Discover more from The Worked Shoot

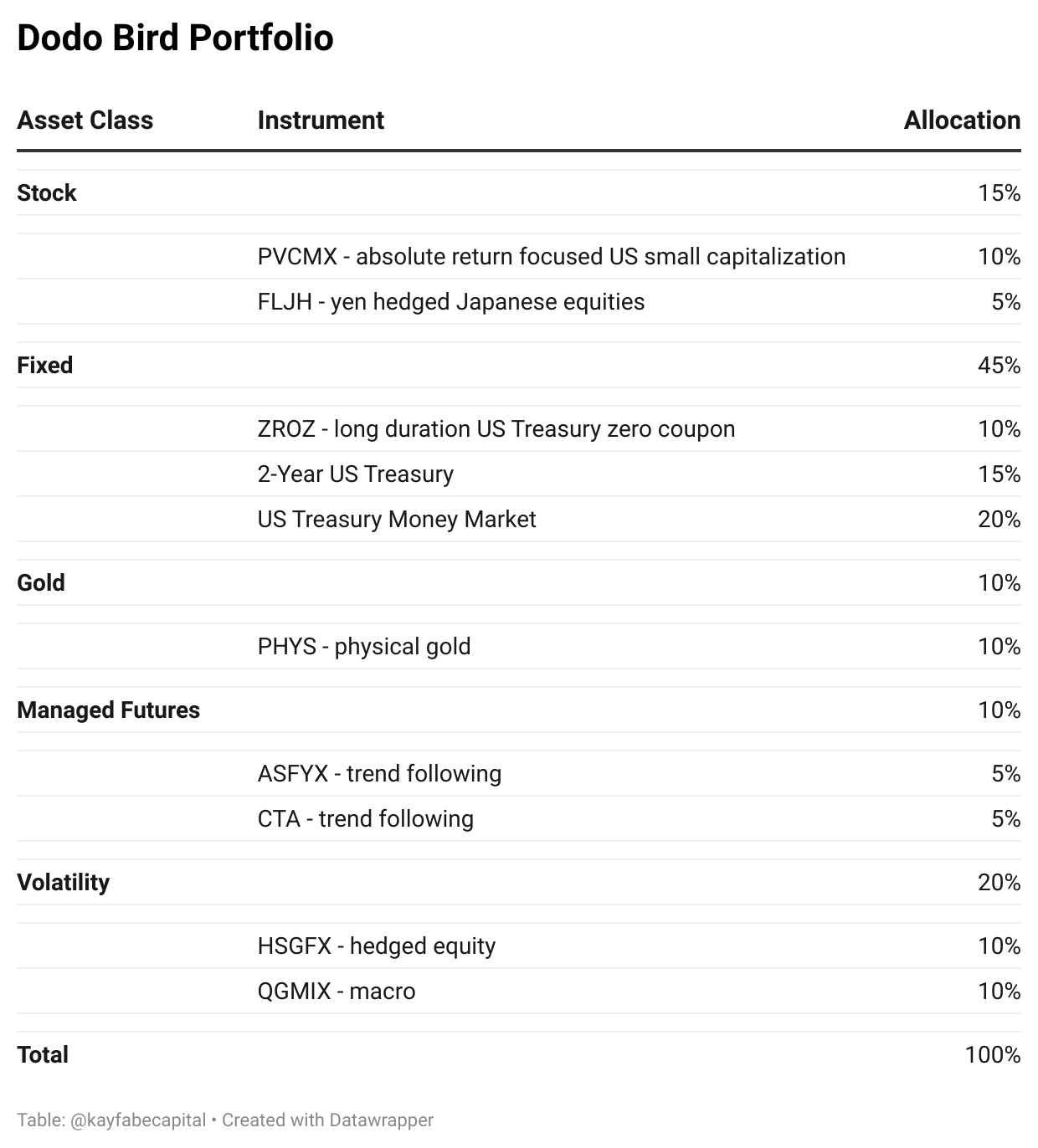

Dodo Bird Portfolio

Kayfabe version of the Hawk and Serpent

The Worked Shoot has been focused primarily on big-picture cyclical trends since inception, with one notable exception. Just under a year ago, I profiled the Palm Valley Capital Investor (PVCMX) fund and its manager, Eric Cinnamond. The fund finished 2022 up just over 3%, in a very challenging year for investors. Today, I am introducing the Dodo Bird Portfolio, which is a Kayfabe Capital ‘model’ inspired by the work of Chris Cole from Artemis Capital. The specific white paper, titled The Allegory of the Hawk and Serpent, can be found here via the Macro Voices podcast. Chris appeared on episode #215 to discuss the concepts in the paper, for those interested.

