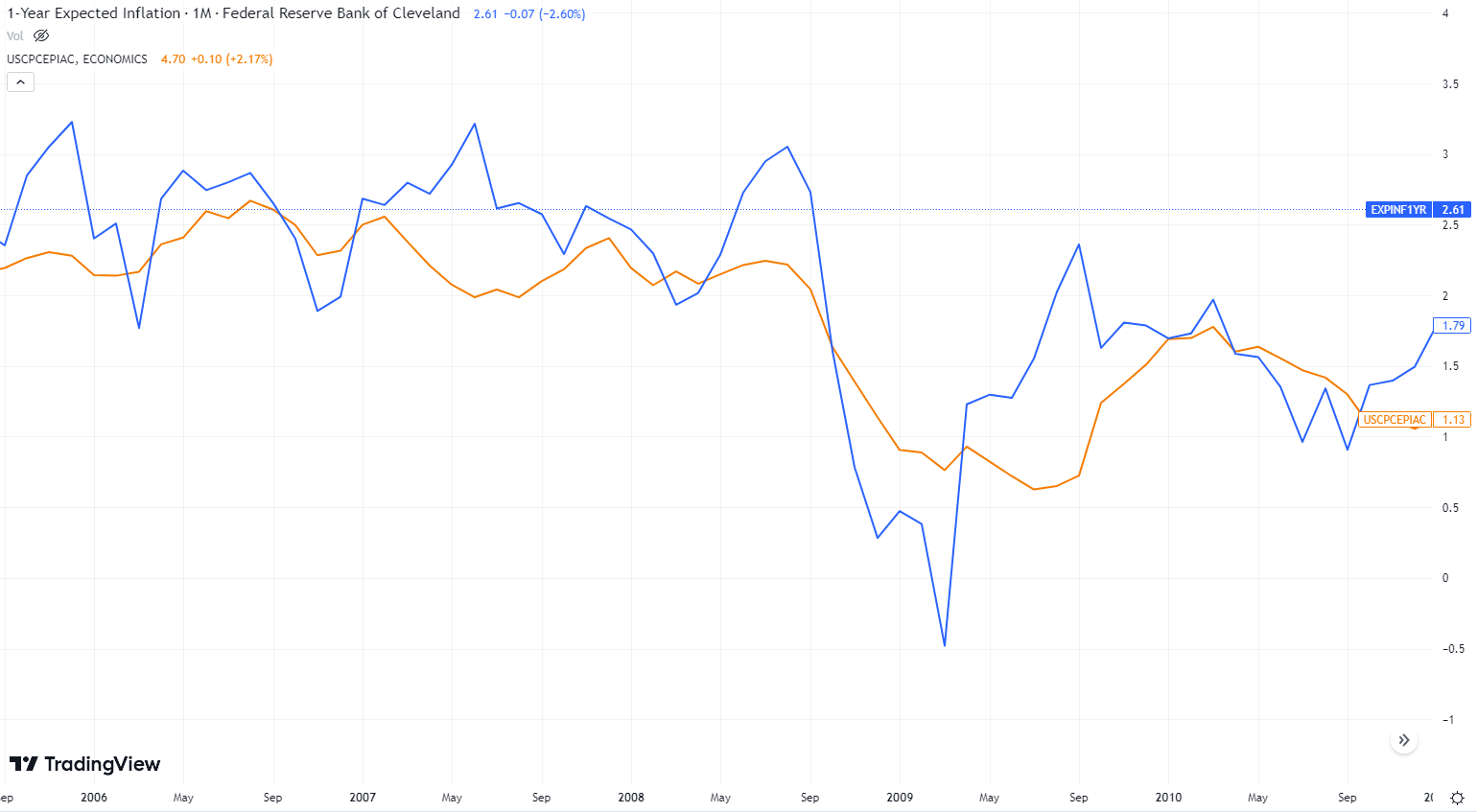

That chart shows 1-year inflation expectations for the period surrounding the GFC along with the Federal Reserve Board’s supposed ‘preferred measure’ of inflation, Core PCE. Just as a refresher, the recession was subsequently dated by NBER to have begun in December 2007, yet Q2 2008 GDP was initially reported as +1.9%, and subsequently revised HIGHER to 2.8%.

