Analyzing Ackbar

A sardonic stratagem?

This week appears as if it may end up being a horrifying Kayfabe Captial singularity, as a significant number of prior topics covered in The Worked Shoot have simultaneously become acutely germane. A quick review prior to jumping into analyzing Admiral Ackbar:

News of Iran and Saudi Arabia re-establishing diplomatic relations echoes Bye Bye Brenton Jr.? from last August, as a potential long march forward towards a US dollar alternative appears to be progressing

News of potential bank runs and regulators closing the nation’s 16th largest bank in California echoes Schrodinger’s Bak from last July, as the ‘dead cat’ of unrealized balance sheet impairment at US banks was known to some, but the box appears to have been opened to all this week, with associated cascading ‘sandpiles’ avalanching

The presumed Federal Reserve “mouthpiece” in the financial press referenced the drop off in survey responses for government data ahead of Friday’s huge non-farm payroll/jobs report and echoes When Delusion Impacts Reality from December 2021, when the line between what is fake and what is real becomes cloudy - it’s kayfabe, baby

Developments at various US banks follow the zinc blowup last year, UK pension blowup in September, FTX collapse, and the alleged fraud at Adani companies in India are starting to echo a recessionary bear market Timeline Tango

There are more, but let’s get to today’s topic:

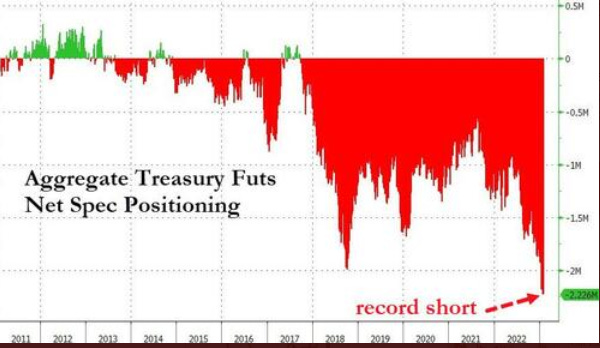

In last week’s That Pip Nonsense, I laid out a base case pathway for the rest of 2023, with an expectation of risk markets selling off this spring due to a renewed growth/inflation scare fueling higher interest rates. The news involving some US banks this week appears to have started a short covering rally driving rates lower short term, as speculators’ exposure to betting on higher rates/short bonds reached an extreme level:

The news of regulators closing Silicon Valley Bank, and rumors of other potentially distressed banks, may be triggering all sorts of PTSD from the GFC period via recency and confirmation biases, but the current backdrop is much different. I’ve argued we are in the midst of a sort of 1930/1973 Frankenstein setup, so can we add a little S&L crisis as the sprinkle on top?

None of these historical analogs are the same, but similar to saying that a zebra is like a horse with stripes, they offer some framework for understanding….while obviously being different.

For those unaware or who do not remember, the S&L crisis took place mostly in the 1980s and carried over into the early 1990s. A combination of higher interest rates to combat inflation (sound familiar?!) and a regulatory regime ill-equipped to handle the higher rates left many Savings and Loan financial institutions with impaired business models. Effectively, their difficulty and cost of attracting deposits relative to the assets/loans they could own were not economical.

What are policymakers apt to do after poorly thought-out regulations create a problem? Make things worse, of course! S&L’s were allowed to increase the risks they took and the rest, as they say, is history.

The crisis overlapped with a boom in commercial real estate and associated lending, and along with what would become the introduction and subsequent implosion of the junk bond market. It was the era that inspired the creation of this guy:

The inflation crisis of the past two years has driven the Federal Reserve to raise short-term interest rates to around 5%. Banks have been slow to raise the rates they pay on deposits, and customers have been moving their money out. This is now causing increased costs at banks in order to retain and attract deposits. In addition, the era of financial repression post-GFC resulted in banks moving out the risk curve in order to preserve profitability. Part of that was to extend duration on some of their higher quality bond holdings, such as US Treasuries, as well as holding mortgage-backed securities.

The explosion higher in interest rates over the past year has left a significant amount of those holdings at significant mark-to-market losses - i.e. the price of a 1.5% 10-year Treasury purchased in late 2021 is now trading as if the bond has a current yield around 3.7%, with a price decline of roughly 15%. Banks are able to account for “held to maturity” positions at full value, but a significant decline in customer deposits can, in theory, create potential liquidity and/or capital issues. If/when held to maturity positions are sold, a loss could be realized and compound problems.

