Seminal Singularity

I have had some writing fatigue recently, as the evolution of life developments has conspired with increasing realized market volatility to raise my excuse-making threshold for not sitting down and typing. The return this week is to say something relatively simple: I believe we have reached the Kayfabe Capital Singularity.

This Substack was started immediately prior to a huge cyclical turn in global financial markets early in 2022. Remember the good ole days, when the Federal Reserve was still locked near zero with the Fed Funds Rate and doing QE while Core PCE was still accelerating and nearly tripling their supposed 2% target rate? Good times!

The timing of the launch of The Worked Shoot was not happenstance - my goal was to try and offer a variant perception of what I expected to be a historically difficult cycle to navigate. For those who have not been reading since the beginning, or explored the archive, I encourage you to do so. These ramblings make even less sense without the full context offered by the prior pieces.

Much of what we all consume on a daily basis from Wall Street, media, Fintwit, and the government is kayfabe - fake intertwined with real. This has been a journey to try and offer my framework for attempting to analyze and delineate, while also trying to keep market cycles separate, though obviously also intertwined, with business and inflation cycles. Perhaps the most important non-consensus pillar within that framework is viewing pretty much everything through the lens of complex adaptive systems and self-organizing criticality.

The topic was first broached here in Where are We in ‘The Process’? at the end of 2021, and revisited in some depth in Schrodinger’s Bak in July of 2022. Those offer vital context for how I have written about and analyzed the business, inflation, and market cycles over the nearly two years here.

I describe the present as a potential “Singularity” because many of the issues I have written about, including the timeline of this cycle, are manifesting in an acute fashion, IMO.

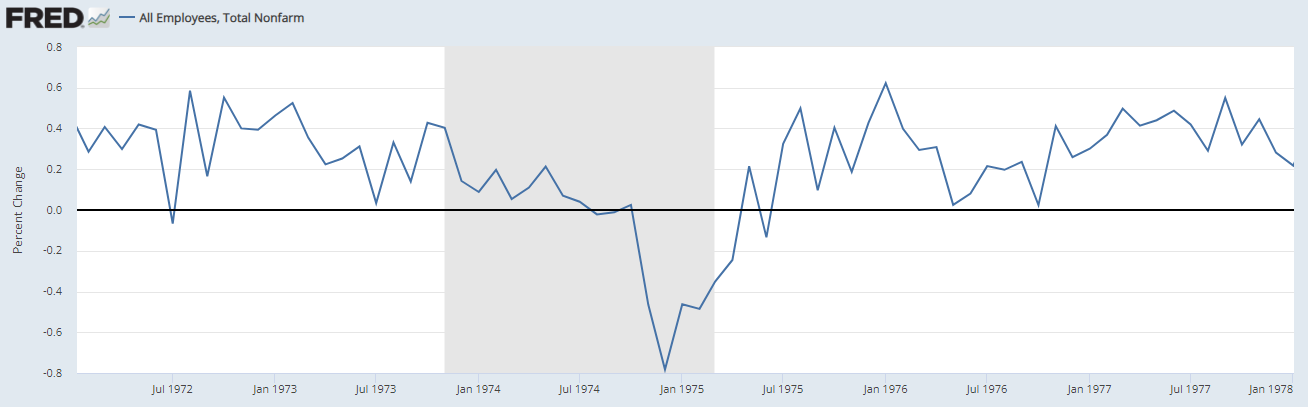

My labeling of this cycle as a Frankenstein of 1930 and 1974 is central to the ‘story,’ as we are now seeing clear evidence, even within the flawed coincident government data, of the labor market rolling over materially. The seemingly delayed timeline of this occurring, similar to 1974, has been THE major leg propping up the ‘cyclical table.’

With clear evidence of a business cycle sandpile avalanche having begun in Q4 2022, the labor market finally capitulating amidst the grains of economic sand crumbling around it will unleash the vicious part of the business cycle. Once again returning to the 1973-1975 cycle:

The labor market ‘sh*t’ did not hit the fan that cycle until a YEAR AFTER the NBER eventually dated the recession to have begun in November 1973. Of course, that market cycle did not have an options market/leverage mania and was not a golden age of fraud - topics also covered here at various times….though the Nifty Fifty does echo a bit with the Magnificent 7.

Those elements are more aligned with the other half of the Frankenstein, as financial market leverage via investment trusts and margin borrowing reached epic levels in 1929 and into 1930. The last gasps of that leverage bubble occurred as margin requirements were raised materially, which should echo with recent government officials talking about the leverage in the US Treasury market via the basis trade, increased margin on MBS bonds, and the comment period the SEC opened in May this year on the burgeoning insanity of unlimited intraday leverage available to some firms via the options markets.

What could happen to the orgy of intraday market fun and games that have become brazenly obvious since the introduction of daily expiries just over a year ago, when/if unlimited intraday leverage ends?

In addition to these US-specific elements, another hugely important aspect of this potential singularity is the global nature of the cycle, which through the lens of SOC, means the size of the sandpile and related hypercriticality increases latent risks exponentially. With Europe/UK coincident economic data already quite poor, even prior to their labor market acceleration phases, China once again decelerating, and Japan struggling with its late-stage sovereign insanity experiment, the landscape for the US to renormalize amidst a global sandpile avalanche is daunting.

However, as has been the case in many prior cycles, financial markets have an ingenious way of suckering people into doubting what in hindsight becomes glaringly obvious - see If Hitler couldn’t do it, then… and Timeline Tango for examples.

The irony in all of this is that after 2 years of a vicious bear market in US Treasury Bonds, with real rates having moved well into positive territory, and gold remaining relatively range-bound, markets are now at least offering avenues for diversification that most are either rejecting and/or ignoring while remaining focused upon playing the greater fool game of the anointed Megacap tech stocks and/or gambling via the options market within the increasingly rigged intraday casino.

Governments and central banks will very likely shift policy directions as the gravity of the current business cycle risks become glaringly self-evident, and the details of those actions will be very important as they unfold, as explored in Regime Change in April 2022 and Bizarro Recession in July 2022.

But the time for preparedness has ended, in my opinion. The recent explosive rally in risk assets over the past two weeks appears to me to be yet another one of Mr. Market’s dastardly tricks, just as the kayfabe singularity is unleashed. As stated on Twitter in August, evidence of the next downward phase of the bear market emerged within the Kayfabe Capital analytical framework, with interludes such as mid-September and now mid-November offering opportunities for people willing and able to get conservative to do so. Contrary to most of the past 15 years, there are alternatives.

The QQQ ice bath lady beating us all in her qqq's. Nice work.

Ken

Thank you Ken - the options mania is making the 1999 IPO mania look like a wuss!