Note in the chart above that the 1-year expectations moved sharply higher over that stretch of ‘strong’ economic reports. Oil peaked at over $147 a barrel in July 2008, and the market was STILL pricing in higher inflation well into August, despite being on the precipice of the largest deflationary shock post-Great Depression. Ooopsie!

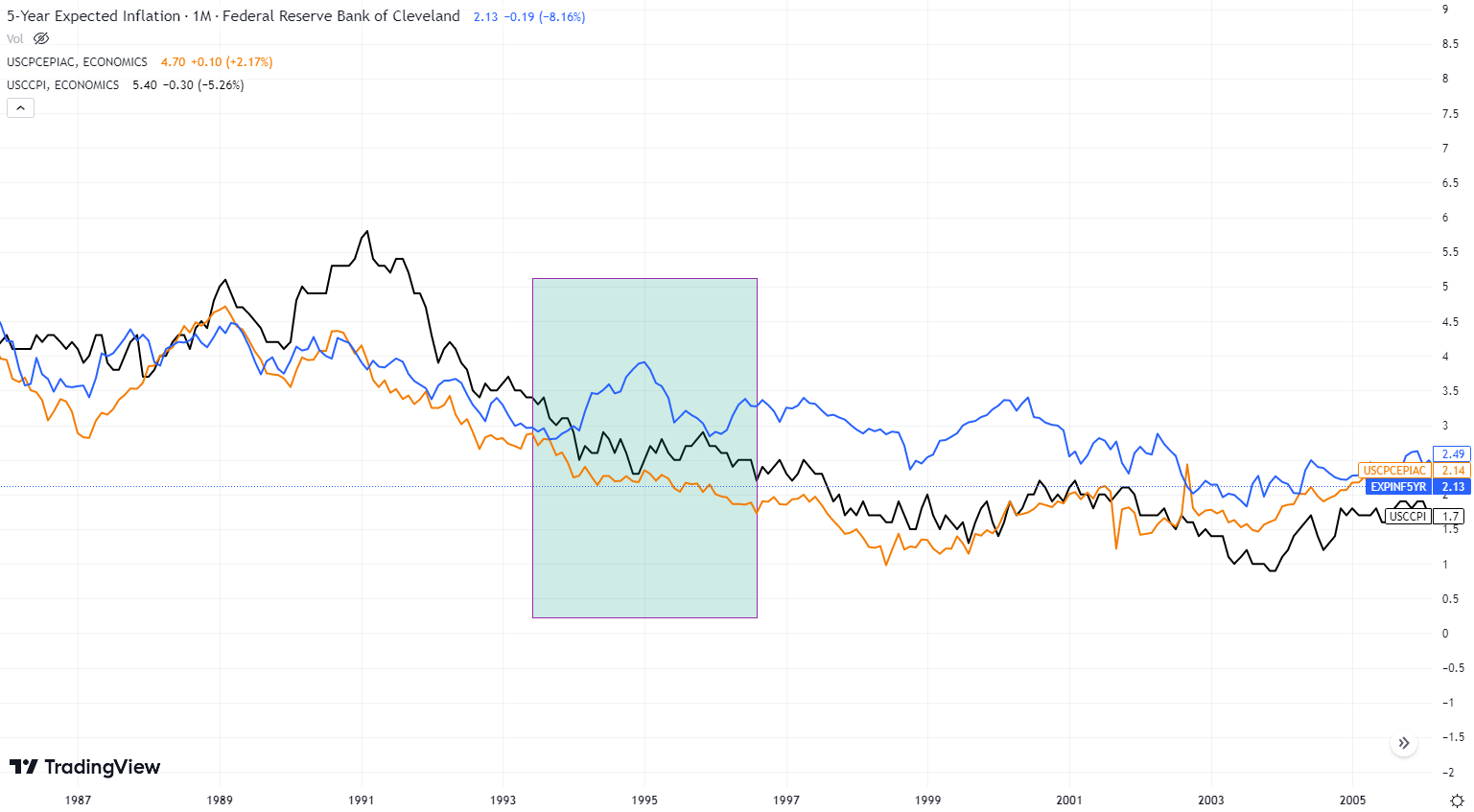

Next, we go back further to the last time the bond vigilantes were taken out to the woodshed prior to the last couple of years:

Here we look at the 5-year inflation expectation, as surely, the markets would be more efficient over longer periods. The 1994-1995 period was fairly unusual, in that former chairman Alan Greenspan used forward-looking leading indicators on the inflation cycle to move proactively to raise rates to try and preempt an inflation cycle upturn. This was a huge surprise to Wall Street and bond markets were decimated, with crises like Orange County and the Tequila Crisis triggered.