The credit cycle has not experienced a recessionary purging since the GFC, as the 2020 shock was cushioned via various government programs. There are 13+ years of ‘dry tinder’ laying on the floor of the credit forest, including in commercial real estate. I covered some of these issues and how they were a reverse echo of the 1920s in A Young Powell last December.

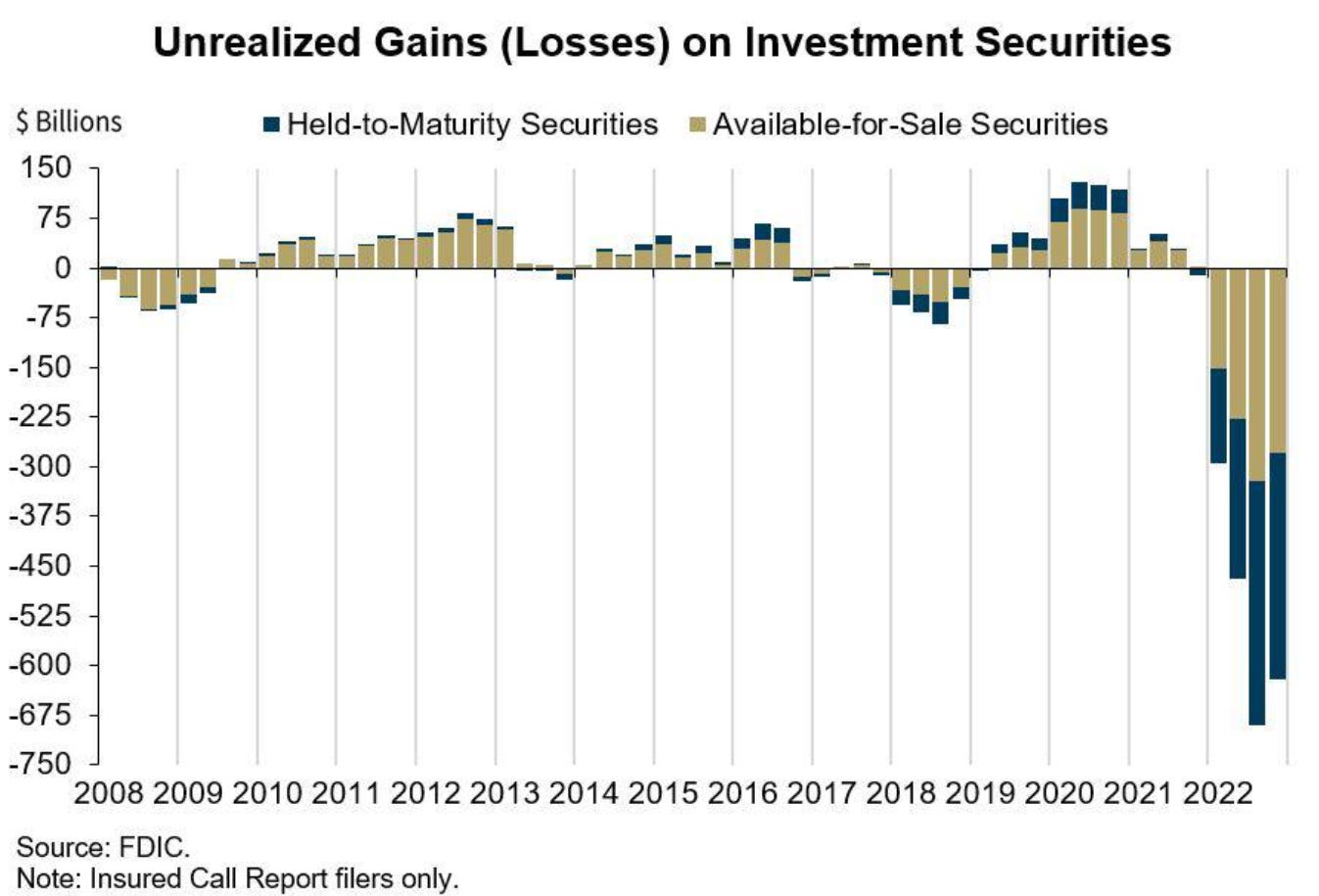

With inflation rates still high relative to the Federal Reserve’s stated target and various recent economic reports having been received as “hot,” what if there are more banks that ‘float to the surface’ in the coming weeks? System-wide bank reserves are robust and the Fed and regulators surely stand at the ready to protect insured depositors, but what of bank balance sheets and their appetite to extend credit? Here are unrealized losses on US bank securities portfolios:

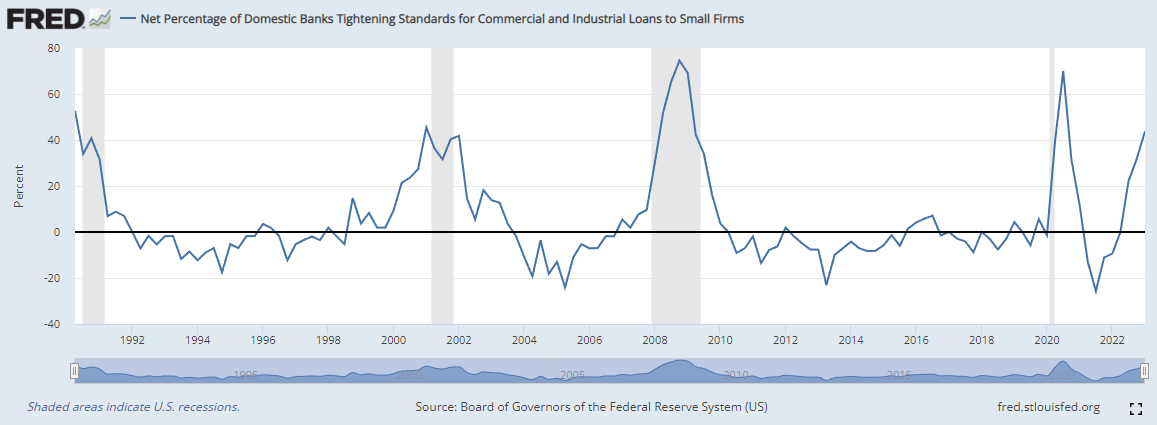

The net percentage of US banks tightening lending standards to small companies:

Given the loss of credibility over how badly the Fed managed the inflation crisis, could they ‘pivot’ with core inflation remaining at double their long-stated target?

Would they be willing to take the associated reputational risk, as well as potentially de-anchor long-term inflation by aggressively reversing policy without the Too Big to Fail brethren under direct threat?

With Main Street-targeted federal programs like food and healthcare assistance from the pandemic period ending this spring, can they afford to be seen ‘bailing out the banks’ yet again?

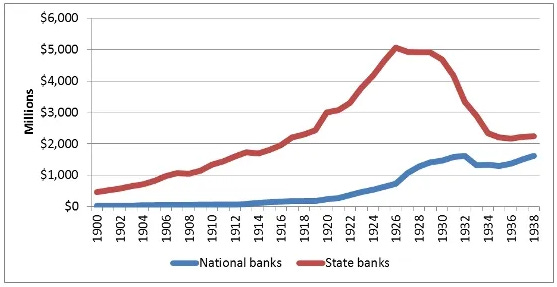

The Fed may be trapped, and the US may be looking at a LOT of small and medium-sized banks that may need capital, with additional failures likely in the pipeline. Surely, the big banks would not use a crisis to their benefit?! From the A Young Powell piece - real estate lending a century ago:

Nice work on Ackbar. I wonder if you might lend some insight/clarity to the last two days. I am trying to understand the psychology of the bond market here. This is a brief detour away from a higher for longer 10 year yields due to the “fear-flight to safety” trade prompting people to rush-in and buy bonds due to echos of a GFC like contagion around the corner? People are thinking the FED will pause or pivot sooner given SVB and the other “dry tinder” ready to burn that you write so well about? The S&P is gonna get hammered like you suspect and bonds are doing what they should be doing... My way of thinking is inflation will not relent near term and the FED will stay higher for longer and rates rise. How can you buy longer duration here with the inflation boogie-man lurking in the closet?