Housing Heartache

Quite reasonably, many people look to the home building industry as an important component of analyzing the business cycle. I agree it is a vitally important and cyclical industry with far-reaching tentacles that spread through the economy. It is also a historical fact that the industry has been a leading component of post-World War II business cycles within the United States, as well as in other countries’ business cycles. All other things being equal, I would bet that it is more likely than not to be an industry that leads within business cycles more often than not in the future.

However, a primary reason that business cycle analysis is so difficult is that lead/lag sequencing, timeline, statistical relationships, and amplitudes are all inherently unstable over business cycles. The element that is never ‘different this time’ is that of the human condition. What is different every time are the specifics of the dynamics just mentioned.

For example, some of the challenges for business cycle-focused analysts for the GFC period were:

The extended period of yield curve inversion prior to the onset of the recession was dated to have begun in December 2007.

The boom of the preceding expansion was focused on housing, specifically in mortgage finance. The initial period of recession unfolded with relatively narrow diffusion - i.e. the weakness was significant in that specific portion of the economy, but had not yet ‘spread’ more broadly.

Much of the world was still growing well into 2008, as the lead/lag nature of the cycle happened to have manufacturing and the associated Mack Attack, including its disproportionate impact on emerging market economies, in a lagging position. This resulted in the persistent ‘decoupling’ narrative and cycle denialism by many all the way up until Lehman Brothers went bankrupt. Indeed, manufacturing held up relatively well into August 2008.

Traditional business cycle orthodoxy is geared toward the cyclical components of the economy, which are inherently more volatile, as typically populating the ‘lead’ portion of indicators - residential home construction being part of that bucket.

Narratives are nice and clean, and seemingly obvious, retrospectively. Now it is obvious that the yield curve inversion for the cycle was presaging the implosion in the financial industry and housing, which eventually dragged down other industries into the recessionary culmination from late summer 2008 into spring 2009. Housing was the epicenter of the boom and served to lead the recessionary bust as well, with manufacturing lagging.

I believe this cycle is displaying an inverse dynamic, as the good-centric boom that transpired during the pandemic period is now leading the recessionary bust. Throw in some unfamiliar dynamics relating to the pandemic period, and the Fog of Cycles is extreme.

The normal difficulty of navigating these cycles, combined with the extraordinary nature of the pandemic period, was a large part of why this Substack was launched in November 2021.

The archive of this Substack since inception is filled with pieces that laid the foundation for these dynamics. A summary of some of the most relevant posts:

That last piece included speculation that the acute decline that had begun in early February and manifested in the banking failures in mid-March, would lead to another ‘soft landing’ period of optimism heading into summer.

We are there now, including all sorts of hidden interdependencies (see Schrodinger’s Bak) along the way, all within the context of a generationally epic mania continuing to unfold in the equity options market.