Before progressing, I just want to say that I do not know or have any relationships with any of these people. They are simply people whose work I have admired over the years.

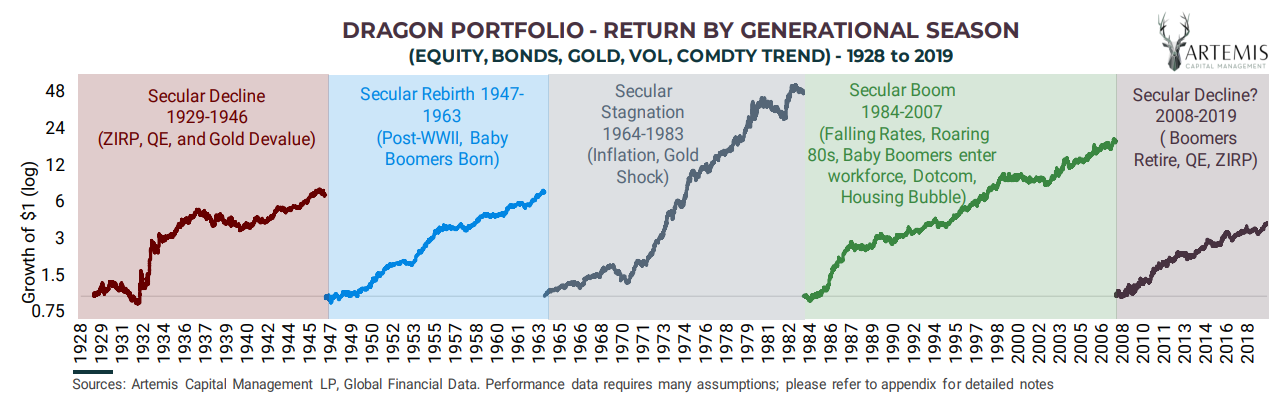

The white paper presents a heterodox, and I believe, compelling case, as to how the conventional strategic asset allocation framework is flawed- both culturally and analytically. It then proceeds to propose an alternative, with the concept of preserving and growing wealth over 100 years central: the Dragon Portfolio.

To summarize, it has 20% each in stocks, bonds, gold, commodity trend following, and volatility. The idea is to have components of the portfolio resilient to various secular market forces and to rebalance over time. Here is a graphic from the piece showing the back-tested performance through various secular periods:

Last year was another year in which the resilience of this portfolio construction persisted. To keep things simple here were some related returns for 2022, which was the worst in modern times for a traditional 60/40 US stock/bond portfolio mix:

S&P 500 -19%

Long-term US Treasuries -30%

Gold flat

Commodity Trend +22%

Volatility ? (Kayfabe Capital proxies were up 17% and 29%)

The volatility component is a tricky one and will be addressed in the Dodo Bird Portfolio. Realized volatility was quite high for the year, but navigating what became a tricky year in the pricing of implied volatility meant performance was highly dispersed for those active in the space. Regardless, we can see the elements of real diversification, rather than the kayfabe variety deployed by most of ‘Wall Street’ - i.e. strategic asset allocation.

