Bad Mother******

I have had very few original thoughts in my life, and cannot remember any that were not nonsensical. If there is any skill hiding in the dark recesses of my brain, it may have been the ability to identify good ideas from smart people and incorporate them into my Borg-like analytical framework. They tend to be bad mother*******, in a good way, with the fortitude to be heterodox and zig when others are zagging.

I came across Eric Basmajian on Twitter this year, and his analysis has been a welcome addition. As an example, today’s The Worked Shoot is built off one of his ideas.

One of the key elements driving concerns amongst central bankers and many ‘macro bears’ focused upon the high inflation of the current cycle has been the perceived risk that higher wages will create a ‘wage-price spiral.’ Basmajian has written about his view that the cyclical sequence has actually been money-price-wage.

He shared this chart via Twitter on October 16th:

This was from Lacy Hunt’s Q2 2022 quarterly letter where he discussed Other Deposit Liabilities, which was the monetary metric in Basmajian’s chart:

In 2020/21, other deposit liabilities (ODL), which comprises about 80% of M2, and is the energizing component of M2, increased by an average of 19.6% (Chart 1). The difference between M2 and ODL is currency in circulation and money market mutual funds held by individual investors. Examination of the critical monetary relationships indicate that ODL is, at a minimum, of equal importance as M2 and most likely of even greater value in terms of cyclical economic analysis.

For those interested in the more technical aspects of these metrics, read Hunt and Basmajian’s work. Even if not, I strongly encourage following anyway!

The chart shows the epic amount of money poured into the economy in response to the pandemic - i.e. the money part of the cycle.