The bond market geniuses of the day apparently did not understand Mr. Greenspan’s preemption, as 5-year inflation expectations (blue) remained well above CPI (black) and Core PCE. Ooopsie!

This next chart displays the evolution post-Boskin Commission as Delusion Impacted Reality - note how expectations remained persistently higher than the then-recently ‘enhanced’ inflation data prior to eventually succumbing to the Kayfabe.

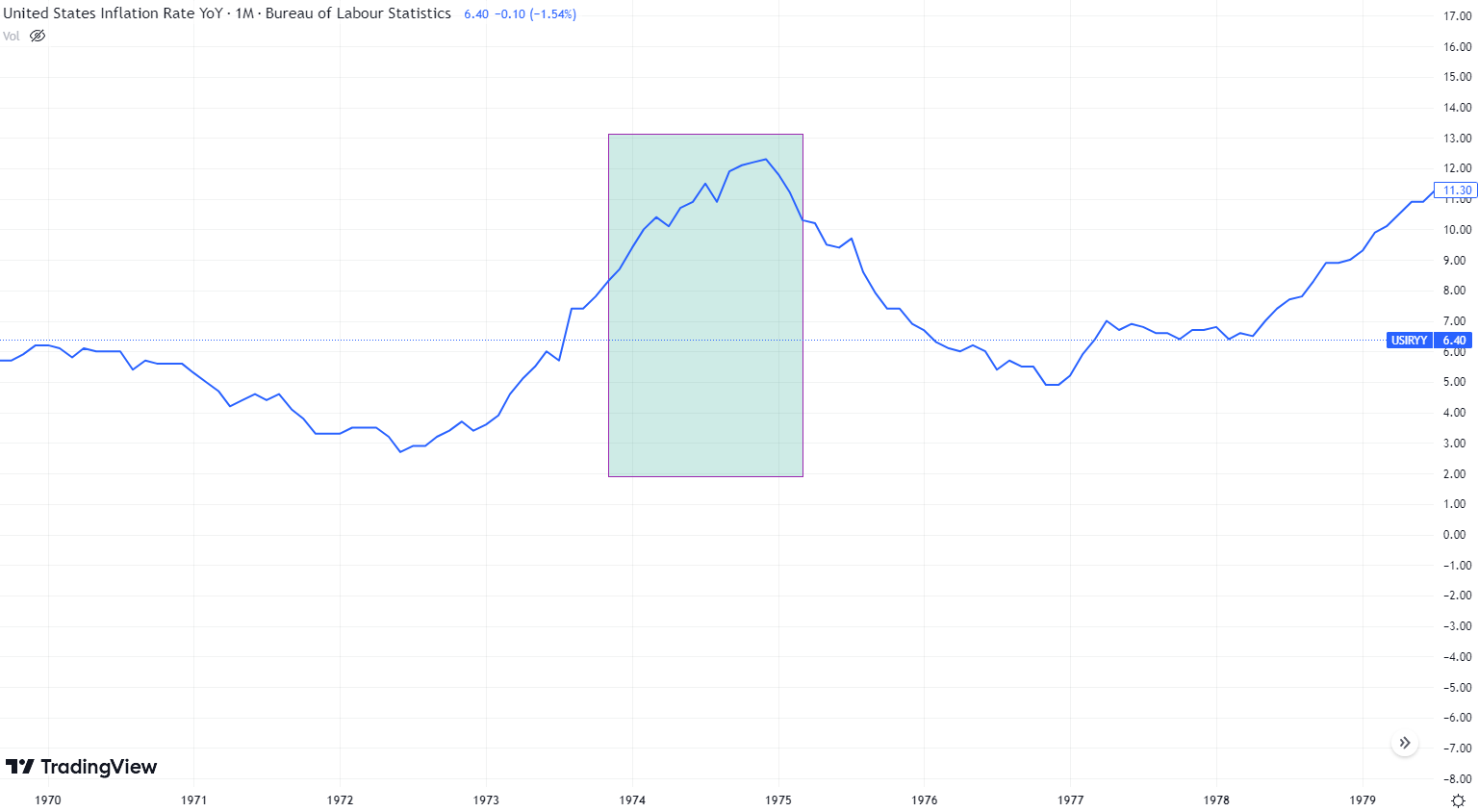

As was painstakingly taught in the 1970s, while certainly linked, business and inflation cycles are discrete. It is not unusual for inflation and related expectations to increase early in a recession as central banks typically ‘pivot,’ but then inflation eventually responds as the lagged/sticky nature of inflation cycles unfold.

Take the November 1973-March 1975 recession, for example:

Amidst the oil embargo of the period, inflation persisted well into the recession and then trended lower for two years into the subsequent recovery.

A notable aspect of the current cycle is the persistent strength in macro-level data for the US consumer and labor market. While various data points are now emerging (auto loan delinquencies) suggesting cracks are emerging in the consumer veneer, the deep reservoir of savings from the pandemic-era stimulus is still being burned through. In addition, many retirees/workers received significant cost of living adjustments (COLA) at the start of 2023. All this has conspired to support nominal consumer spending.

Markets, and apparently the Fed, are pricing in these various elements as if they will be persistent. Discussions of ‘big flip’ and ‘no landing’ have become ubiquitous amongst the Fintwit intelligentsia. It reminds me of all the talk of the supposed ‘decoupling’ of emerging markets in 2008, or in early 2001 when things like ‘the market has never been down X number of months after the Fed has cut this much’ was all the rage.

Markets are now engaged in a reflexive feedback loop with central bankers and driving conditions which, if dealt with similarly, could be analogous to a prior period post-pandemic amidst a European land war: 1920-1921….the often forgotten depression.

While the economic pain would likely be severe, tightening policy into a period of economic weakness was the Fed’s path during that depression, as it acted as a true ‘lender of last resort’ by lending to solvent entities at punitive rates. I could see that path being a reasonable one at present if it were intentional, but I fear we are facing a period of the worst of both worlds. Markets and central bankers are acting ‘tough’ for now, as they appear to be oblivious to the implications of what it means when the water is getting sucked out:

Once the ‘water’ does come rushing back in, I fully expect policymakers to panic and revert back to the same failed policies of the recent past. However, getting from here to there remains riddled with uncertainty amidst the Fog of Cycles.

The Truflation metric for the US has plunged from over 12% last spring and just breached the 5% level:

However, 5% inflation is still pummeling people when it is on top of the prior price increases, and much of this decline has been on the back of recent plummeting prices in the goods sector of the economy. Services are typically far more ‘sticky’ and slow to come down until job losses really ramp up. As mentioned above, the big macro consumer and jobs-related data are likely to persist ‘strongly’ in the near term.

Combined with sticky inflation, the path to an unintentional ‘overtightening’ scenario appears to be unfolding. Narratives about European and US economies re-accelerating may persist well into this spring. A wave lower in financial markets, in both stocks and bonds, may coincide with this persistence, and could even breach the autumn 2022 lows in major indexes.

However, the wall of water is likely to become undeniable sometime in late Q2 or Q3 of 2023, in my opinion. The transition from ‘big flip/no landing’ to a severe recession that triggers the next wave of disinflationary (possibly deflationary) forces is not likely to be like a light switch. While strictly intended as conceptual, this is the sort of path in the US stock market I can envision:

A transition of narratives could include a ‘soft landing’ interlude as inflation data hits significant base effects this summer (i.e. year over year will reference the peak reading from summer 2022), as well as the potential for a ‘goldilocks’ rationale as employment data weaken, but before getting really bad.

This base case pathway will likely be reflected in the Dodo Bird, as a spring decline could offer opportunities to reduce equity hedges, and possibly ramp up exposure to US Treasury duration and gold-related exposure, while expecting to ‘reload’ on hedges into the theoretical summer rally. This is the sort of scenario planning I have found to provide clarity amidst the Fog of Cycles in the past. It is intended as a loose framework rather than a rigid forecast.

Thank you. A thoughtful, realistic scenario. Predictions with a prior history. The "calm before the storm" sort of speak. I hope to be on higher ground when the "water" comes in...