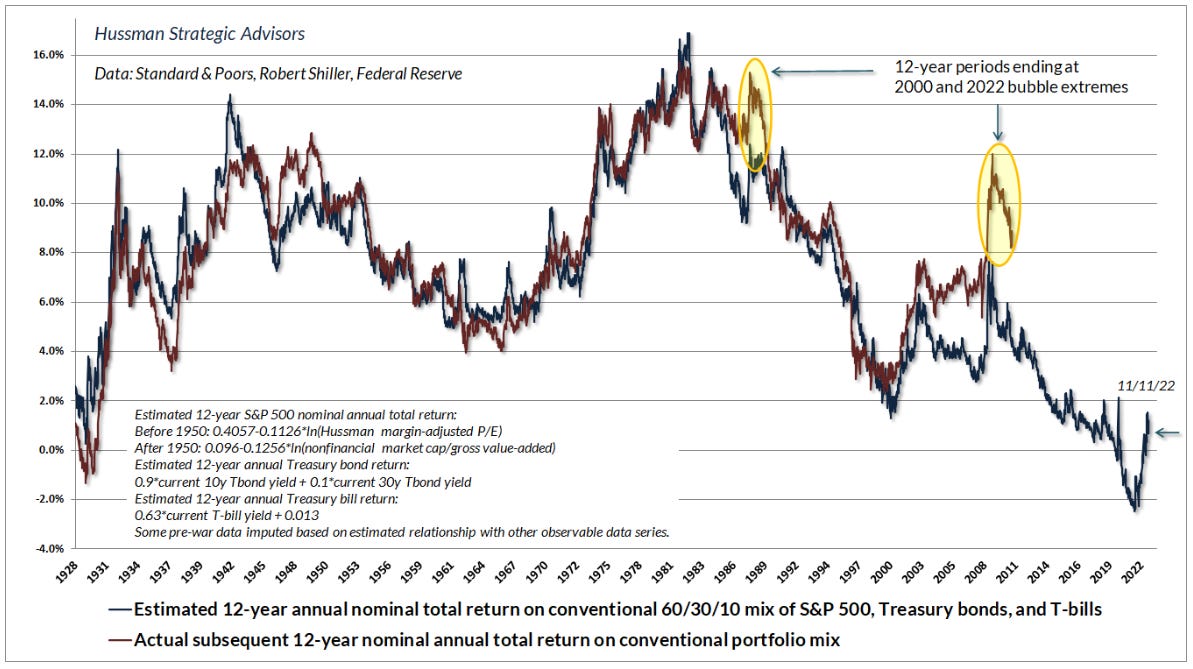

I like to track the performance of the now-ubiquitous target date strategies that dominate defined contribution plans. For example, Vanguard Target Retirement 2035, so let’s say someone around 50 years of age who aspires to retire in 2035, experienced nearly a 17% decline in 2022. What are the prospects for such ‘60/40’ - style strategies going forward?

That graphic and model come courtesy of John Hussman, whose commentaries are always worth reading, in my opinion. We can see his proxy for 60/40 and historical performance versus his valuation-centric forecasting model suggests very poor nominal returns over the coming years. The so-called ‘fiduciary’ industry is ignoring this reality - they are kayfabe fiduciaries, IMO. I believe the reality is they, with some exceptions, are generally in the business of asset gathering and retention.

With prospective returns in mainstream strategies potentially so poor, what are the ‘50-year-olds’ trying to plan for retirement to do? For young people, many of these topics are a distraction, as investing in one’s career, living below one’s means, and systematically saving/investing, are the most important issues. But for people with assets already accumulated and with far less than 100 years over which to plan, I introduce the Dodo.

The Dodo Bird model portfolio is intended to be conceptual and not financial advice for any individual. I am sharing this for educational purposes and to try and introduce some of these concepts. It does not take important factors such as taxes, etc. into account. Please seek out a non-fake professional if you require assistance. In a real portfolio, I would not ‘snap’ the exposure as this one will be.

This is obviously oriented towards a US-domiciled investor, but the concepts can be re-oriented globally. The idea is to blend the Kayfabe Capital analytical framework with the Dragon Portfolio concept for the individual investor. I have tweaked the exposure to the ‘asset class’ groups based on where the Kayfabe Capital framework place markets within the cyclical forecast.

For example, the concern over one more deflationary impulse this year has the gold position at half the 20% Dragon Portfolio weight and allocated to the less volatile physical metal. At some point, that could be increased and metals miner equities added.

The broader priority is to try and preserve portfolio value and liquidity to be in a strong position to reallocate as markets become less liquid and risk asset values continue to re-price materially lower.

Stocks - underweight and extremely conservative

Fixed - very overweight and tilted heavily towards US Treasuries and liquidity

Gold - underweight and more conservative

Managed Futures - underweight to be more conservative

Volatility - equal weight

The last two categories are likely the least familiar for many individual investors. Managed futures are typically quantitatively-centric models which trade commodity, foreign exchange, and financial futures contracts. The underweight is due to my concerns over the potential for the coming months to be very volatile and choppy - i.e. the kind of volatility that could make trend following more challenging.

I have been skeptical of volatility as its own asset class or strategy and have been particularly concerned about how it would scale as assets dedicated to it increased. In addition, I am not aware of any viable instruments available to individual investors that may be suitable, so the proxies I have chosen for ‘Volatility’ are alternative strategies that typically perform well during periods of increased financial market volatility: hedge equity and global macro.

Now some explanation on each of the positions with links to more information:

Stocks:

Palm Valley Capital Investor - referenced earlier in this letter. Please refer to the link above.

Franklin and Templeton FTSE Japan Hedged - Japanese equities have been in a 3-decade bear market. This position offers some equity market exposure but is specific to a potential macro scenario. The Japanese government and central bank have been engaged in what I consider very dangerous and unsustainable fiscal and monetary policies. Essentially, they are many years ahead of similar problems emerging in the United States.