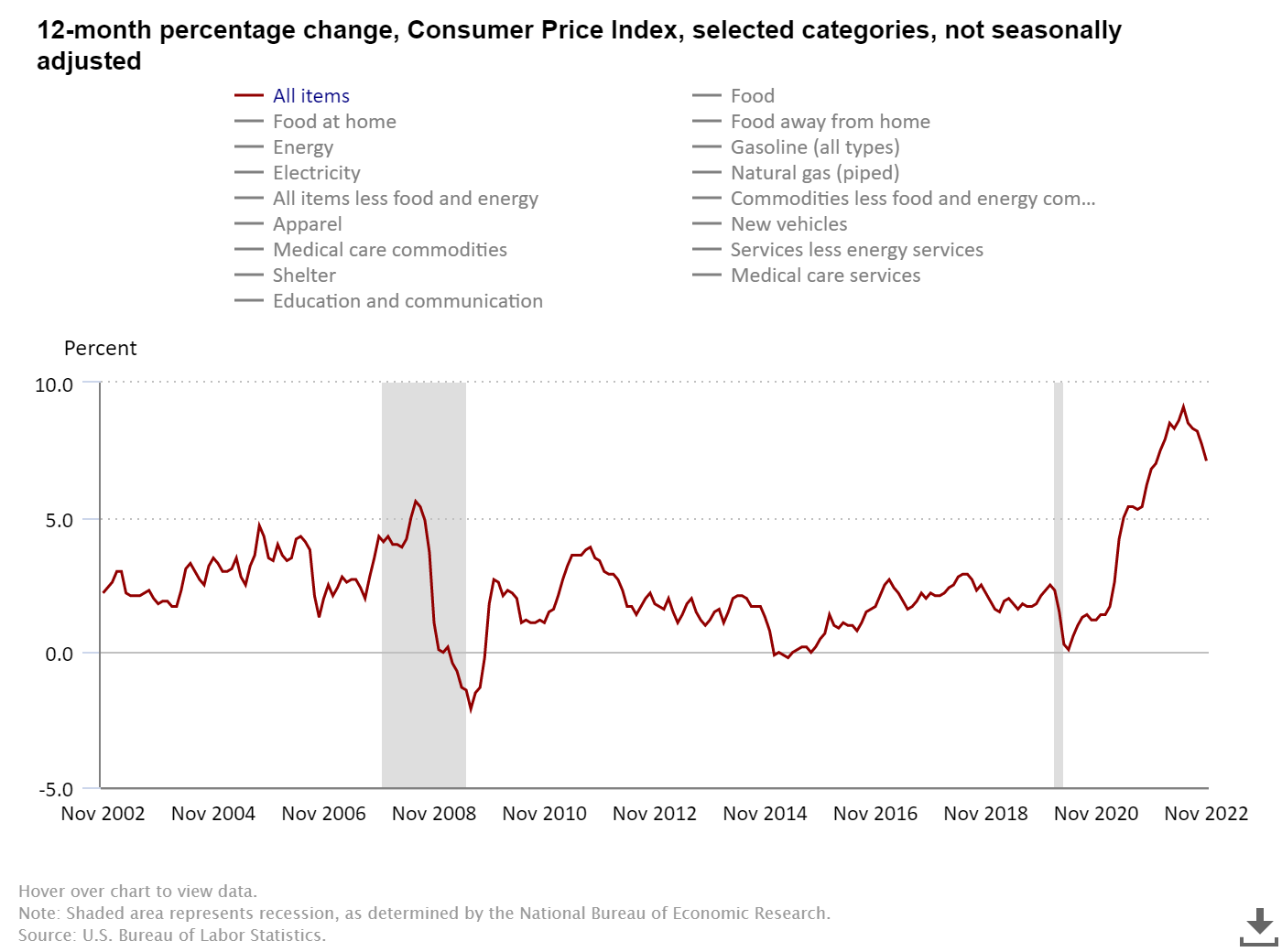

This was the price part of the cycle:

Or at least that has been the official phoney baloney CPI reported by the government - for more on that, read When Delusion Impacts Reality from last year.

What came next in the cycle? Wages!

The chart showed the nominal year-over-year rate of change in wages, with the impact of the massive stimulus standing out in 2020/2021. Following the swings in growth rate as stimulus checks came and went, a more persistent upswing took hold. However, the nominal increases have been well below even the phoney baloney rate of inflation. The result has been a huge contraction in real incomes and a cost of living crisis for 150+ million Americans.

As I add this to the Kayfabe Borg, evidence of increased cyclical volatility appears to be emergent. Readers can revisit the Schrodinger’s Bak piece from July where the complex systems element of the Kayfabe Borg was reviewed. Today I’ll throw in some pendulum analogies, as the oscillation of this money-price-wage cycle has had huge amplitude. We can see this across macro-focused charts. Here was retail sales after this week’s report, courtesy of Ms. Sonders:

With cycle volatility having been ‘unleashed’ by the pandemic and subsequent policy responses, the path to renormalization could be an extended one, in my opinion. The record level of synchronized stimulus from central banks in 2020-2021 has now oscillated with comparable amplitude into record tightening.

Central bankers are operating off flawed models using flawed lagging data to try and centrally plan the future. Money growth has gone negative, prices are likely to follow, and then wages. However, it requires people to Kiss It Patiently in the era of dopamine short-termism. Central banks are tightening with record pervasiveness into the first global recession in over forty years with the amplitude of their policy error looking more and more like it will match those made in 2020-2021. As the pendulum swings back, some Frankenstein version of a Young Powell could emerge.

You have to appreciate Ronald Reagan's famous mantra that government is the problem and then nominating Alan Greenspan. This began an ever expansionary intrusion into markets made notorious by the "Don't Fight The Fed" guiding star principle. It's only getting worse. The pandemic hastened this. Maybe by end of the decade we will all be singing 'Don't Cry For Me Argentina"😭

I have to say that I really enjoy your writing. Your writing helps me make sense of the complex, interactive pieces of financial markets. Like Yuval Harari helps explain key drivers of human behavior, Kayfabe helps explain key drivers of market behavior. I believe markets are a three-body problem, you can't predict the future with precision but you can make reasonable guesses based on Borg Brain models which inform where to look for emerging trends. Thank you for your work!