Mack Attack

If you are bored and dorky enough to be reading this Substack, you’ve likely heard of Milton Friedman and possibly even Geoffrey Moore. The former needs no introduction, while the latter was the “father” of leading indicators and founded Economic Cycle Research Institute (ECRI) in 1996. ECRI is part of the Circle of Trust at Kayfabe Capital, and today’s focus is upon someone whom you likely have not heard: Ruth Mack.

Mack was a contemporary of the two men and also worked as an economist at NBER. I first came across her work almost twenty years ago when she was referenced in ECRI’s book, Beating the Business Cycle, in which they referenced her analysis of the shoe industry in the 1950s, including the cycle dynamics through the leather and hide supply chains. From page 41 of ECRI’s book:

During a period of growth, the shoe manufacturer anticipates rising demand and begins to build an inventory of shoes to avoid being caught short. If the economy slows, for whatever reason, some concerned consumers will react by postponing shoe purchases. Even if this results only in a slower increase in shoe demand-one that fall short of expectations-the shoe manufacturer will be stuck with excess shoe inventory. In addition, earlier orders to the leather producers continue to be filled, and the shoe manufacturer’s inventory of leather also piles up.

As those inventories pile up, the ripple effects down the supply chain become significant. From page 42:

Mack found that slower growth in shoe sales resulted not in a slow easing of demand for leather, but in a sudden plunge. In turn, the leather producers, stuck with an even larger excess of inventories than the shoe manufacturers, turn to their suppliers of hides and cut orders still more sharply. The hides producers experience an even more precipitous drop in demand than the leather makers do. Mack’s study demonstrated how the cycle becomes more pronounced the farther you get from the consumer, cascading in ever-larger cycles the closer you come to the earliest supplier in the chain.

Notable that a seminal work of research in the field of economics conducted by a woman would subsequently become known as the “Bullwhip Effect.” That phrase was coined by Proctor & Gamble about 40 years after Mack’s work - note all of the citations in this linked piece, with none referencing Mack. HIStory, indeed.

The phenomenon will heretofore be called the “Mack Attack” here at Kayfabe Capital, in honor of one of the infinite number of women whose prodigious contributions to history have gone uncredited and/or overlooked.