Japan recently began to try and intervene and peg both its currency and bond markets. This is not sustainable even over the intermediate term, and my thesis is that the yen will ultimately revalue much lower. The massive fiscal deficits over the past decades have resulted in a debt burden relative to their economy which makes higher interest rates untenable. A default will have to occur either technically or via the yen. The Franklin ETF attempts to hedge its exposure to the yen, and equity markets in countries that experience tend to move sharply higher in local currency terms. In theory, it should perform very well in such a scenario. The ETF is relatively small and does not trade a significant volume, but individual investors should be fine executing via limit orders. Wisdom Tree offers a more liquid alternative, symbol DXJ.

Fixed:

PIMCO 25+ Year Zero Coupon US Treasury - this is an expression of the concept laid out in the Dragon Portfolio, which is to offer a portfolio component that should perform very well in a disinflationary/deflationary scenario. Its price dropped by over 60% from its 2020 all-time high to the recent low in October last year. In such a scenario, I could see this ETF appreciating by 30%+, which would offer material portfolio diversification.

2-Year US Treasury and Money Market - price stability and liquidity are the name of the game here, with important lessons from 2008 kept in mind. Stretching for yield in the allocation sleeve is intended to offer stability and liquidity can be a big mistake. Keep it simple stupid is my credo, including the selection of money market vehicles.

Gold:

Sprott Physical Gold Trust - another example of keeping it simple stupid. An alternative is the closed-end fund version, symbol CEF, which during periods of market dislocations could possibly trade at a material discount to net asset value, and could present an opportunity should that occur. Precious metals miners remain very cheap on most long-term valuation metrics, and I would not argue with those who decide to allocate some to that market segment. My preference for the Dodo Bird portfolio is to remain patient and observe how they trade during a potential upcoming broad market decline, which I suspect will occur amidst more acute concerns about recession. I expect this allocation to increase in the coming months.

Managed Futures:

AlphaSimplex Managed Futures and Simplify Managed Futures - I am no expert on quantitative strategies or trend following. The former is a mutual fund structure, while the latter is a new ETF. Both are managed by firms with long histories and track records deploying these strategies. Spreading amongst similarly profiled managers seems reasonable to me. Trend following had an excellent year overall in 2022, as there were persistent trends in various bond, currency, and commodity markets. Again, with a more conservative overall posture in the Dodo Bird, and concerns of 2023 possibly being a choppier year, has me underweight for now, but will be revisited regularly.

Volatility:

Hussman Strategic Growth - after an extended and well-publicized period of poor performance, I believe this hedged equity strategy offers quality diversification benefits. The fund is managed by the same ‘Hussman’ as referenced above. Effectively, it is an active equity portfolio strategy, that focuses on high-quality cash flow businesses, with an active options/hedging overlay. Given the convexity of options, this can provide ‘volatility-like’ portfolio exposure during periods of increased market volatility. For example, the fund was up about 25% during the COVID panic period in Q1 2020, and 10% during the far less volatile decline in early 2022 surrounding the start of the war in Ukraine. Such positions are not ‘set and forget,’ and as with all active strategies, I will monitor for potential drift and/or shifts in Dodo priorities.

AQR Macro Opportunities - best of breed in the global macro space are typically in the hedge fund world or now have their own family offices - think Soros and Druckenmiller. I like the relatively small size of this fund and AQR has a long history of running alternative strategies in the mutual fund structure. Like the Managed Futures allocation, similarly profiled funds would be reasonable. As a complement to trend following, global macro can perform well in choppier market environments and historically has done well in periods surrounding recessionary bear markets.

My plan is to price the portfolio as of the close of trading on January 6, 2023, and will update periodically. For convenience, I will probably use an ETF proxy for the 2-year US Treasury position, so please excuse my laziness in advance.

Please do your own due diligence and use this as it is intended - an exercise to provoke thought and question conventional ‘wisdom.’ Depending upon interest, the Dodo Bird Portfolio may be the topic for which I open up the subscriber chat function, though I have to admit that my initial solicitation for interest in that idea was underwhelming - may confirm my suspicion that this is a very smart subscriber base!

*Added post-initial publishing - I encourage and may share with express permission any crowd-sourced ideas sent to me for the Dodo Bird allocation weights

Subscribe to The Worked Shoot

Analyzing the madness of crowds with help from Ric Flair and Benoit Mandelbrot

I'm having too much fun trading to lock in an long-term portfolio, but I do own some of the assets mentioned.

Very interesting piece - reminds me a bit of the Jakob Fugger portfolio: 25 % real estate, 25% gold, 25% bonds, 25% stocks.

https://www.fidelity.com.sg/articles/analysis-and-research/2017-09-06-breaking-with-tradition-a-history-of-multi-asset-investing-1548036438537

Be interesting to see how the managed futures component plays out - I dont pretend to be an expert, but the tax benefits of an ETF vs MF could make a difference in that space.