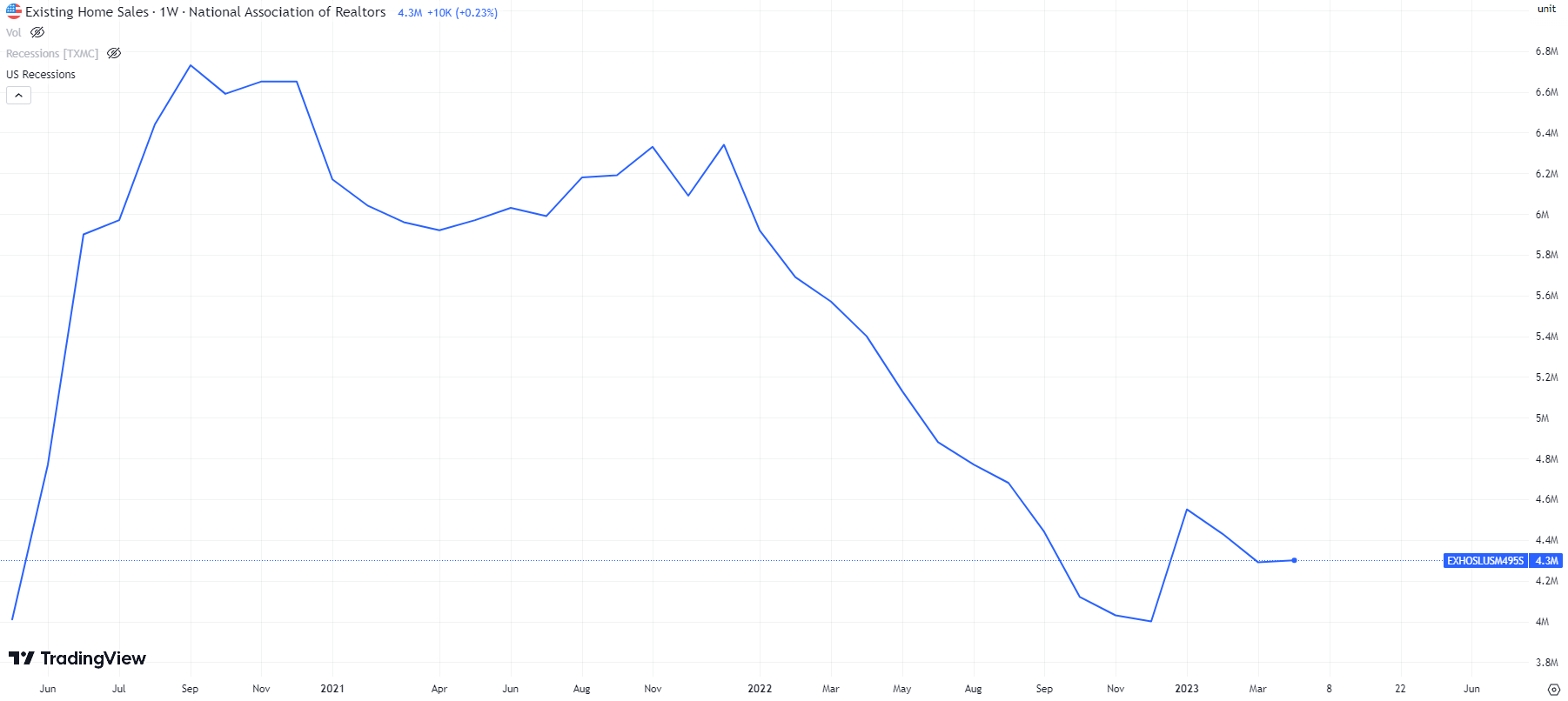

But as we revert back to the KISS It mantra, the cycle timeframe progression continues, including epic levels of narrative-fueled denialism. As referenced above, the recent upturn in the single-family residential homebuilding industry does not conform with the ‘script’ of housing leading the business cycle. But this cycle is VERY different, in that the explosive move in mortgage rates and home prices resulted in a massive decline in existing home listings, inventory, and transactions:

Here we see that the volume of existing home sales has declined by over 2 million homes since the cycle peak in 2021. A majority of homeowners with mortgages have sub-4% rates, and with record levels of unaffordability from high prices combined with 7%+ mortgage rates, many people are staying put. Of course, life throws various wrenches into the mix that force sales, such as divorce and job losses, with the latter being the biggie.

With the existing home inventory still down by nearly 50% from the cycle peak, housing demand is being disproportionately funneled into new homes (furthered by the ability of big builders to offer financial incentives like below-market mortgage rates), which have begun to trend higher in recent months:

Through the lens of housing being a ‘leading indicator,’ one could easily see how this could be interpreted as part of a ‘soft landing’ narrative. Indeed, I have seen this argument being made a fair amount recently. My process suggests that the specific dynamics of this cycle will make this area of the economy suffer a lagged ‘cliff’ as job losses explode in the coming months - similar to manufacturing in 2008:

Every cycle throws curveballs above and beyond the normal problems with data quality, revisions, and the human condition. As we now rapidly approach the ‘Oh Shit!!!’ part of the cycle, those relying upon US homebuilding as the savior are likely to experience heartache. The cycle is always different this time.

Hate the Illusion, love the Meme!

Incredible post! Thank you for the needed additional context. Amazing.