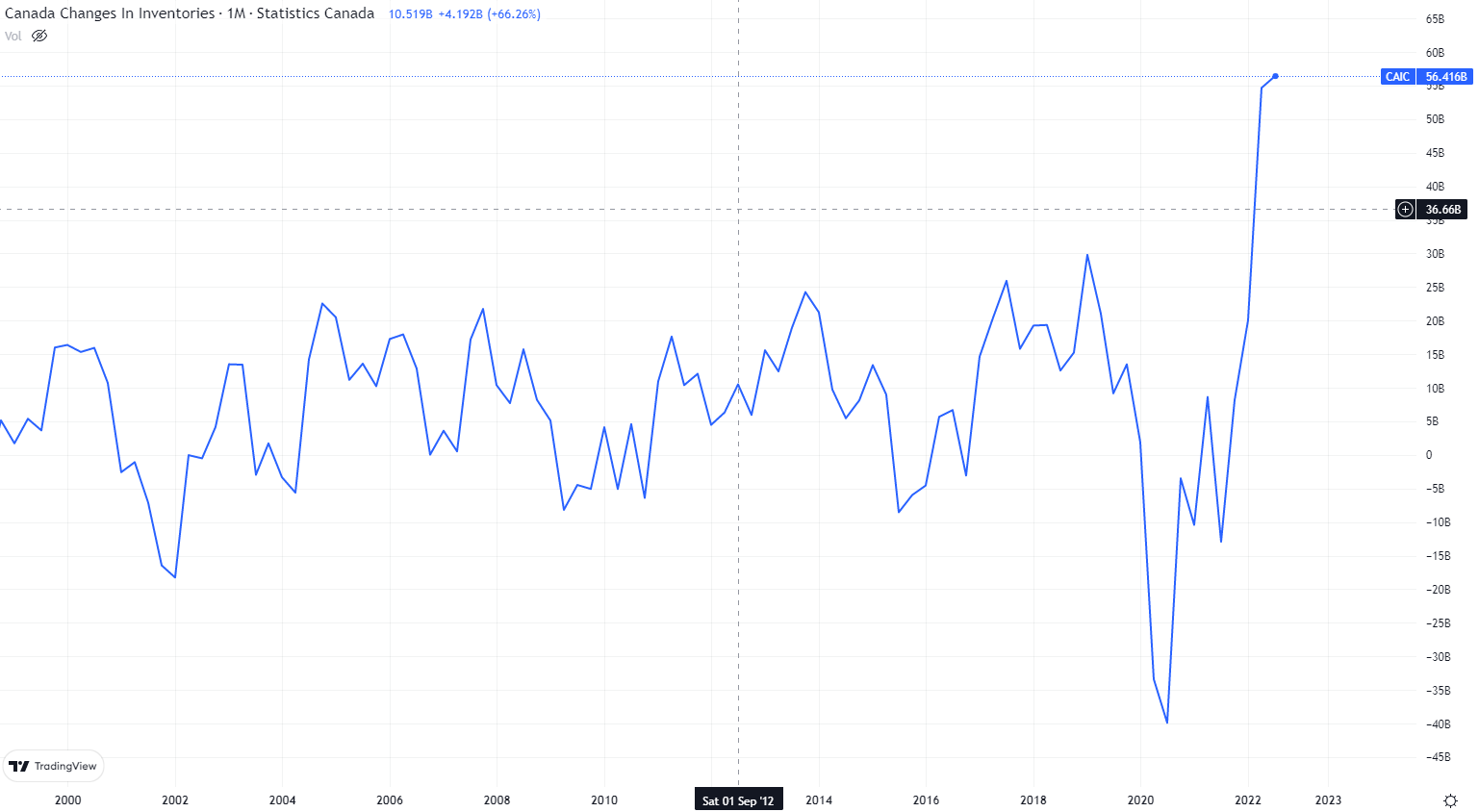

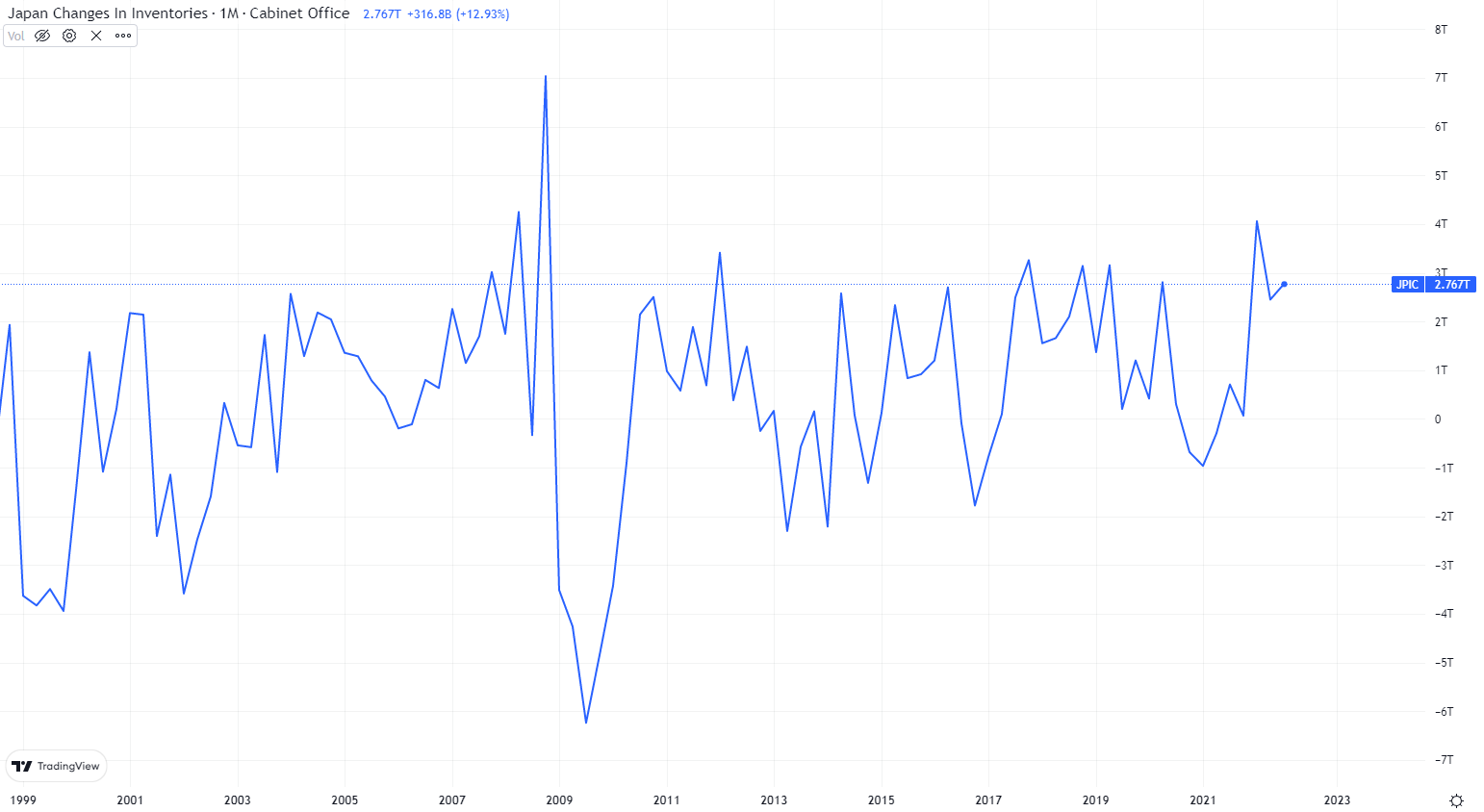

I referenced in Geek Squad Reboot back in August last year how the pandemic had served as a sort of unplug and plug back in of the global economy. Here are the changes in inventory levels in each of the G7 economies:

Obviously, the sizes of the economies and related inventories vary, but we can see that the breadth is significant at a very high level. As demand went up in 2020-2021 from the massive stimulus, prices ramped and production to meet demand followed. Inventories were built, and now…..

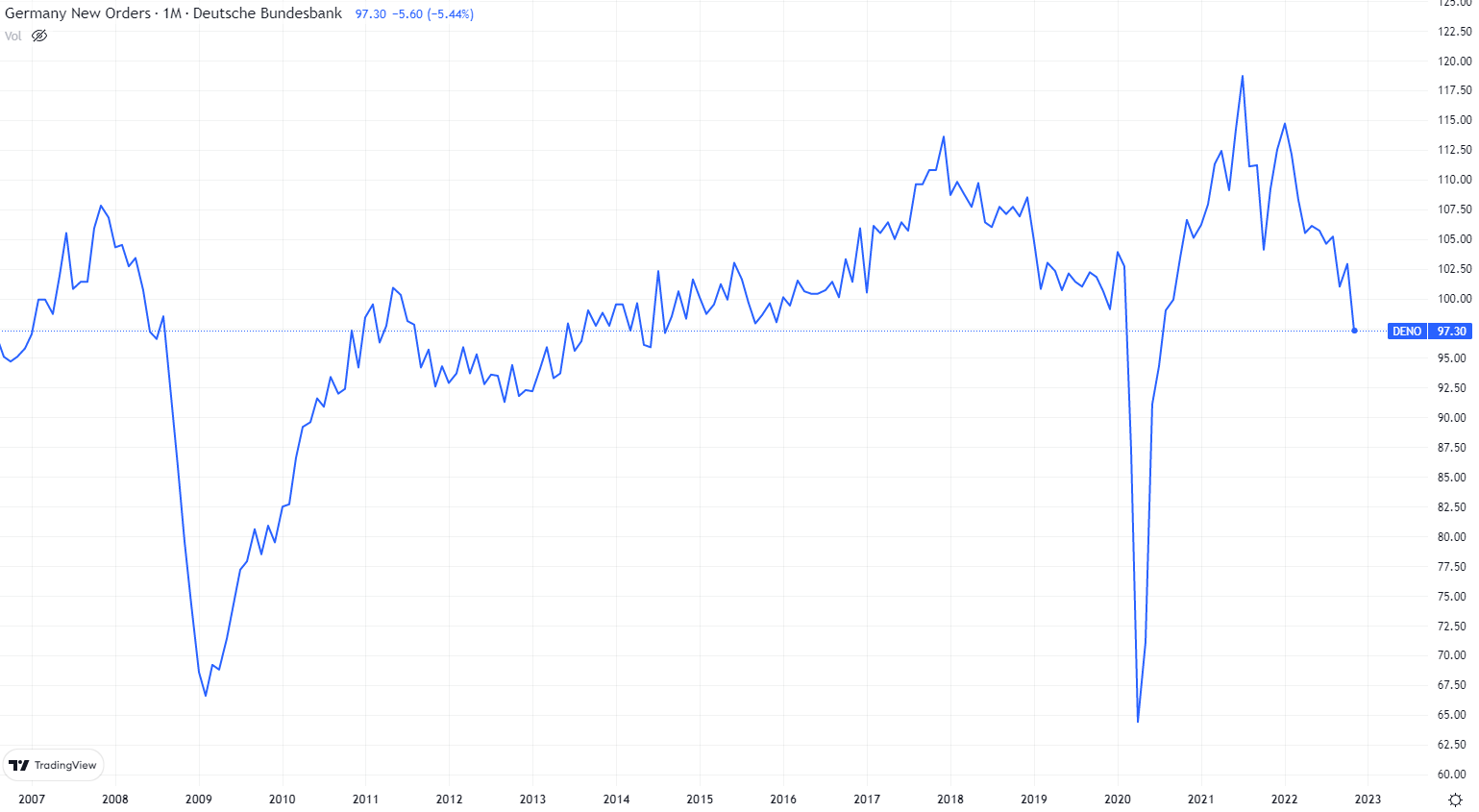

Those are factory orders in the US, UK, and Germany. Here are industrial materials priced in US dollars:

With inventories still extremely elevated, and what is likely to occur to orders? If/when orders continue to decline, and possibly a “sudden plunge” continues, what will happen to demand for industrial materials? What happens to related employment in manufacturing and industrial industries?

High inventories lead to cutting orders, which leads to falling production, which leads to job cuts, which leads to lower incomes, which lowers demand, etc. etc. etc.

Yes, the US economy is far less cyclical than it used to be, but the volatile components of the economy have already begun to contract. The service sector has only contracted in modern times during the most severe US recessions such as 2007-2009.

The NBER does not place much weight on quarterly GDP data- they look at a wide breadth of monthly data because GDP is not broad enough and subject to large revisions. Co-incident economic data for the US that the NBER looks at is already near a zero growth rate, and the US and G7 countries STILL have a ton of inventory and central banks are STILL tightening.

The is from the most recent UK monthly GDP report for November, also likely subject to potential revisions - note the UK charts above, which may be a preview of how the other G7 countries’ economies are to unfold:

Financial markets remaining largely oblivious to cyclical forces unfolding for extended periods is not unusual, and the specifics of each cycle are different. The last few months, and particularly the last few weeks, have renewed optimism about a ‘soft landing’ and a Fed Pivot. Relentless speculation and short covering is par for the course in bear markets, as Lehman Brothers’ 55%+ rally off its lows when Bear Stearns was ‘rescued’ in March 2008 displayed.

The Kayfabe Capital analytical process, which focuses on cycle timeframe developments, remains firmly in the Mack Attack camp.

*The first post for the Dodo Bird Model Portfolio was sent on Friday, January 27th. If interested, instructions on the Substack app to access are here.

It's a fascinating moment in markets, and a fascinating time to be able to follow so many smart people publishing their thoughts. I remain most convinced by the arguments (like the one presented here) that a recession is, indeed, on the way and there will not be a soft landing. What this actually means for asset prices is another question. Will falling rates (after the recession hits) buoy multiples and counteract declines due to earnings? What will central bank reaction functions look like? How will fiscal policy play in?

Great post 💪🏻